“We can’t afford to risk a downturn, no matter how much inflation.”

-Richard Nixon

Nixon’s legacy is Watergate. Trivial Pursuit presidential history doesn’t yet appreciate how horrendous he was for the US economy. On matters of economic policy, this guy was easily the most conflicted, conniving, and compromised president in the post WWII period.

If you’d like to re-educate yourself on the what, when and why (Nixon’s economic policies), chapter 4 “Gamble” of Volcker: The Triumph of Persistence is a beauty. The aforementioned quote came from Nixon during his 1972 re-election campaign.

Prior to that (1971), Nixon had already abandoned the Gold Standard and explicitly devalued the US Dollar. On the fiscal policy side, he hired a Democrat from Texas who polled well (John Connolly) to be Treasury Secretary. Connolly wrote later, “I was not an economist; I had really never studied monetary affairs. My experience with fiscal issues was limited largely to a familiarity with Congress…” (Volcker, pg 74)

Back to the Global Macro Grind…

Why do we care about the context of politicized currency devaluations (and the local inflations they drive) this morning? Well, because the only opportunity the US economy has to grow (on a real inflation adjusted basis) is through pervasive Commodity Deflation. It’s a Tax Cut.

To be balanced, cracker jack economists who have never traded a market in their life (i.e. don’t understand price expectations) want you to believe that currency devaluation will give you the elixir of an exported life. Now that the Japanese Yen is crashing (-24% from where we made the short call in 2012), they’ll have to let us know how that is going for the Japanese consumer who isn’t levered long Nikkeis.

The biggest Global Macro calls for 2013 YTD have been centered squarely on understanding the causal impact central planners have on their domestic currency:

- Get the central plan right, you get the currency right

- Get the currency right, you get the correlation right

- Get the correlation right, you get the money

“Show me the money!” –Tom Cruise

To review, the US Dollar has been strengthening ever since Bernanke tried to promise to print to infinity and beyond (SEP2012):

- MONETARY POLICY: Since, on the margin, market expectations for an iQe5 upgrade have been crushed (see Gold chart)

- FISCAL POLICY: after plenty of political spending wants, the US actually implemented marginally hawkish spending cuts

Again, if you get policy (monetary and fiscal) right, you’re going to likely get the local currency move right. On the margin is what matters most in macro, and when you combine marginally hawkish domestic policy with relatively dovish competing policy (Japan), ta-dah!

Japan’s currency devaluation is very easy to understand (primarily because Japan’s #PoliticalClass is doing precisely what America’s did):

- MONETARY POLICY: hit CTRL+P (print) and step that Japanese debt monetization up to 50 TRILLION more Yens (a year)

- FISCAL POLICY: get the LDP to take the Upper House in this summer’s election and implement “spend your brains out 2.0”

In other words, even if we are dead wrong on the USA’s marginal policy shifts in 2013, we could be right on our #StrongDollar via the rate of change in Japanese policy. Layer on some European Marxism onto the Euro, and I have myself quite a Keynesian treat.

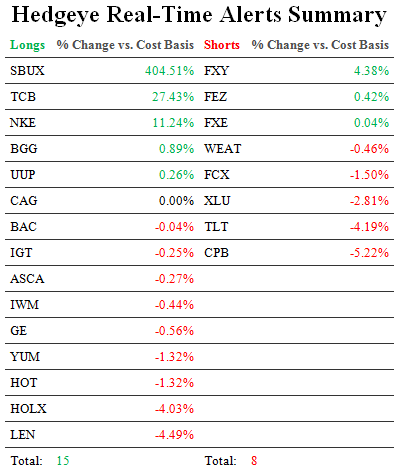

Hedgeye Playbook: how do you make money on this?

- Long US Dollars vs Short Yens

- Short Commodities (they have hyper high inverse correlations to #StrongDollar)

- Long Asian and US Consumption Equities

Some of our competitors can pop this in their next report. “Last night the Chinese reported more of the same on this front. #StrongDollar = Down Food Prices (globally) = Down Inflation (for countries that have a US Dollar peg).” Chinese CPI fell from 3.2% in FEB to 2.1% in MAR – and yes, that is better than a bad thing for people who don’t take government car service to work and have to eat.

I shorted Wheat (WEAT) on the bounce yesterday (unlike trying to call tops in the SP500, it’s always easier to short things that have already started going down – Wheat prices are down -8.4% YTD). Corn and soybean prices are down -9.3% and -2.9% YTD, respectively.

Brent Oil is down -5.7% YTD – but seriously? Who cares about these YTD Commodity Deflations when you can look at how epic they’ve been since Wall Street front-running Bernanke on Commodity prices ended (in food prices especially) at their all-time highs of September 2012? On a 6 month basis, Corn and Wheat are down -14.6% and -17.2%, respectively.

Nixon had it wrong – so did Charles de Gaulle, Jimmy Carter and George W. Bush. President Obama, like Clinton, has a choice on monetary and fiscal policy in his second term. Will he risk the Big Auto lobby for a weak currency? Folks, we need a #StrongDollar and Commodity Deflation. Oh yessir – Yes We Can.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and SP500 are now $1, $103.19-108.02, $82.42-83.39, 95.23-99.31, 1.71-1.83%, 12.21-14.43, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer