Current Investing Ideas

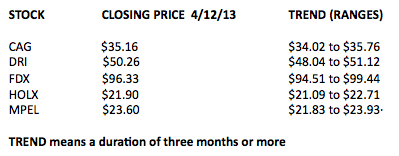

CAG, DRI, FDX, HOLX, MPEL

Investing Ideas Updates

- CAG:ConAgra continues to be one of Consumer Staples sector head Rob Campagnino’s favorite names. While he recognizes that his sector is not a “value play” right now, Campagnino continues to like CAG’s commitment to aggressively increasing their marketing expenditures. This is particularly notable since some of their major competitors trimmed marketing budgets to compensate for higher expenditures, perhaps as a way to beat Wall Street earnings estimates. Campagnino continues to like CAG’s earnings growth potential, which could get a substantial kicker if commodity prices continue to come down. (Please click here for the latest CAG Stock Report.)

- DRI: Restaurants sector head Howard Penney noted March employment figures suggested “less of a tailwind for restaurant sales,” but the sector may have been bailed out by the Bureau of Labor Statistics’ inability to figure out the seasonality affect of Easter falling in March, rather than April. Financials sector head Josh Steiner sees the latest seasonally adjusted employment as the start of an uptrend that should run through the summer. This should let managements across the casual dining sector breathe a sigh of relief. Even Darden’s management should get a lift – though Penney continues to believe DRI management “cannot effectively manage the business as it exists today.” Rather than pose a negative, Penney believes this “rolls out the red carpet for an activist.” (Please click here to see the latest DRI Stock Report.)

- FDX: Industrials sector head Jay Van Sciver continues his patient advocacy of FedEx, challenging the bears who are attacking the minutia of their latest earnings release. “Too much data can be toxic to clear thinking,” says Van Sciver, who notes “the market ascribes little value to any FDX business other than FedEx Ground.” He says the opportunity comes into sharper focus when you look at simple numbers. FDX trades at an equity value-to-sales ratio of about 0.67, compared to UPS at a ratio of 1.56. If, as Van Sciver believes, FDX makes even small steps towards improving express margins, simple multiple adjustment could mean a big boost in stock price. (Please click here to see the latest FDX Stock Report.)

- HOLX: Health Care sector head Tom Tobin presented groundbreaking analysis that indicates we could be on the brink of an upsurge in the birthrate. This has major implications for Hologic, the leading provider of mammography equipment, since HPV/PAP testing is a common part of prenatal screening. If, as Tobin’s work indicates, we see as much as 1.4 million additional births in the coming three to five years, HOLX would be a natural beneficiary. Perhaps more important in the near term, Tobin sees acceleration in doctor visits (“physician utilization”) and in the mammography segment in particular. (Please click here to see the latest HOLX Stock Report.)

- MPEL: Gaming, Lodging & Leisure sector head Todd Jordan says the recent swoon in Macau gaming stocks could be a head fake. Macau stocks recently dipped 5%, largely over concern about the latest Bird Flu deaths. But Jordan notes that during the 2009 Swine Flu scare, “gross gaming revenues actually continued to improve.” March was a record month for Macau, notes Jordan, andMelco Crown Entertainment largely participated in the increase in revenues. (Please click here to see the latest MPEL Stock Report.)

Macro Theme of the Week: All Together Now! Dollar, Commodities and Stocks in Harmony

Last week (“Bad News Bulls”), Hedgeye CEO Keith McCullough said weak employment figures could be a head fake and the dollar could continue to strengthen, while commodities continued to drop. Sure enough, this week’s jobs data came in “surprisingly” strong as the Bureau of Labor Statistics can’t seem to get those pesky seasonally-adjusted numbers to behave in those funny years when Easter comes in March, instead of April. Financials sector head Josh Steiner cautions that seasonally adjusted labor market data is likely to soften on the margin through the summer just as it has over the prior three years, but sees this as a buying opportunity since the non-seasonally adjusted unemployment data continues to strengthen.

The markets are making fools of Washington policy makers as the strengthening dollar continues to make a series of higher lows and higher highs, versus its 40-year low in 2011 – and commodity prices continue to make a series of lower highs and lower lows, versus their 40-year highs which likewise occurred in 2011.

