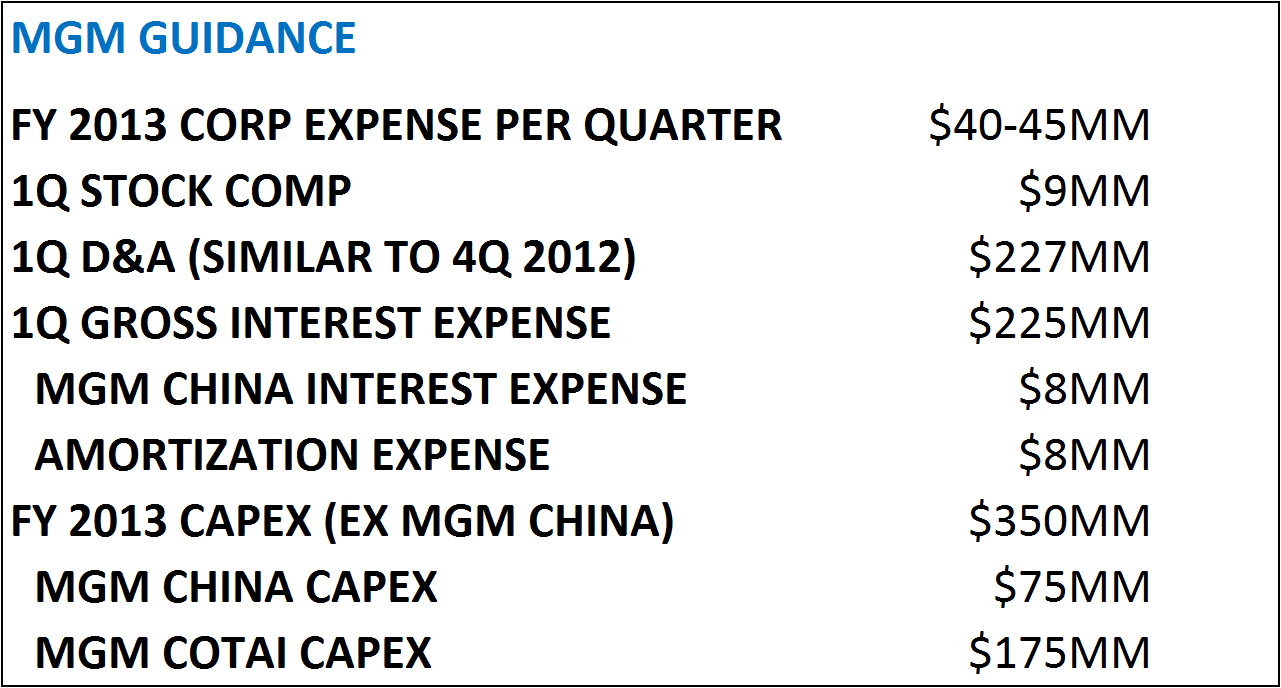

In preparation for MGM's F1Q 2013 earnings release tomorrow, we’ve put together the recent pertinent forward looking company commentary.

YOUTUBE FROM Q4 CONFERENCE CALL

- [MGM Cotai] "We remain on track, as we've said before, for an early- to mid-2016 opening."

- "Last quarter, a referendum was passed in Prince George's County in Maryland, and we are now in the RFP process for what would be a very lucrative fixed license in Maryland. We have a deadline... of May to submit our proposal. We will easily meet that deadline. We believe that we will prevail for an MGM at National Harbor, which is a tremendous destination resort, literally minutes from our nation's capital. A decision on that by the State of Maryland will be before the end of the year, we expect."

- "Our international casino business continues to be strong, as this was a record fourth quarter for our Strip properties when you include ARIA for both the international drop and win. We're seeing some encouraging signs in our domestic casino play, as our non-baccarat table drop at our wholly-owned Strip properties increased 6% year-over-year."

- "We are starting to see domestic customers again, starting to see their activity pick up."

- "Looking at the room trends here in the first quarter, we anticipate the trends to be similar to what we saw in the fourth quarter, with room revenues up low single-digits and essentially flat REVPAR."

- "While it is still early, ARIA is off to a good start in 2013, and we expect to continue to build traction throughout the year. Convention sales are pacing well, as room nights on the books for 2013 as of February 1 are 14% ahead of last year at this time....2014 is looking even stronger as we look forward. So there's still work to do in 2014, but its pace is actually even up higher than what we're experiencing here in 2013."

- [MGM CHINA] "We're seeing early signs of success from our level 2 VIP gaming floor expansion, which opened in late September. We're also expecting to add another junket operator in the second quarter of 2013. The fourth quarter was our strongest volume quarter for the year for our own in-house VIP business. We expect to see continued growth in this business with the support from the MGM International marketing team."

- [MGM CHINA] "This transition of mix has also driven an increase in our pre-branding-fee EBITDA margins by 60 basis points. We expect this positive trend of increasing main floor mix to continue, driven by upgrades to our main gaming floor product, marketing efforts, and of course the strong growth in the Macau mass market revenues."

- "On the convention side, without the solid citywide convention base, what ends up happening is our lower-end properties Circus and Excalibur, they're the last to fill, and there's always a challenge there from a pricing perspective. With regards to Luxor, they're also usually a benefactor of Mandalay's overfill, and that hasn't quite happened as much as it used to happen in the past, but it's well-positioned to get that overfill coming up in the future here."

- "We like the way our convention business is shaping up for the calendar year 2013, and obviously the leisure and transient business has been performing well for us. That's a big part of our business, so I think it's too premature right now to go out with full-year guidance. We like the way the calendar is shaping up, and we like the way the convention business is booked and the pace that we're on, and I think the best is to kind of leave it at that for now."

- "I'd just reemphasize what's happening for us, in the second quarter, between when someone spends over $100 million on the corner of Tropicana and the Las Vegas Strip in Hakkasan to build a night club/lounge/bar, which right now has been a construction site and has been for the better part of nine months, is going to have a material impact on MGM Grand; having a Mayweather fight in May, material impact on MGM Grand; having a new Cirque show at Mandalay Bay, a material impact in the second quarter for Mandalay Bay; and the restaurants that we're adding there."