“For unless man were to be like God and know everything, it his better that he should know nothing.”

-John Buchanan

The Gap in the Curtain (1932) is a novel by John Buchanan that speaks to the human desire for certainty, and the dangers its quest can bring.

In a London country house, five party-goers partake in an experiment that allows them a glance at a newspaper that will be printed exactly one year in the future. The rest of the book tells the story of how that information affected each of their lives over the next year.

One man reads of a business merger, spends the next year painstakingly traveling the world buying every share of the to-be-acquired company he can find, only to find that the business combination he read of was one nearly out of bankruptcy… Another character reads his own obituary and dies of a heart attack the night before it prints; he does not live long enough to read the correction the paper issues on the following day for the typo…

---

This exchange from Core Laboratories’ (CLB) earnings call yesterday reminded me of the novel:

Analyst: “So, what’s your prediction, where is oil going from here?”

David Demshur, CEO of CLB: “Don’t have a clue, my friend.”

I sympathize with the analyst’s question – wouldn’t that be nice to know! – but, more so, I appreciated Demshur’s candid answer.

Gold is going to $2,000… Oil will spike to $200/bbl… My price target for the S&P500 at year-end 2013 is 1,458…

Wall Street loves making declarative statements. I used to think that I had to make them too – I was scared to say “I don’t know,” as if I should have the answers to so many inherently unknowable questions. But after several humbling experiences early in my career – i.e. being wrong – I have “resigned from the professional undertaking of coin-flipping,” to quote one of my favorite risk managers and thinkers, Hugh Hendry.

Sure, I have my biases – commodity prices tend to mean revert, oil lower (possibly a lot lower), Peyto Exploration (PEY.CN) higher (possibly a lot higher), LINN Energy (LINE, LNCO) and EV Energy Partners (EVEP) lower – but really I try to let the market tell me what to do (embrace uncertainty and our complexity-based models) and make solid risk-adjusted investment decisions given those signals.

Our playbook since the beginning of the year has been long USD and US consumption-oriented sectors, and short commodities and commodity beta. Our Macro Team reviewed our #StrongDollar theme on our 2Q13 Macro Call on Tuesday – we’re bullish on the USD due to:

- All-time low interest rates with the prospect of a hike;

- Cessation of QE initiatives;

- Improving housing and employment picture;

- Addressing all-time highs in sovereign debt and deficit ratios;

- USD solidified as world reserve currency at the expense of a weaker Yen and Euro.

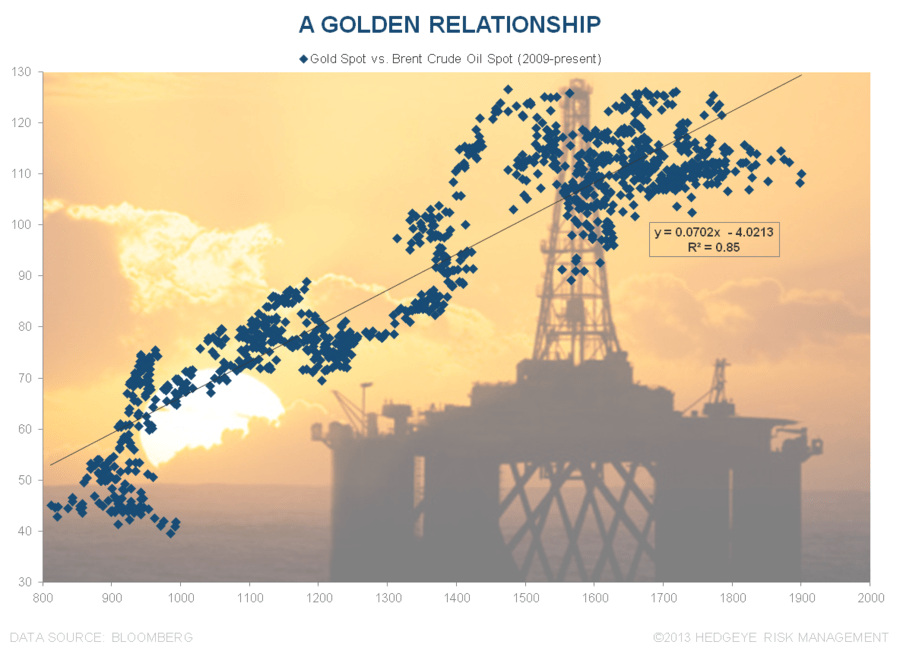

From there we think that a #StrongDollar deflates commodity inflation and takes commodity-levered sectors (XLE and XLB) lower with it. If you don’t think I should paint a broad brush across “commodities,” tell me why gold and oil have a +0.92 correlation since ’09 (see Chart of the Day). We think it’s the same “inflation hedge” trade that’s now unwinding…

Today, the risk management signals across the “financialized” commodity complex are still not good:

- Gold is bearish TREND (needs to recover: $1,681)

- Copper is bearish TREND ($3.58)

- Brent Crude is bearish TREND ($110.54)

- WTI Crude is bearish TREND ($93.88)

- Energy Stocks (XLE) are bearish TREND ($76.87)

So as our fundamental #StrongDollar theme plays out, and oil and energy stocks begin to break down across our core TREND duration, we want to be underweight energy, looking for energy stocks to sell/short, and know that our energy long ideas have to be really tight (imminent catalysts or special situations) or levered mostly to natural gas prices (bullish TREND).

---

Two stocks that I think are worth selling are LINN Energy (LINE, LINCO) and EV Energy Partners (EVEP). I wanted to hit on this in this note because these stocks are hugely popular among retail investors, which are attracted to that juicy yield (LINE 8%, EVEP 6.5%). It’s kind of funny – any time Keith or I tweet about LINE/LNCO we get borderline hate-mail in return! But how much cash a company pays out to its shareholders says nothing of the intrinsic value of the business – and these stocks are hugely overvalued, and their distributions sustained with capital raises. The distributions paid are inconsistent with the economics of the businesses, and we think it ends in tears. Hedgeye subscribers, do not be left holding the bag!

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, EUR/USD, UST10yr Yield, VIX, and the SP500 are now $1, $96.72-102.27, $81.95-83.11, 96.63-101.57, $1.29-1.31, 1.68-1.76%, 14.27-18.68, and 1, respectively.

Have a great weekend,

Kevin Kaiser

Senior Analyst