Conclusion: There's been no shortage of reasons for us to be negative on BBBY, and it's underperformed accordingly. But the risks are passing, and there are emerging factors that cause us to model EPS/EBITDA above consensus. This is when being cheap actually starts to matter. If our model is right, this is a $90 stock in 12-18 months.

DETAILS

We’ve been bearish on BBBY for much of the past year, as we couldn’t get over a) a slowing core business, partially due to increased pressure from on-line competitors, b) acquiring businesses (Cost Plus, Linen Holdings) to mask weak organic growth, c) integration risk associated with those businesses, d) BBBY’s office relocation in 2H, and the associated headcount/execution risk, and lastly e) stepped-up levels of capital investment to build-out new facilities, which we thought would erode returns.

Ultimately, BBBY was worth staying away from, as it disappointed in five of its past six quarters. But things are changing on the margin. Specifically…

a) While still anemic, the rate of growth in the core business has stabilized and is picking up. Comps in the latest quarter were only 2.5%, but they accelerated sequentially to 4.7% (from 2.9%) on a 2-year run rate.

b) Housing prices up 11% year-to-date. That’s not exactly a newsflash to anyone keeping up with the market, but it definitely flies in the face of the ‘bearish consumer spending’ call that is fueled by the payroll tax hike and sequestration. The degree to which this will help discretionary spending is debatable, but historically, every 1% change in house prices resulted in 6-8bp increased consumer spending – typically on a one-year lag. The point is that housing alone could offset the payroll tax hike (42-64bp hit to GDP). Tack on commodity deflation – which we think is in the cards – and it could all add up to be very bullish for the consumer, and for BBBY.

c) The two acquisitions and the headquarters transition have passed through the riskiest periods, and the company emerged reasonably unscathed. It is now at a point where it can grow square footage at CPWM, and optimize SG&A and working capital.

d) BBBY is past the halfway mark in a mini capex bubble to fuel non-store-related corporate projects. We should see a significant slowdown in the rate of capex in 2014.

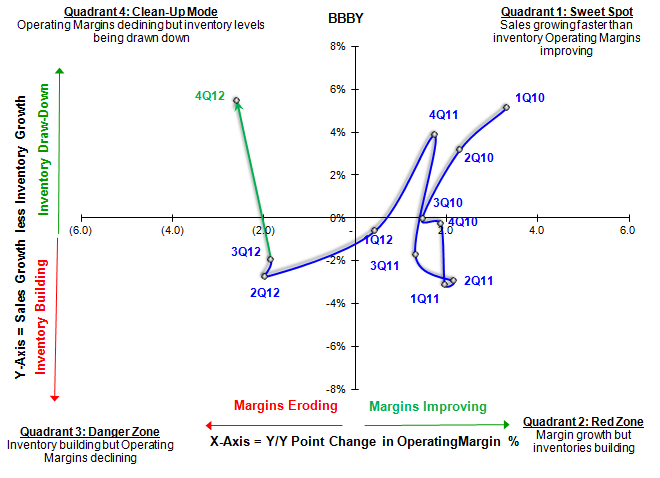

e) Inventories look solid, as the company had the best SIGMA move we’ve seen out of any company year-to-date. These moves are usually coincidental with some iteration of an upward stock price move. But they are just as often a setup for a greater move in quarters to come.

The stock obviously realizes this to an extent, as it is up 20% year-to-date versus the S&P Retail Index at +16%. Despite the move, it’s underperformed the retail index by a whopping 29% over the past 12 months.

The point here is that BBBY remains an extremely high return company with a 44% RNOA, and it is trading at 13x earnings and 7x EBITDA. ‘Cheap without a catalyst’ usually means nothing to us, but we think that while the Street ended up with estimates at the higher end of guidance, they’ll end up being on the low end of what BBBY will ultimately print. If our model is right, then we’re looking at $2.2bn in EBITDA in 2014 and $6.12 in EPS. Every EBITDA multiple w BBBY equals $10 in the stock price. A 20% year-to-date might sound rich. But 9x $2.2bn in EBITDA is a $90 stock. That’s another 36% upside from here.