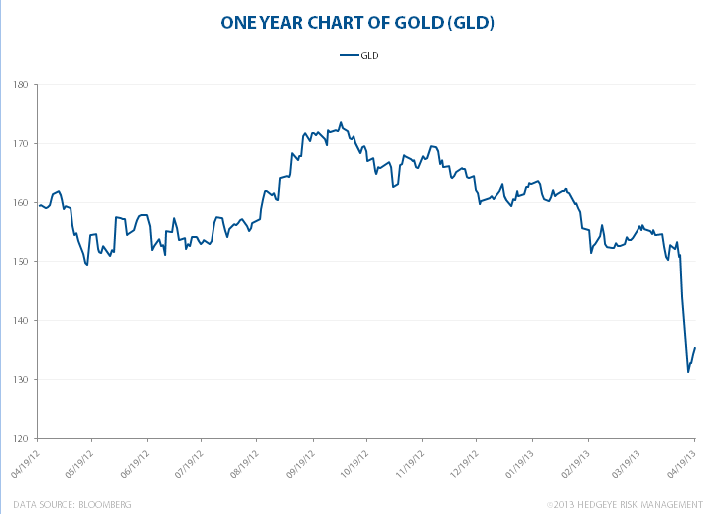

This week started off with the price of gold plummeting nearly 11% intraday on Monday, followed by a small recovery in price as the week progressed. Institutional investors, including hedge funds, banks and asset management firms, fled the precious metal, selling off gold and gold-related stocks like miners.

The SPDR Gold Trust ETF (GLD), by far the most popular and liquid way to trade gold, is down -5.75% since Monday and is down a whopping -14.9% over a one-year period. Pundits who said gold would go to $2000 are undoubtedly in need of a stiff drink after this week. We've made our case for long consumption/short commodities since the beginning of the year and believe that gold can fall further, especially if the US dollar continues to appreciate in value.