Quick comment on weekly POS data.

Though aggregate sales trends in athletic footwear and apparel remain fairly consistent, we’re seeing some interesting movement amongst the brands – specifically UnderArmour.

UnderArmour had a monster week in both apparel and footwear – great timing given that it reports earnings on Friday. UA’s apparel sales continue to run at a 30% clip, which is very consistent despite a downtick for the category in general. But UA Footwear clocked in growth over 70% last week per NPD. That’s on top of 40-50% growth in the preceding two weeks. This is the first time we can recall UA’s market share ever being closer to 2% than 1%.

It’s been our view that UA will need to step up its SG&A dollars in the back half to achieve the kind of growth (footwear and international) that investors are paying for. If the company can hang on to the growth rate we’re currently seeing in footwear for the duration of the year, it will add about 4%-5% consolidated growth to the parent. We’ll be surprised if this is the case – especially given the fact that UA is currently going against its easiest compares of the year (they get tougher in mid-May).

Nonetheless, these numbers can’t be ignored. And with a good print coming up on Friday and excitement around UA’s analyst meeting in June, they’re coming at a good time for its multiple. The sustainability of this growth rate is officially the number one issue we’re focused on right now with UA.

UnderArmour’s Footwear Business Is Having a Great April

Source: The NPD Group

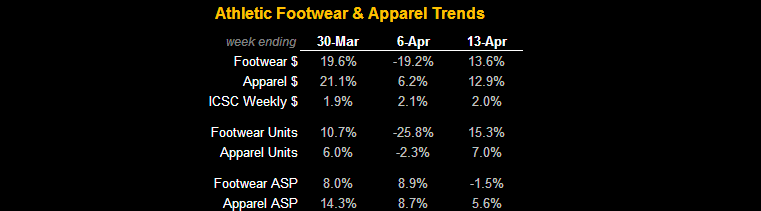

Athletic Industry Sales: Athletic Footwear and Apparel (Trailing 3-week)

Source: SportscanINFO, ICSC, The NPD Group, and Hedgeye

Athletic Industry Sales: Athletic Footwear and Apparel

Source: SportscanINFO, ICSC, The NPD Group, and Hedgeye

Footwear Market Share By Brand

Source: The NPD Group