TODAY’S S&P 500 SET-UP – April 16, 2013

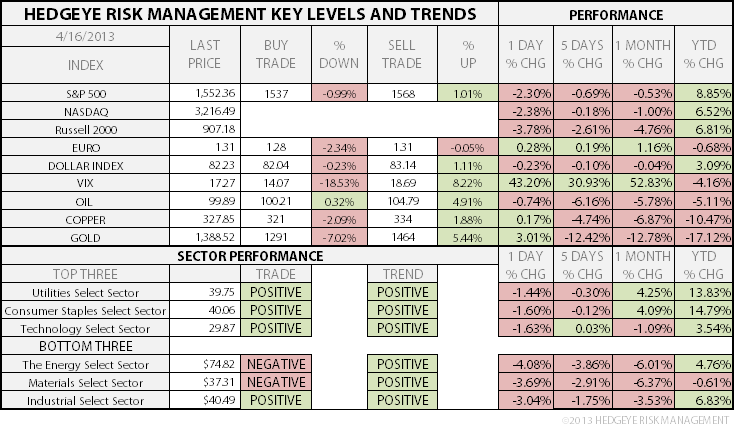

As we look at today's setup for the S&P 500, the range is 31 points or 0.99% downside to 1537 and 1.01% upside to 1568.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.50 from 1.46

- VIX closed at 17.27 1 day percent change of 43.20%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8am: Fed’s Dudley speaks in Staten Island, N.Y.

- 8:30am: Consumer Price Index M/m, March, est. 0.0% (prior 0.7%)

- 8:30am: CPI Ex Food & Energy M/m, March, est. 0.2% (prior 0.2%)

- 8:30am: Housing Starts, March, est. 930k (prior 917K)

- 8:30am: Housing Starts M/m, March, est. 1.4% (prior 0.8%)

- 8:30am: Building Permits, March, est. 943k (prior 939k)

- 8:30am: Building Permits M/m, March, est. 0.4% (prior 3.9%)

- 8:55am: Johnson/Redbook weekly sales

- 9am: Fed’s Evans speaks in Chicago

- 9am: ECB’s Draghi speaks before European Parliament

- 9:15am: Industrial Production, March, est. 0.2% (prior 0.8%)

- 9:15am: Capacity Utilization, March, est. 78.4% (prior 78.3%)

- 9:15am: Manuf (SIC) Production, March, est. 0.1% (prior 0.8%)

- 11:30am: U.S. to sell 4W bills

- 12pm: Fed’s Duke speaks in Washington

- 3pm: Fed’s Yellen speaks in Washington

- 3pm: BOE’s King speaks in Washington

- 4:30pm: API energy inventories

- 5pm: Fed’s Kocherlakota speaks in Minneapolis

- 5pm: BOE’s Haldane speaks in Washington

GOVERNMENT:

- IMF issues World Economic Outlook, growth projection

- House Energy and Commerce panel marks up approval bill for TransCanada Corp.’s Keystone XL pipeline, 2pm

- FDIC Chairman Martin Gruenberg, White House Council of Economic Advisors Chairman Alan Krueger, House Financial Svcs Cmte Chairman Jeb Hensarling, R-Texas, speak at American Bankers’ Assn Government Relations Summit, 7:30am

- Senate Judiciary panel hears from DOJ antitrust chief William Baer and FTC Chairwoman Edith Ramirez on enforcement of antitrust laws, 2:30p

- Senate Commerce and Transportation Cmte hears from FAA Administrator Michael Huerta, NTSB Chairwoman Deborah Hersman on FAA’s progress on safety initiatives and the investigation of Boeing 787, 2:30pm

- 3M IP lawyer Kevin Rhodes, former USPTO director Jonathan Dudas testify before Judiciary Cmte on abusive patent litigation, 2pm

- Boston explosions kill 3, injure scores at marathon’s finish

WHAT TO WATCH

- Housing starts in U.S. probably increased as progress sustained

- Gold selloff sparked by Cyprus-sale concern, Goldman says

- Putin calls for stimulus as minister sounds recession alarm

- IMF issues World Economic Outlook, growth projection

- Energy Future proposes opening salvo as KKR, TPG seek 15% stake

- Fairway Group seeks premium to supermarket rivals in U.S. IPO

- AMR files bankruptcy-exit plan hinged on merger with US Airways

- Gensler-Wheatley panel aims to end conflicts in benchmark rates

- Blackstone-backed Senrigan’s fund said to lose 13% on Sundance

- Twitter said to seek deals with Viacom, NBC to feature TV online

- Glencore-Xstrata deal said to win China regulator’s approval

- Facebook talking with Apple about new version of home software

EARNINGS:

