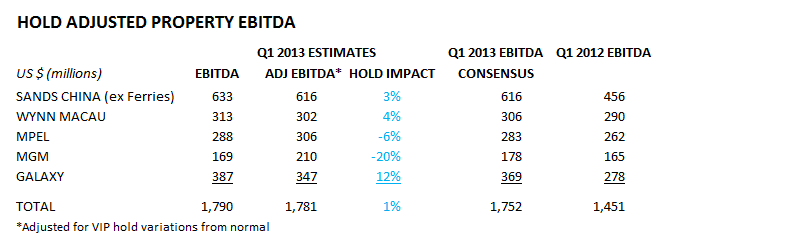

Recently updated Q1 Macau EBITDA and hold adjusted EBITDA projections – MPEL looks great

Q1 earnings season should be decent for the Macau operators although there are only 2 real standouts – both were impacted by low hold. On a hold adjusted basis, which is what we care about, MPEL and MGM Macau performed very well in Q1. Wynn Macau is the only property that looks like it could post a slight miss relative to consensus but that would be on a hold adjusted basis as our projection for actual EBITDA exceeds consensus slightly.

MPEL remains our favorite name in the space with the catalyst of a terrific Q1 earnings release looming. More importantly, the stock remains incredibly inexpensive relative to most Macau names and could be ripe for a 2-3 multiple turn increase in its EV/EBITDA valuation. As we wrote about in our note “INVESTABLE MPEL” on 03/21/13, MPEL should transition from a trading vehicle to a core long-term holding for many long only investors which should help inflate the multiple to something more realistic: 11-12x (post-opening of MSC).