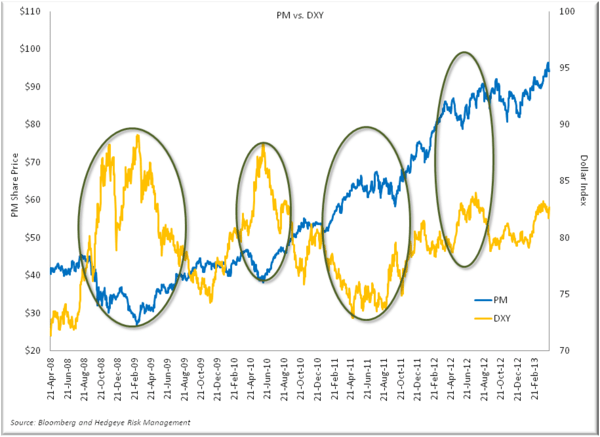

Philip Morris International (PM) reported weak first quarter earnings for 2013. One of the major headwinds the company is up against is a stronger US dollar. In the chart below, we've highlighted periods of dollar strength and weakness and how it is inversely correlated with strength and weakness in the share price of PM. When the dollar is weak, PM's share price tends to rise and vice versa. The outlook for Philip Morris is not a positive one on our end and we believe the company will have a rough time meeting earnings per share (EPS) estimates going forward.