CAT: Why Consensus Is Coming Our Way

Resource-related Capital Investment Cycle: When commodities rise sharply, resources-related capital spending ramps quickly to bring on additional supply. A subsequent flattening or decline in commodity prices can bring resource-related capital spending back to trend levels – typically not far above maintenance levels, since the industries are generally mature. Currently, resources-related capital spending is very high following 100+ year outlier gains in many commodity prices, like iron ore, copper and gold.

Expect Very Large Declines: Some are looking for slower growth or small declines in resources-related capital spending. That expectation is inconsistent with history and logic. As the chart above shows, resources-related capital spending declined 80% over a five year period following peak orders in the late 1970s. CAT posted very large losses in the early/mid 1980s, in part as a result of this readjustment. As the chart below shows, a return to slow output growth levels of capital spending (approximated by depreciation and amortization) would bring a ~70% decline in capital spending at large miners. Mining is not a growth industry. In the long-run, capital spending should be expected to approximate DD&A.

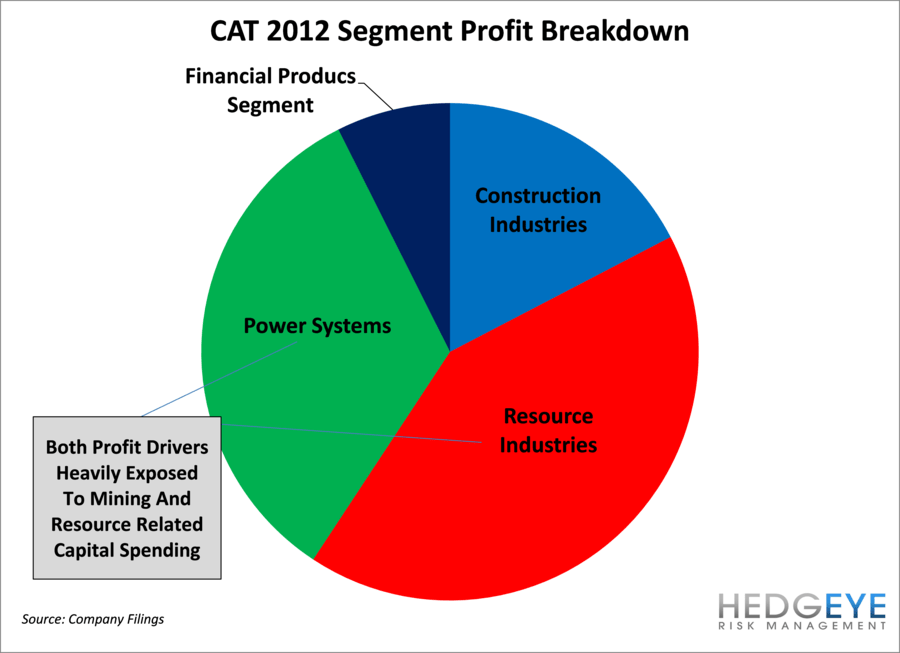

Resources Capital Equipment Is Where CAT Makes Money: Approximately three-quarters of CAT’s 2012 operating income was derived from Resource Industries and Power Systems. Both of those divisions are heavily exposed to resource-related capital spending. Resource Industries counts sales of mining equipment to coal, copper, iron ore and gold mines as its largest end-markets. Power Systems sells locomotives to mines and railroads, power generation systems to mines/resource companies and power plants, turbines to gas compression and energy extraction sites, and other end markets. Picturing the impact of a 50% decline in resources-related capital spending (not at all unlikely in our view) on the operating income of CAT does not require much imagination.

Value Traps: CAT, Komatsu and other diversified resource-equipment suppliers are likely to look cheap on multiples for years to come. They will go down and investors will buy them thinking they are values, only to find that results weaken yet further. Beware the low PE in cyclicals – it is frequently a sign of a cycle peak or decline.