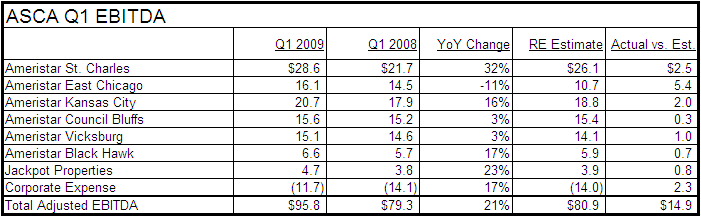

We wrote about the potential for a big quarter in our note "ASCA: INCENTIVE TO BLOW OUT Q1". However, the quarter was even better than our most optimistic scenario. Property EBITDA beat us at every property and increased YoY at every property, save East Chicago. Competing with Harrah's used to be a tough business. All together, corporate EBITDA increased 21%. We're in a recession?

Margins were the story as revenues were just flattish. Certainly, ASCA had an incentive to beat the quarter, as we discussed in the 4/12/09 note. ASCA will be in the market to raise subordinated debt or extend the maturity of its credit facility. The current credit facility expires in November of 2010. Our thesis was that the credit markets needed to be pried open and a big quarter would be a good start. Regional gaming credits trade at a big spread to other similarly leveraged consumer sectors because they are, well, gaming. MGM, Station, Harrah's, etc. continue to weigh on the sector. The "collusion" of strong regional gaming earnings releases (ASCA, PENN, PNK) could change that.

ASCA closed up 21% on the day, and rightfully so. We are now projecting EPS and EBITDA of $1.48 and $379 million, respectively, for 2010. We took a hack at EV/EBITDA as a valuation tool (4/20/09 - "GAMING REGIONALS: THE FALLACY OF EV/EBITDA") since it doesn't incorporate refinancing risk or increasing cost of debt for companies with nearer term debt maturity or covenant issues. For ASCA we've incorporated the incremental borrowing costs of a refinancing into our 2010 estimate so we will look at both EV/EBITDA and FCF yield for the stock.

After the big move in the stock and a significant hike in our EBITDA and FCF estimates, the stock looks like it is valued pretty close to perfection. EV/EBITDA and FCF yield on our 2010 projections is 6.6x and 14%, respectively. In the 4/20/09 note we pegged fair value at 6.9x and 15%, respectively. Multiples could go higher and we are open to debate, but we'll sit tight for now.