This note was originally published at 8am on April 04, 2013 for Hedgeye subscribers.

“Chickity China the Chinese Chicken. You have a drumstick and your brain stops tickin’.”

-Barenaked Ladies (1998)

Thank goodness the A-Shares are closed today.

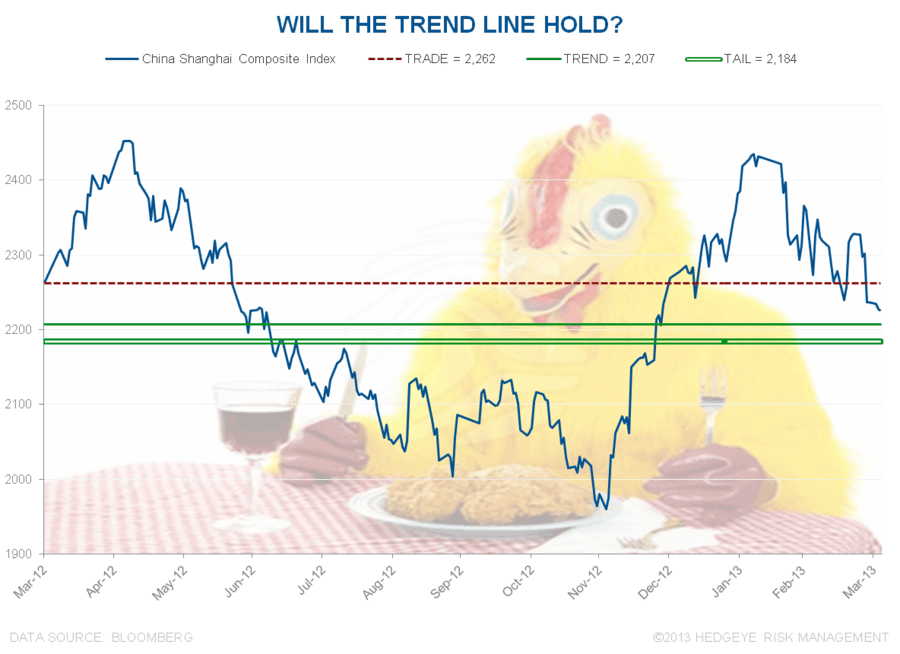

Ok, perhaps that is quite a bit dramatic, but we’re certainly not thrilled by the fact that the Shanghai Composite Index is down -3.8% since our Macro Team pitched Chinese equities on the long side in our 2/27 Best Ideas Presentation (underperforming the regional median equity market gain of +1.3% by 507bps).

The lesser analyst in me would’ve begun the note pointing to the SHCOMP’s +6.8% delta since 12/10 (when we originally introduced the idea), calling for the index to continue making higher-highs and higher-lows over the intermediate term.

While that remains our base case scenario – for now at least – we would be remiss to ignore what we have learned from Dr. Daniel Kahneman’s work in the then-groundbreaking field of prospect theory – specifically in that economic agents A) assign an asymmetrically greater absolute value of utility to losses then they do to gains and B) multiple gains and/or losses are accumulated to create an overall feeling about a series of transactions that extends from the most recent, not original, reference point.

Applying prospect theory to our bullish bias on China, the absolute value of the negative utility associated with the -3.8% delta since 2/27 is likely in excess of the positive utility associated with the +11% delta from 12/10 to 2/27. Loosely applying the above quote from our Canadian friends up north (which itself hardly makes sense even in the context of the song it is sourced from), it would be fair to say that the Chinese stock market has indeed indulged in a rather infamous “drumstick”.

Cutting to the chase, it was our view that Chinese authorities would delay any tightening of monetary policy and/or macroprudential regulation until well after the country’s economic recovery had been firmly entrenched – creating cover for at least 3-6 additional months of potential upside for a traditionally high-beta market. With the introduction of the early-MAR propriety curbs, the late-MAR clamp-down on wealth management products (WMPs) and the dramatic acceleration in official recognition of systemic risks in the financial sector, however, it has become quite clear to us that the aforementioned view was dead wrong.

No doubt these measures will have some negative impact on Chinese economic activity, which we still see as accelerating over the intermediate term. But as prospect theory would have, the negative delta from our original, fairly-subdued expectations for a Chinese economic rebound to our updated view of an even more muted acceleration likely registers the entire sequence as a negative utility event.

In broader terms, it’s bad when your bull case gets less bullish, at the margin. Moreover, to the extent that the bull case was consensus across the investment community, the initial delta from “positive” to “less-positive” in any fundamental thesis is often the first cue for experienced short-sellers to enter a particular market.

Is China a short?

While we don’t believe it is (at least not yet; as evidenced by Keith’s buy signal on the CAF yesterday afternoon), we would be downright slipshod to not thoroughly debate the merits of the bear case, which we did in our 3/28 note titled “IS CHINA CAREENING TOWARDS FINANCIAL CRISIS?”. To recap a few highlights:

- Last week China Daily reported that the China's banking regulator has urged banks to pay close attention to the credit risks in key industries affected by the economic downturn and hit by overcapacity woes. Zhang Ping, Chairman of the National Development and Reform Commission recently said that the industrial sectors suffering most from overcapacity include steel, cement, electrolytic aluminum, plate glass and coal coke sectors, each of which is operating at 70-75% of total capacity. Analysts estimate the outstanding loan portfolio of those industries may amount to around 30T-40T yuan ($4.83T-$6.44T or 22.6-30.2% of total banking system assets at the end of JAN). Per the PBOC, outstanding loans to the property sector were 12.1T yuan at EOY ’12.

- In addition to these on-balance sheet risks, China has roughly 15T yuan of off-balance sheet credit (28.8% of GDP) in the form of commercial bills, trust financing, entrusted loans, etc. that has increasingly been allocated to riskier borrowers in recent years (per various agencies, including the IMF) – many of whom which have outsized exposure to property prices, such as property developers and local gov’t financing vehicles (LGFVs). The latter entity has 636.8B yuan in bonds outstanding as of EOY ’12 (+148% YoY) and 9.3T yuan of loans outstanding (17.9% of GDP) – 20% of which are “funding projects which are largely not profitable and thus are vulnerable to [repayment] risk,” per PBOC Governor Zhou Xiaochuan.

- The next round of interest rate liberalization should promote better real returns and improved access to credit for Chinese households and SMEs, respectively, and that may perpetuate an unwind of off-balance sheet lending activities, which, according to most sources, have been largely capitalized with the surplus savings of China’s private sector that are seeking higher real yields via Trust Products and WMPs, where average annualized yields are 37% higher than the PBOC’s benchmark 1Y household deposit rate of 3%. To the extent there are any weak hands in the WMP or trust financing sectors, a lack of new inflows, at the margins, would expose the “ponzi-scheme” nature of some products (per the words of the Xiao Gang, Chairman of the Bank of China) – specifically those that rely on short-term funds in order to invest in illiquid fixed assets and fund distributions largely with new net inflows.

- Ultimately, the most recent WMP regulations should translate into slower (and potentially even negative) growth in the supply of credit within the shadow banking channel and to the extent any existing liabilities facing repayment risk aren’t able to be rolled over, we will start to see default rates accelerate across China’s shadow banking sector. Any spillover effects across key industries – particularly in the oversupplied construction and construction materials sectors – could adversely impact Chinese bank NPL ratios (currently at 0.95%) on a lag.

In spite of all this, we continue to hold a reasonably high degree of conviction in our bull case on China, as a core driver of the thesis (i.e. Strong Dollar) is, in fact, the same bull case for US equities we have held since late 2012 that consensus has largely ignored and/or fought all year. To sum it up in a few bullets:

- As expected, early MAR growth data is supportive of the Chinese economy resuming its trend of broad economic acceleration (the official Manufacturing PMI accelerated to 50.9 from 50.1 and the official Non-Manufacturing PMI accelerated to 55.6 from 54.5).

- A sequential slowing in China’s MAR CPI and PPI figures (due out 4/8) is highly probable from the Lunar New Year jump in FEB. Moreover, continued gains in the CNY (at a ~19yr high) should weigh on inflation expectations over the intermediate-to-long term as China reorients its economy, though rebalancing certainly won’t happen overnight. Amid rebalancing, the country’s import model should change (less commodities; more consumer goods), ultimately increasing the impact of currency fluctuations upon consumer prices.

- Lastly, continued USD strength should continue weighing on the prices of internationally-traded commodities, which should ultimately allow the pace of economic activity to creep higher in China on a lag. China’s heavy industry benefits from energy and raw material deflation via margin expansion and potentially increased production, at the margins, in a backdrop of subdued credit expansion. Additionally, Chinese consumers benefit from food and energy deflation by freeing up share of wallet for more discretionary goods and services.

All told, being long of China is certainly a non-consensus position at the current juncture. In spite of fairly recent gains, the fundamental backdrop for the Chinese stock market is as convoluted as it has been in quite some time. As such, we are sticking to our process and deferring to the quant on this one.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/JPY, UST 10yr Yield, VIX and the SP500 are now 1542-1594, 106.26-109.11, 82.55-83.46, 93.07-96.11, 1.81-1.93%, 12.31-14.54 and 1546-1576, respectively.

Keep your head on a swivel,

Darius Dale

Senior Analyst