This note was originally published April 11, 2013 at 11:15 in Financials

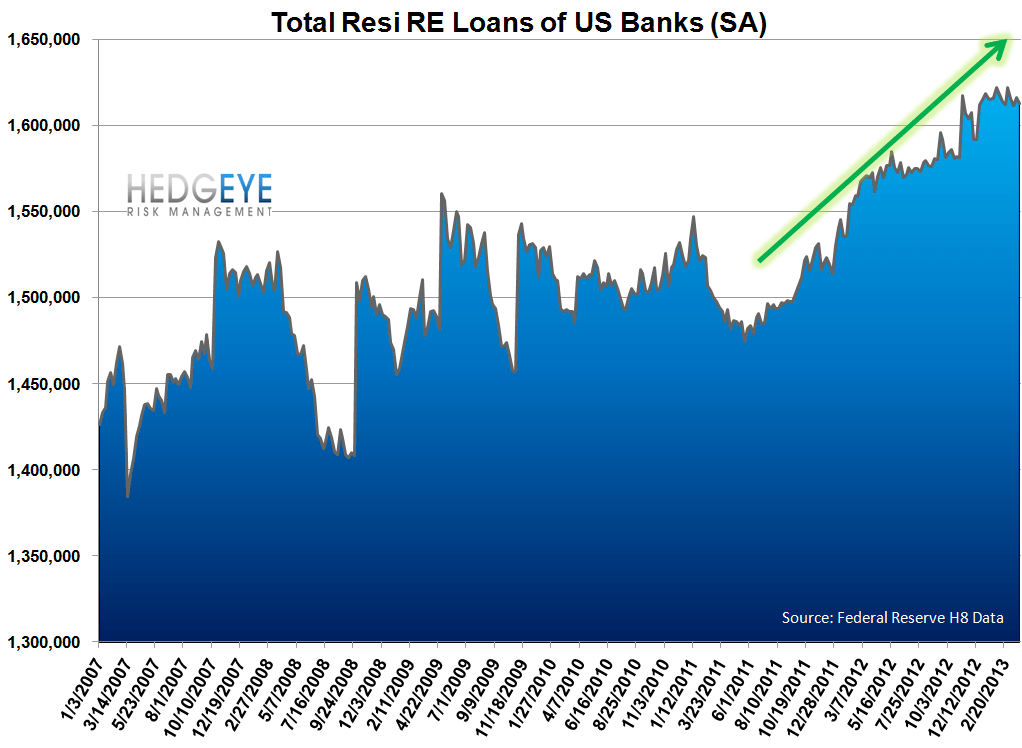

Overall, we expect this earnings season will be lackluster for the banking sector. Outside of ongoing credit quality improvements and a recovery in housing, there will be little good news for management to discuss. Top line pressures will become more notable, while credit tailwinds, vis-a-vis provision expense/reserve release, will be simultaneously fading. Offsets to these two pressure points will be expense reduction initiatives and falling sharecount from active repurchase programs. Another offset may be relatively upbeat guidance with respect to a reduction in future costs, both legal and operational, relating to legacy mortgage troubles. We think 1Q results are likely to set expectations fairly low for the duration of 2013.

