“Energy itself can neither be created nor destroyed, though its many forms can change.”

-Eric Chaisson

That’s pretty much the first law of thermodynamics. The second law is that there is a price that gets paid when forms of energy change – it’s called entropy.

“Entropy is also a measure of the disorder (or randomness) of a system… some of these basic thermodynamic ideas date back to 1824, when a young French army officer, Sadi Carnot, sought to understand the rudimentary elements of an ordinary steam engine… engines work because of a temperature difference…” (Cosmic Evolution, pg 17)

In market speak, you might insert words for entropy like “rip” or “meltdown” – but, to me at least, it’s all about the same thing – rates of change. And for those of us who aren’t on the Federal Reserve’s inside information leak-list, I guess that’s the best we can do. Think for ourselves and do our own work in a transparent and accountable way.

Back to the Global Macro Grind…

“Literally, thermodynamics means movement of heat” (Chaisson). That’s why I call my rants on Twitter #TweetHeat. And oh were the #PTCs (Professional Top Callers) feeling it yesterday.

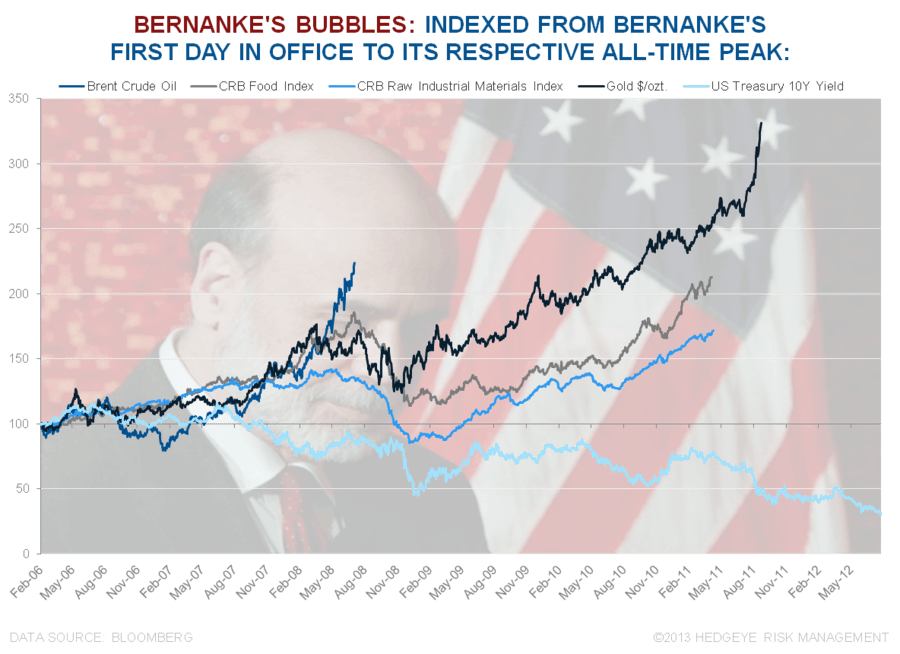

No matter what your market views have been for 2013, here we are – at all-time closing highs for the SP500 (+11.3% YTD at 1587). Consumption stocks continue to lead the charge (Healthcare (XLV) +18.82%, Consumer Discretionary (XLY) +13.13%) and Commodities continue to get hammered.

To review our non-consensus bull case for US Growth (and US Consumption Equities):

- #StrongDollar continues to make a series of higher-lows and higher-highs (vs its 40yr low in 2011)

- #CommodityDeflation continues to make a series of lower-highs and lower-lows (vs their 40yr high in 2011)

- US Consumption Growth occurs when the real purchasing power of the US currency rises

Pretty simple really. Wouldn’t it be nice if the President of the United States (either Bush or Obama) A) understood these basic concepts and/or B) had financial advisors who made these fundamentals crystal clear to them instead of focusing on leaking whispers about their spurious economic policy conclusions to the #OldWall?

Sadly, Margaret Thatcher passed away this week. She taught Ronald Reagan a lot about the real purchasing power of a currency and the real impact a political leader can have with her people (trust) by calling out all the conflicted and compromised bureaucrats. She was a patriot. God rest her soul.

We made some sales yesterday (I don’t like buying on green), but what would really get me to change my economic and market views?

- If Bernanke debauched the Dollar again

What would happen if Obama let that happen?

- Dollar Down = Commodities Up

- Commodities Up = Food and Gas Prices Up

- Food and Gas Prices Up = US Consumption Growth Down

Again, it’s not that complicated. Really.

What is complicated is comprehending A) Bernanke’s “transparency” model (leaking information selectively? #embarrassing) and B) how he has the “best inflation track record of any central banker since World War II” (that’s what he whined to Senator Bob Corker, under oath, earlier this year after Corker called him the biggest dove in modern history).

Bernanke has been wrong on this growth forecasts at least 70-80% of the time since he took over at the Fed in 2006. Remember, he got the job with his thesis of the “Great Moderation” (he was talking about volatility, after it hit generational lows). Not that he wants to talk about that anymore (his Fed has overseen the Greatest Volatility in US market history).

Maybe we should call his legacy The Great Transparency? Nah. Maybe Obama should put Bernanke on trial. Give the man his fair share already. Please have him explain (with someone who isn’t a market moron asking the questions):

A) How leaking information selectively = #transparency

B) How the all-time lows in the US Dollar (2011) = #trust

C) How the all-time highs in Commodities (2011) = #accountability

To be balanced, the all-time highs for Food Prices (globally) didn’t happen until 2012 (Gold and the CRB index topped in 2011). So there’s still a fighting chance that Bernanke’s final rip to all-time bubble highs comes in either his reputation amongst people who get paid to believe him or in the US Bond market.

Q: (in this order) Housing, Commodities, Gold, Food, Treasuries, and now US Stocks (again). He Who Saw No Inflation at the all-time highs in all of those prices – what does he really see? Or like any un-elected and un-accountable central planner with a confirmation bias, does he see what he wants to see?

What he’s hiding from you is what you really don’t trust. And you shouldn’t. Fortunately, the other side of his storytelling doesn’t cease to exist. The popping of his Commodity Bubble is becoming self evident. That’s a real-time Tax Cut. That’s good. So will be the inevitable leak that you are no longer getting 0% on your hard earned savings account.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, USD/YEN, USD/EUR, UST10yr Yield, VIX and the SP500 are now $1, $102.39-107.38, $3.29-3.45, $82.24-83.34, 97.62-101.63, $1.27-1.31, 1.71-1.88%, 12.04-14.41, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer