PM is on the tape with Q1 2013 EPS of $1.29, a shortfall of $0.05 versus consensus – however, currency was a $0.07 headwind in the quarter. Currency is now forecasted to be a $0.19 headwind for the year (versus $0.06 prior) resulting in a $0.13 downward adjustment to EPS at both the top and bottom end (now $5.55 to $5.65). Underlying guidance remains unchanged.

PM posted a volume decline of 6.5% (against the toughest comparison of the year, +5.4%). Volume was weaker than consensus in multiple regions – European Union (-10.1% reported versus -6.7%), Asia (-10.4% reported versus -5.4%) and Latin America and Canada (-7.5% reported versus -1.0%). However, again, Q1 was the most difficult comparison of the year in each of those regions. Despite the volume shortfall versus consensus, reported revenue (net of excise taxes) of $7.584 billion came in slightly better than consensus, against a very difficult comparison. Constant currency organic revenue growth was +3.2% despite the volume print, indicating to us that the pricing architecture for 2013 is in place and intact.

Operating income declined year over year (-0.6%), currency neutral EBIT +2.9%, so the company saw negative operating leverage for the first quarter since Q4 2011 – not surprising given the volume print in the quarter.

What we liked:

- Preservation of underlying operating guidance

- Solid pricing architecture in place for 2013

- Respectable constant currency organic revenue growth of +3.2% against a difficult comparison

- Comparisons ease substantially through the balance of 2013

What we didn’t like:

- EPS miss and reduction of guidance (even if for no reason other than currency)

- Volume weakness across multiple regions versus consensus (and even versus our more bearish estimates)

- Lack of operating leverage (first time since Q4 2011)

- Awful FCF generation in the quarter (-32.8%, and -17.1% adjusting for currency)

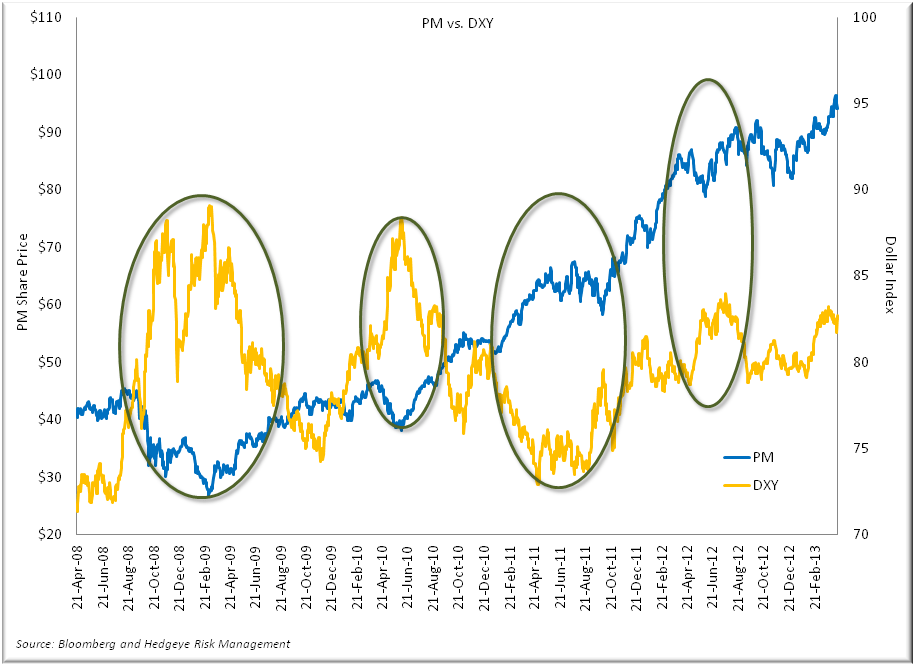

It’s tough for us to be positive on a stock when EPS estimates are heading lower (regardless of the reason) and when we couple that with a firm view of continued strength in the U.S. dollar, we have a hard time getting behind PM at this point despite what we readily acknowledge as strength in the underlying business model.

Call with questions,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst