This note was originally posted on December 14, 2012. As the price of gold crashes today, we’d like to point out that Hedgeye CEO Keith McCullough has shorted gold via the Gold Miners ETF (GDX) eight times since September 2012 and is batting 8 for 8 in our Real-Time Alerts.

SUMMARY BULLETS:

• Gold remains a crowded long for a variety of very obvious reasons – one of which could become less supportive, at the margins, on a sustainable basis.

• In the note below, we thought we’d take a stab at how a core component of the bull case (i.e. central bank diversification) can come unwound over the long-term TAIL. It’s very important to note that we’re not positing this as the only factor driving the market price of gold; nor are we necessarily suggesting that this is a thesis to run out and short gold today with. Rather, we are offering intellectual ammunition to understand what’s likely going on behind the scenes in the event gold continues to make lower-highs over the intermediate-to-long term.

• Sustained weakness in the JPY and EUR along with a diminished EM central bank purchases of gold (relative to investor expectations) could provide the necessary lubrication for a sustained USD rally and lower-highs in the price of gold over the long term.

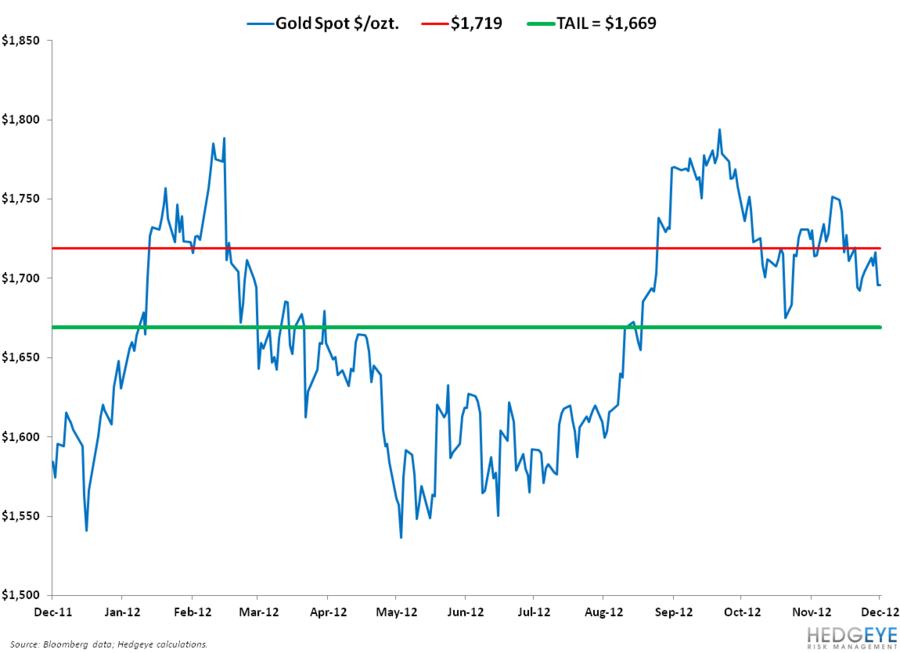

• All told, we think investors should consider reducing their allocation to this asset class. At a bare minimum, it would be prudent for gold bulls to confirm whether or not our TAIL support ($1,669) holds before increasing exposure to gold here. If $1,669 breaks, there’s no true support to the prior closing lows.

Gold is widely loved and probably over-owned – at both the institutional and sovereign level. Having appreciated in value for 12 consecutive years with a CAGR of 16.4%, the bull case on gold is well understood by just about every market participant.

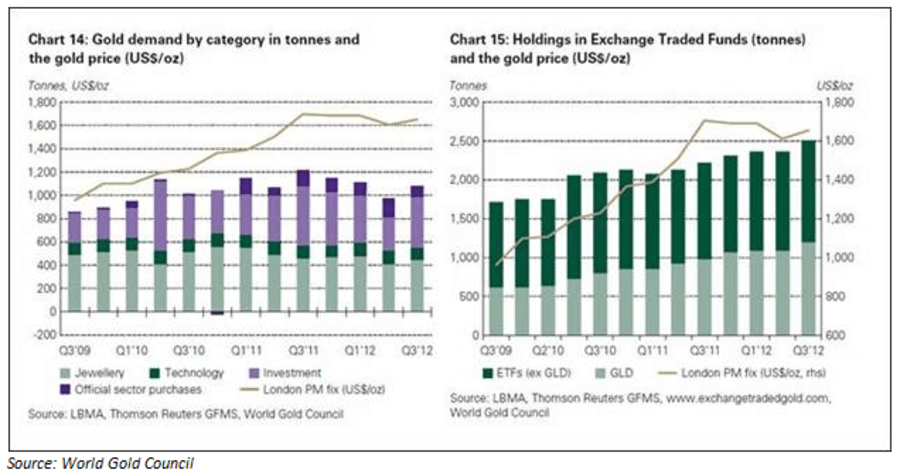

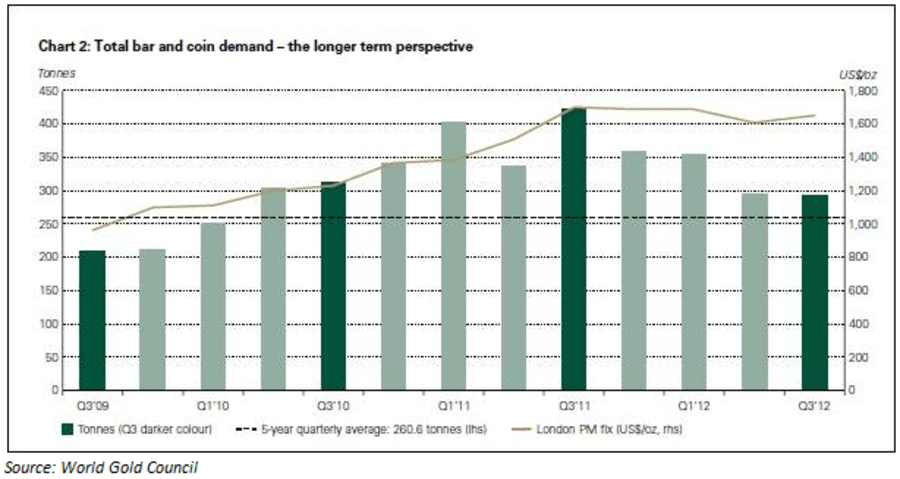

This is true from traditional L/S equity hedge fund managers all the way down to retail investors, as ETF volumes have been the only thing mitigating the precipitous decline in physical gold demand. The latest data from the World Gold Council (3Q12) showed overall demand had declined -11% YoY from the all-time peak in 3Q11, with every category posting a contraction except “ETF & similar”:

It’s not surprising to see demand for physical gold peaked when the price of hit an all-time peak of ~$1,900 early in the quarter.

We’ll hold off on the discussion on gold supply, as we firmly believe PRICE eventually leads supply in most, if not all commodity markets. For example, if the price of gold rips to the upside, gold miners will likely follow the move by instituting aggressive E&P plans. If the gold price were to plummet, many producers will struggle to operate their mines above the cost of capital and will eventually curb production. Anything in between probably equates to a status quo level of supply growth.

Going back to the point we made earlier about the bull case being deeply penetrated, we thought we’d take a stab at how a core component of the bull case (i.e. central bank diversification) can come unwound over the long-term TAIL. It’s very important to note that we’re not positing this as the only factor driving the market price of gold; nor are we necessarily suggesting that this is a thesis to run out and short gold today with. Rather, we are offering intellectual ammunition to understand what’s likely going on behind the scenes in the event gold continues to make lower-highs over the intermediate-to-long term.