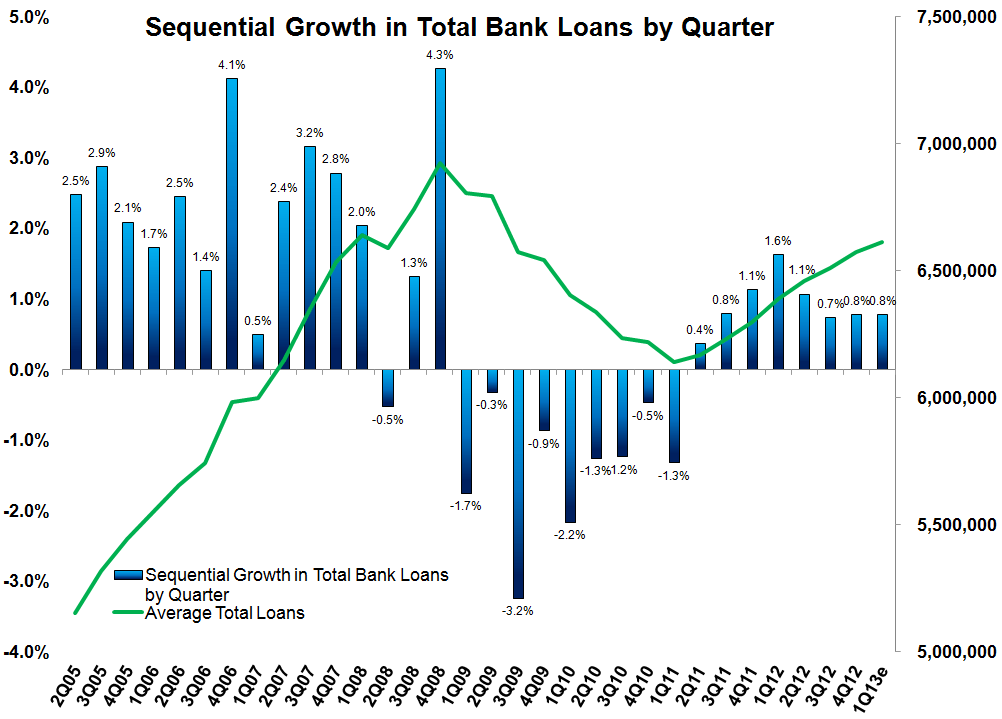

- Loan Growth - Status Quo - Overall, loans grew by 0.8% QoQ in 1Q13, which was flat with 0.8% QoQ growth in 4Q12.

- Margin Headwinds Ongoing - 1Q13 saw some relief in the average yield spread QoQ, but banks have largely run out of room on the funding side and are now facing unmitigated earning asset yield pressure. CBSH is a good example today with NIMs down 28 bps QoQ vs. expectations for down 11 bps.

- Credit - Fading Tailwinds - Credit is still improving, but provision expenses have largely flattened out. The odd silver lining may be that with little to no loan growth there's no need to grow provision expense.

1Q13 Revenue: Expect To Be Disappointed

* Loan Growth - Total loan growth appears to have grown at 0.8% QoQ, which was roughly flat with growth in 4Q12, based on seasonally-adjusted H8 data. That said, The overall trend in loan growth remains lackluster. Loan growth through 1Q12 had been sequentially accelerating up to a peak of +1.6% QoQ, only to then decelerate in 2Q12 and 3Q12 and remain roughly flat since then. Overall, we don't see this as a notable source of strength for the sector.

* NIM - Net interest margin pressure will persist this quarter in spite of the sequentially improved yield spread. The sector's ability to further reduce funding costs continues to decelerate. Meanwhile, pressure on interest-earning asset yields persists. If Commerce Banc is any indication this morning, the sector is not conservative enough on NIMs. CBSH saw NIMs decline 28 bps QoQ vs expectations for 11 bps. Given the relatively modest expectations for NIM compression this quarter, roughly 5 bps Q/Q, we would expect to see more banks than not disappoint on this front. On the other hand, CBSH shares are down less than 2% this morning,

* Non-Interest Income - Mortgage banking is the primary driver of Q/Q change here, and the news isn't great. Application volume in 1Q13 was down 6% QoQ, but primary/secondary spreads have compressed by ~20 bps Q/Q from 1.16% to 0.96%. Taken together, this implies sequential declines of roughly 21% in production revenue. There will be some offset to this from the servicing side as rates ended the quarter a bit higher than where they started. A small silver lining is that as of the latest data, spreads have modestly re-widened to 106 bps.

Joshua Steiner, CFA

203-562-6500

jsteiner@hedgeye.com