You can draw a neatly diverging chart shaped like the “less than” sign [<] with the dollar running to the upside, and commodity prices falling away. That formation equals Real Purchasing Power for the cash in your pocket. The US Energy Information Administration says that, on a nationwide average, gasoline prices at the pump are 33 cents lower today than a year ago. It has been estimated that a one-cent change in gasoline prices translates into one billion dollars more or less flowing through the economy. Is there effectively a $33 billion tax cut available for spending today? Stock prices say “You betcha!”

What does this mean for your investment portfolio? We recall the old Wall Street adage “Buy on the expectation, sell on the news.” The strong growth in the economy was not widely anticipated. Now that it’s here, the coming increases in consumer spending could be the News You Sell On. We recommend short-term traders take profits at these levels and re-enter on pullbacks, while longer-term holders should be willing to live with a bit less euphoria while waiting for strengthening employment and consumer spending to work their way through the economy.

Sector Spotlight Retail: Learn From the Mistakes of Others (You’ll Never Live Long Enough To Make Them All Yourself)

New York’s colorful Mayor Fiorello LaGuardia was quoted as saying “When I make a mistake, it’s a doozy!” Retail sector head Brian McGough found himself in the “Oops!” box this week when he pulled the plug on his bullish call on JCP (JC Penney), seeing the stock drop significantly as the board of JCP fired CEO Ron Johnson. Should McGough have stayed on the short side?

Shoulda, woulda, coulda. Being wrong, and taking the consequences, is what Capitalism is all about. At Hedgeye, we look at our own losing ideas as our best learning opportunities.

McGough was the lone bear on the stock way up at $40 and rode it all the way down to $19 before doing a 180 last month, in the face of mounting bearishness across the investing community. McGough believed the key was a stabilizing top line in the second half of 2013 with the support of enough avenues to mitigate the likelihood of a liquidity crunch – all in the context of extreme bearishness in the investment community.

Today, with Johnson suddenly out, McGough is staying away from the stock altogether. There could be more downside to come, cautions McGough, even if management does absolutely everything right. Which he says is not likely to happen.

McGough issued a call to fire the JCP board, saying getting rid of Johnson now is one doozy of a mistake – “The Fastest Path To Chapter 11” McGough wrote recently. Speaking with CNBC’s Maria Bartiromo, McGough said “Either fire him six months ago,” when it became clear the pricing strategy wasn’t working – or six months from now, if the new retail strategy flops. But the board apparently wasn’t willing to let Back-to-School drag into Christmas with Johnson at the helm, so they replaced him with former CEO Mike Ullman – the man Johnson replaced in 2011.

Here are a few key points:

- Wall Street hates Johnson – but key JCP key vendors love him. McGough says there is a real risk they may walk away if new CEO Mike Ullman does not succeed in regaining the support of the vendor community, some of whom are already incurring financial penalties from trade intermediary CIT Group for selling into JCP.

- The board replaced Johnson with former CEO Ullman – whom Johnson replaced in 2011. Having been once dumped, will Ullman have the traction to accomplish anything? Is it possible that JCP’s board couldn’t find a qualified retail executive to take over?

- … a qualified retail executive who wants to work for Bill Ackman, the brash hedge fund manager currently embroiled in a very public shouting match over Herbalife. Ackman was the prime mover behind hiring Johnson – and dumping Ullman. Did Ackman have a change of heart, or did the board usurp his decision making? Either way, corporate governance at JCP is a shambles. Desperate times may call for desperate measures, but that doesn’t mean you should be desperate with your cash.

- It’s critical to “rally the troops” at JCP, and Johnson never clicked with the employees (especially given that he fired thousands of them). As CEO and star turnaround expert of the giant retail chain, Johnson still commuted from his home in California, and only spent three days a week on the ground at JCP’s Texas headquarters. But can Ullman rally anyone? His first steps will probably be a return to the Good Old Days – coupons, “attention, shoppers!” specials, and a re-re-branding of the company from “JCP” back to “J.C. Penney & Co.” Ullman has to get the new / old / new retail program in place in time for back-to-school. It’s already April. In the world of retail, that’s not a lot of lead time.