THE KNOWN-KNOWNS

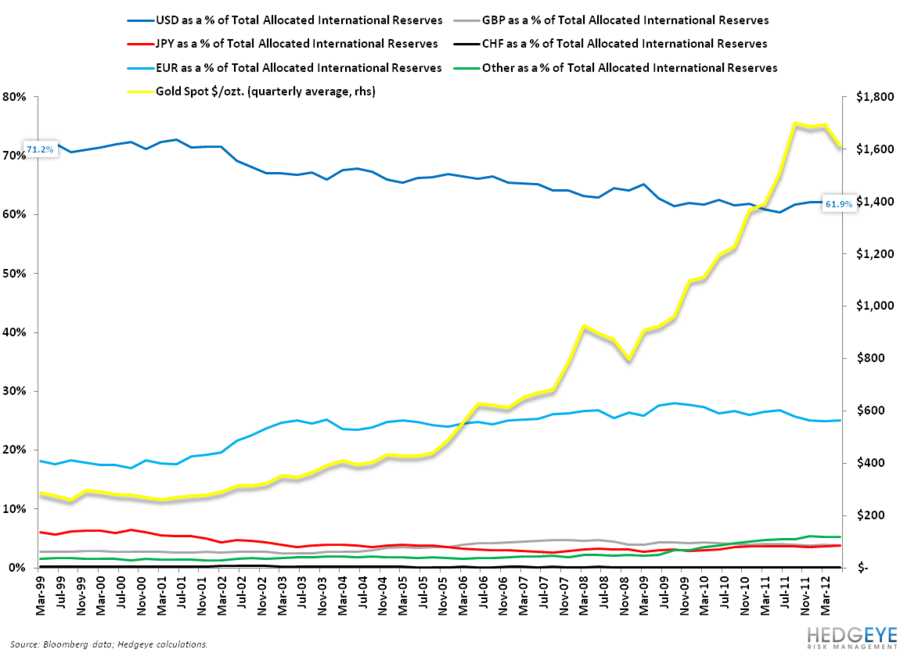

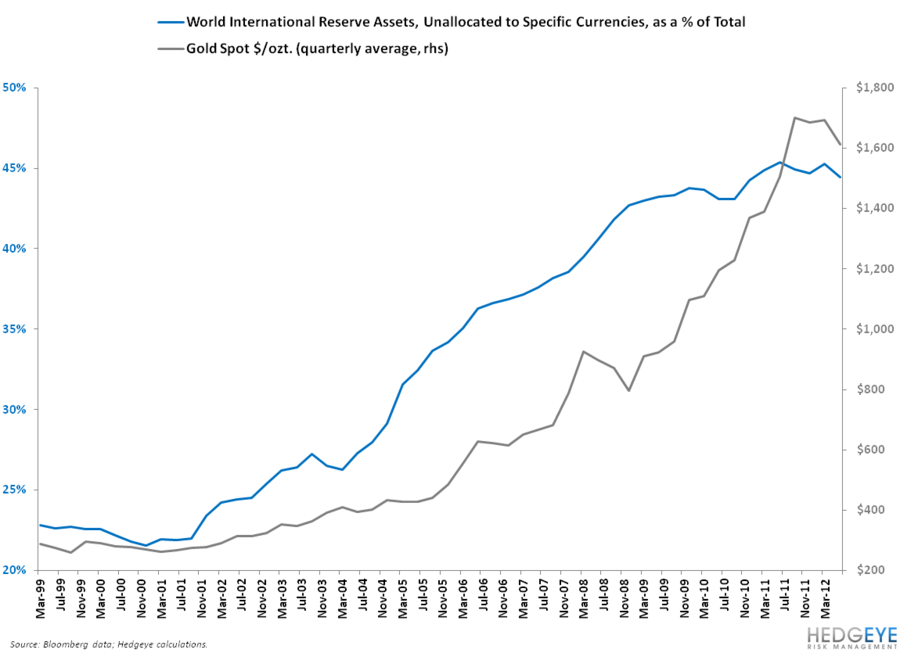

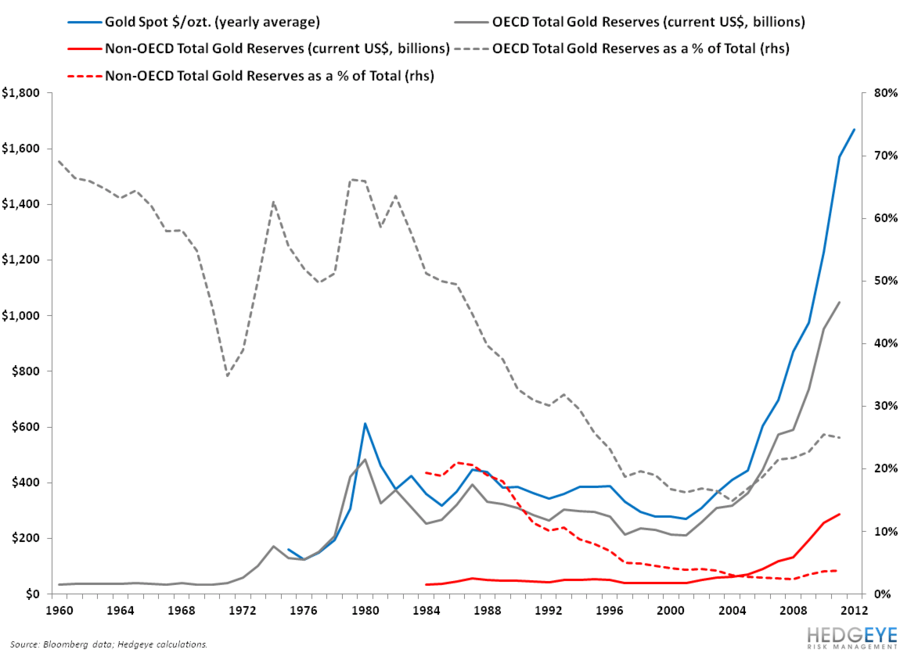

Gold has ripped for over a decade as central banks increasingly diversified out of the primary world reserve currency and into other, more credible currencies, as well as other assets like SDRs and Gold.

We hold the view that credibility within the FX market is 100% relative and ever-changing. The management of foreign exchange is a 24-hour-per-day phenomenon that is consistently anchors on incremental data. Below, we focus specifically on the US because gold and other internationally traded commodities are priced in and settled in USD.

For 10+ years, the stream of incremental data has been a general headwind for the credibility of America’s currency, largely in the form of loose fiscal POLICY and dovish monetary POLICY. That confluence of weak POLICY has created an egregious amount of international money supply that has inflated international reserve assets across both the developed world and non-developed world. Initially, the price of gold appreciated w/o much of a shift in global central bank demand. That changed in 2004 when the confluence of the world’s reserve mangers started to accumulate gold at a rate commensurate with the rate of incremental foreign exchange accumulation. Since 2008 (not ironically when QE1 was introduced), however, they’ve been accumulating gold at a faster rate than incremental FX.

THE LESS-KNOWN KNOWNS

The first major run-up in gold (2004-2008) was occurred as DM central banks began favoring gold over incremental foreign exchange, at the margins. The second major leg up in gold prices came as EM central banks began to do the same (2008-present). This is where the real “juice” likely came from, as EM central banks have increasingly held the lion share of international reserve assets.

The latter point is super intuitive, given that EM economies, on balance, have tended to be more manufacturing and export-oriented in nature (think: China). Additionally, EM central banks have likely aggressively accumulated large amounts of foreign exchange (in lieu of gold, at the margins) over the last 10+ years to resist appreciation pressure on their currencies (think: Chinese yuan and Brazilian Finance Minister Guido Mantega’s “Currency War”).

