McDonald’s is set to release March sales, along with 1Q13 earnings, tomorrow before the market open. Expectations are muted for March comparable sales but we believe the back half of the year is where there is most potential for a disconnect versus expectations. The stock has broken higher from $85 with no supporting increase in earnings estimates. The 1Q13 consensus estimate of $1.26 or 3% EPS growth looks aggressive but the company has many levers to manage the number. We will be hosting a call on April 25th to go through our bearish stance on MCD FY13 EPS versus expectations in more detail.

The company reported February sales on March 13th and, since then, MCD has outperformed the market by 340 bps. We continue to believe that the stock is ahead of the company’s fundamentals, with little upside to earnings for 2013 leaving the multiple embedded in the stock stretched.

Specific to the earnings release, we will be focused on the following:

- Any update to 2013 guidance (sales, costs, reimaging, FX)

- US comp in April

- Commentary on competition in the QSR segment and MCD's value push

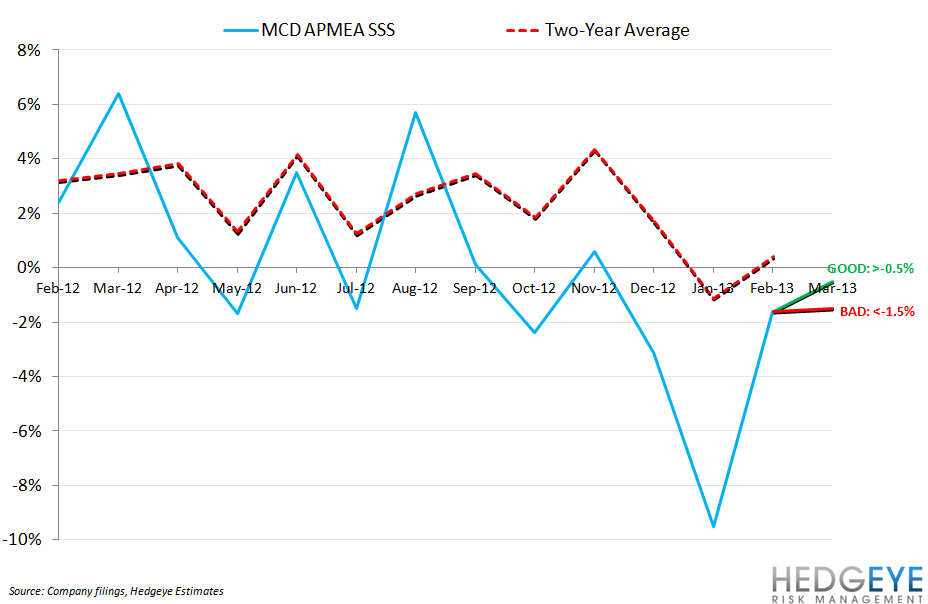

The charts below illustrate what we believe the investment community will perceive as good, bad and neutral results for the US, Europe, and APMEA March sales.

Howard Penney

Managing Director

Rory Green

Senior Analyst