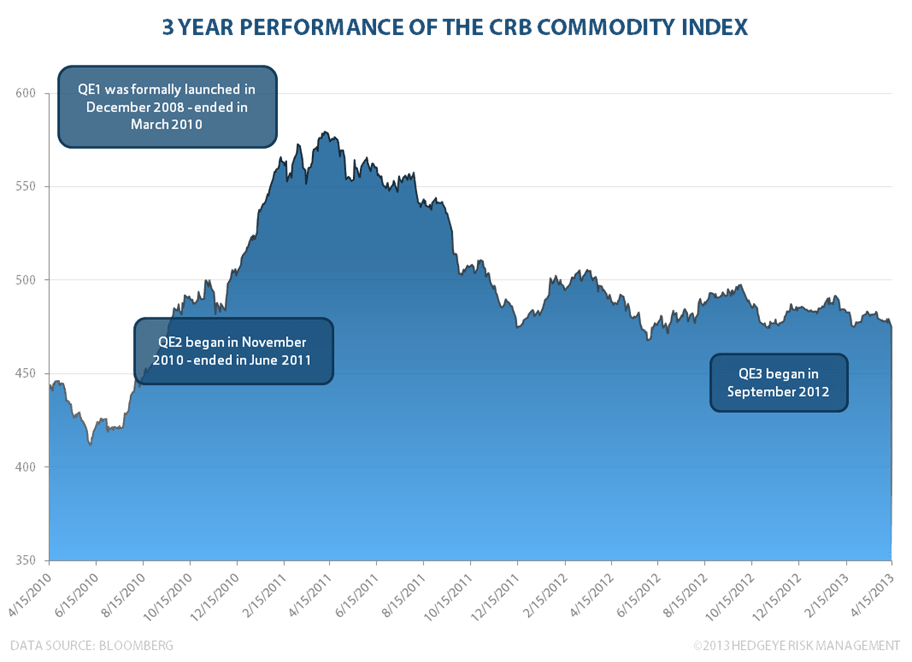

Commodity prices have been under pressure since the beginning of the year. The rise of the value of the US dollar has contributed greatly to the decline in prices across the board. On Monday, gold, oil and other commodities sold off en masse as investors fled the asset class and liquidated their positions. Gold fell anywhere between -10% intraday to -7.5% at the close. The CRB Commodity Index, which measures 19 different types of commodities, took a big hit on top of an already difficult year yesterday. You can see the decline in the chart below.