- Will the 66-year old Ullman step aside once they find a real retail genius (which Johnson supposedly was)? Will JCP settle the Martha Stewart matter? This is more than a distraction, as JCP has merchandise sitting in warehouses that they can’t put on the sales floor until the case is resolved. Can the board possibly regain the trust of management, employees, Wall Street – not to mention shareholders?

- Ron Johnson did something very unusual for a CEO: he took a risk. He will not get a $100 million severance bonus – or even one million. He bet on himself and lost. Is this a “doozy” of a mistake? At Hedgeye, we call it “capitalism.” Even Hall of Fame pitchers lose games. It doesn’t make them less magnificent at what they do. There’s already talk of Johnson being called back to Apple – he’s out, but for sure not down.

- We can’t say the same about JCP.

Investment Term: Bull Market

Some say the terms “Bull” and “Bear” refer to the bull who charges straight ahead, versus the bear who digs a hole and hibernates. Others say it comes from the vigorous upward thrusting of the bull’s horns and the hard downward swipe of a bear’s paw. Either way, Wall Street pros – and not a few amateurs – have traditionally surrounded themselves with trinkets, bookends, cufflinks, and giant bronze statues in the form of these iconic beasts.

The term “Bull Market” is not reserved for stocks. It can refer to any sector, and often there will be a bull market in one asset class that is related to a bear market in another. Think of the common historical divergence as stocks go up, while interest rates, oil and gold go down.

Market watchers follow trends over the short, intermediate, and long term. At Hedgeye, we track our CEO Keith McCullough’s proprietary TRADE, TREND, TAIL metrics (see definitions of TRADE, TREND and TAIL at the end of the newsletter). Standard analysis looks at the Secular Trend (anywhere from five to 25 years), and the Primary Trend (one year or more). The Secular Trend is broad momentum across an entire asset class, and is at any given moment composed of interwoven Primary Trends, much like the crisscrossing threads of an intricate tapestry.

In a Secular Bull Market, Primary Trends feed off one another in a virtuous cycle: increases in consumer demand drive Retail stocks, demand for inventory drives Manufacturing, stimulating Transportation to bring products to the market. Increased consumer demand drives construction (for manufacturing plants) and companies that produce raw materials for manufacturing. Employment drives demand for housing, for financial services, and ultimately for leisure, travel, and the host of companies – from maternity care to pet grooming – that serve growing families. Primary Trends springboard off one another, making up the fabric of the Secular Trend.

Most observers agree the US experienced a Secular Bull Market in stocks from 1983 through 2000 or beyond, and disruptions such as the Crash of 1987 – or even the prolonged 2000-2002 collapse of the DotCom Bubble – are seen as speed bumps that may have rattled the passengers good and proper, but didn’t stop us getting to our destination.

So what exactly is the destination in a bull market?

It increasingly seems the ultimate destination of a Bull Market cycle is a crash, precipitating a prolonged Bear Market. For smart investors, the goal should not be closing one’s eyes and waiting for impact. If the Boom-and-Bust cycle is really here to stay, and crashes are inevitable, that’s all the more reason your goal should be taking profits and socking it away in savings, or in counter-cyclical assets. As Keith constantly reminds us, market tops are processes, not points.

Fear of “leaving profits the table” causes many investors to hold on past the Bull Market top. As they see their profits slip, they panic and hold tighter in desperation to get back those last few points. As their stocks decline further in value, it becomes a frantic exercise of Not Taking A Loss. Finally, when the investor has “round tripped” their portfolio – holding on all the way up, and all the way down – the objective is to get even.

Legendary investor Bernard Baruch (1), stock market wizard, philanthropist, statesman and advisor to presidents, famously said “I made my money by selling too soon.” Sound advice from a successful man – who also said “the main purpose of the stock market is to make fools of as many men as possible.”

- TRADE: analyzes forces that influence risk /reward probabilities over a duration of three weeks or less;

- TREND: analyzes those same parameters over a duration of three months or more;

- TAIL: looks out to a duration of three years or less.