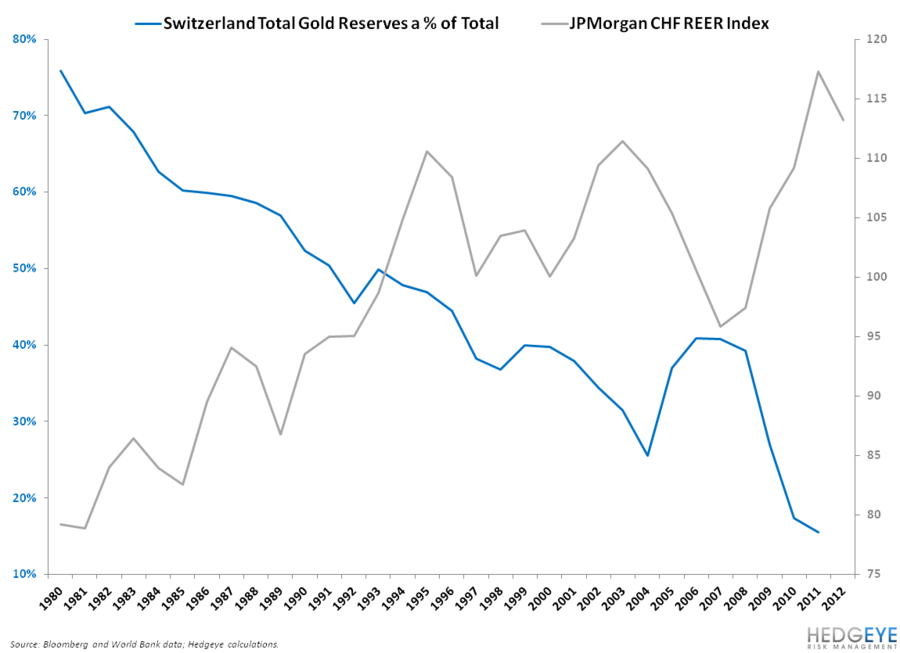

For reference, Switzerland has been doing exactly this (i.e. accumulating foreign exchange at a rate faster than gold) for the better part of 30 years, as the SNB has semi-perpetually combated the specter of a secular loss of competitiveness – which is a real threat given the country’s +42.9% real exchange rate appreciation over that duration. The CHF’s de-facto ceiling vs. the EUR is yet another example of the Swizz central bank being forced to accumulate incremental FX, lest the country suffer the perceived consequences of having a strong currency amid the international “race to zero” in today’s “Beggar Thy Neighbor” global economy.

That brings us to our final point, which is really a question:

Can EM central banks ever really accumulate that much gold – especially relative to consensus expectations that they are poised to be big players in that market in perpetuity?

There seems to be little political will across the developing world to allow for any dramatic currency appreciation – especially with global GROWTH likely tracking in the +2-3% range for the foreseeable future. This means EM central bankers will continue to be forced to daub up large amounts of fiat currency over the long-term, absent a phase change in the global monetary POLICY landscape.

In light of this, it’s important to note that the People’s Bank of China (a key player in the FX reserve accumulation sphere) now views the yuan at/near an “equilibrium level” and they have been using their USD/CNY reference rate as a tool to temper appreciation pressure emanating from the market for several months now. Incremental Polices To Inflate out of DM central banks will force them to accelerate their pace of foreign exchange accumulation if they are going to resist upward pressure on CNY exchange rates from current levels.

What’s new across developed markets is the political will for the Europeans and the Japanese to pursue incrementally aggressive currency devaluation strategies over the intermediate-to-long term. Keep in mind that we haven’t even seen the ECB really go to town w/ unsterilized bond purchases and that the BOJ’s balance sheet is poised to expand to new heights in a variety of experimental manners under the pending LDP regime.

In short, we think Japan faces the risk of a currency crash (peak-to-trough decline > 20%) over the next 12-18 months. Moreover, unless Europe has been magically fixed (are the Greek and Spanish unemployment situations even “fixable”??), the EUR is likely to continue making lower-highs over the long term. In the eyes of the world’s central bankers, the perceived credibility of the JPY and EUR are likely to be materially eroded over the long term, which, on the margin, is positive for other countries’ currencies to the extent they are credible candidates for international reserve management.