- BlackRock (BLK) 6:30am, $3.57

- Wolverine World Wide (WWW) 6:30am, $0.55

- Comerica (CMA) 6:40am, $0.68

- Coca-Cola (KO) 7:30am, $0.44 - Preview

- Northern Trust (NTRS) 7:30am, $0.72

- US Bancorp (USB) 7:30am, $0.73

- Goldman Sachs Group (GS) 7:30am, $3.87 - Preview

- TD Ameritrade Holding (AMTD) 7:30am, $0.26

- Johnson & Johnson (JNJ) 7:45am, $1.39 - Preview

- WW Grainger (GWW) 8am, $2.75

- CSX (CSX) 4:01pm, $0.40

- Intel (INTC) 4:01pm, $0.41 - Preview

- Yahoo! (YHOO) 4:05pm, $0.25

- United Rentals (URI) 4:05pm, $0.48

- Cathay General Bancorp (CATY) 4:30pm, $0.31

- Fulton Financial (FULT) 4:30pm, $0.20

- Linear Technology (LLTC) 5pm, $0.43

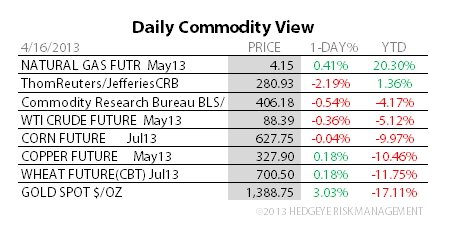

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Drop Splits Central Banks as Sri Lanka Sees Opportunity

- Silver Slump Splits Hedge Funds From Ingot Hoarders: Commodities

- Brent Crude Falls Below $100 a Barrel; WTI Lowest in Four Months

- Gold Gains as 14% Plunge Seen as Overdone, Central Banks May Buy

- Gold Slump Sparked by European Sale Concern, Goldman Sachs Says

- Japan Gold Retailer Sees Purchases Double Today as Price Tumbles

- Rebar Rises From Lowest in Four Months on Iron Ore Price, Demand

- Glencore’s $30 Billion Xstrata Deal Clears China Approval Hurdle

- Sugar Rebounds on Speculation Prices Fell Too Far; Coffee Gains

- Wheat Erases Decline, Climbs as Much as 0.3% to $7.0125 a Bushel

- Crude Supply Gains in Survey as Production Jumps: Energy Markets

- Record Ship Lines in Brazil Fail to Erase Capacity Glut: Freight

- Aluminum Rebound Seen as Opportunity to Sell: Technical Analysis

- Commodity Index Investments Fell $900 Million, Citigroup Says

CURRENCIES

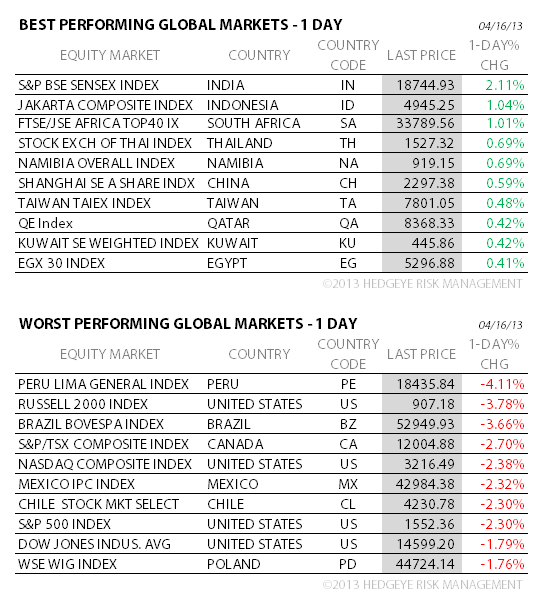

GLOBAL PERFORMANCE

EUROPEAN MARKETS

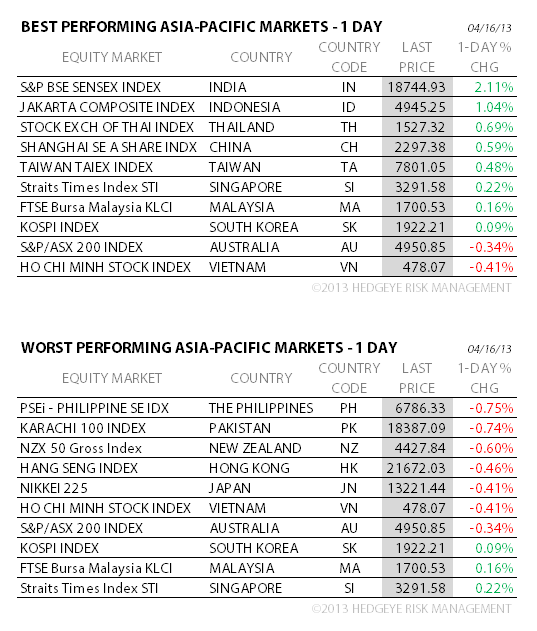

ASIAN MARKETS

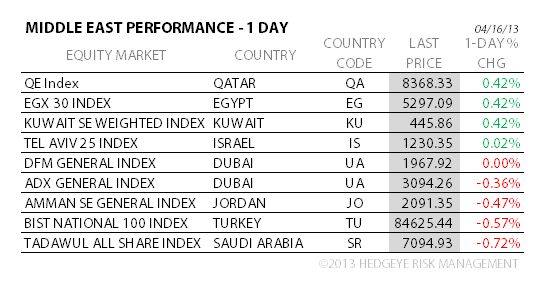

MIDDLE EAST

The Hedgeye Macro Team