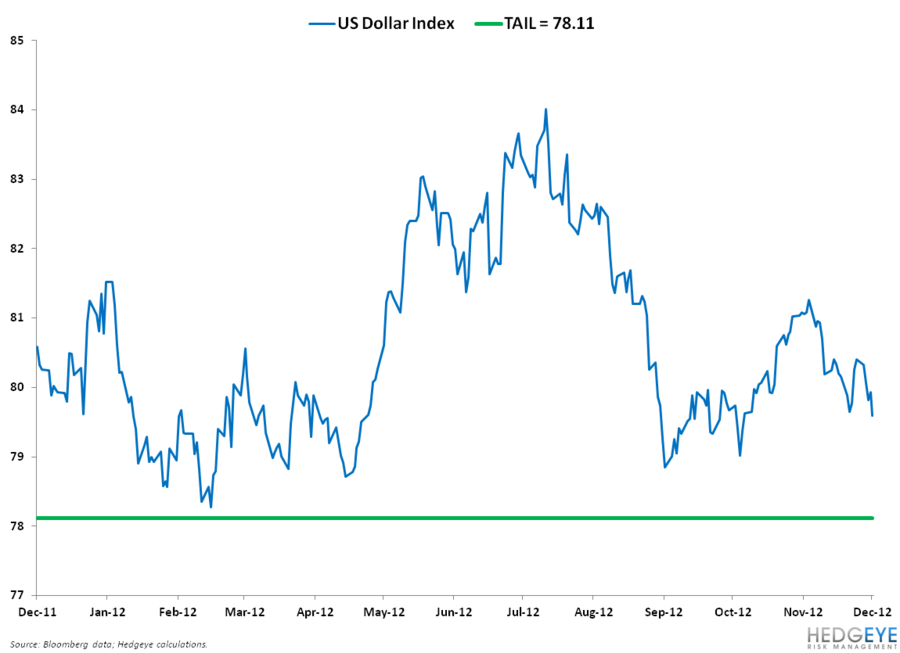

In the aforementioned Global Macro scenario, could we see the USD grind higher against a broad basket of currencies over the intermediate-to-long term? Absolutely – especially if US fiscal POLICY starts to get hawkish on the margin (think: Fiscal Cliff). Perhaps that’s why the US Dollar Index is down less than 100bps YoY, despite the Federal Reserve kicking the ZIRP can down the road 3x in the YTD and instituting perpetual QE – twice in the last three months!

If one is bearish on the US Dollar from here, we can’t even begin to fathom what their next catalyst is, given the USD’s resilience in the face of all that…

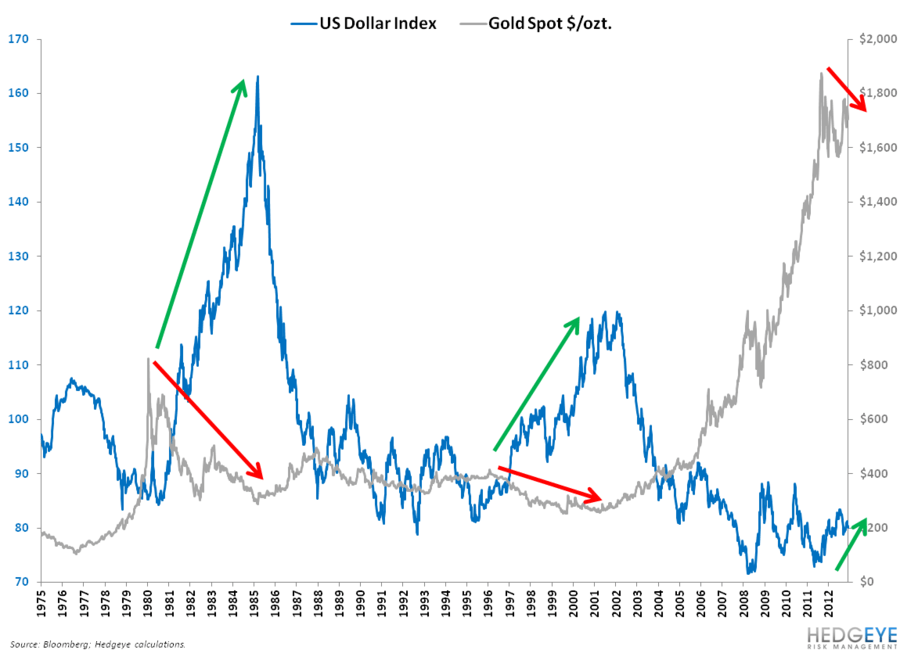

In the past, strong USD has been really bad for gold (early-to-mid 1980’s and late 1990’s). The most recent period of sustained USD appreciation came on the strength of the Balanced Budget Act of 1997, so it’s critically important to avoid underweighting fiscal POLICY as a factor for the market price of America’s currency. If Congress and the White House can figure out a way to resolve the Fiscal Cliff in a sustainable and effective manner (a really big “if”), we could see the US Dollar Index approach the high 80s/low 90s level over the intermediate term. That would not be good for gold.

Our quantitative risk management levels for Gold are included in the chart below. If $1,669 breaks, there’s no true support to the prior closing lows. That’s something to think about as you ponder, “Who’s the incremental buyer of gold from here?” For some, that question sounds more like, “Who can I offload my gold to if and when I want to head for the exits before the crowd does?”.

Gold remains a crowded long for a variety of very obvious reasons – one of which could become less supportive, at the margins, on a sustainable basis.