How Many Investors Does It Take To Change A Lightbulb? – Quantifying psychological drivers of global economy

Hedgeye hosted an Expert Call today with Dr. Richard Peterson, a psychiatrist who also trained as an electrical engineer. Dr. Peterson has rolled his psychological expertise and quantitative skills into a unique specialty in behavioral market economics. He is the author of Inside the Investor’s Brain and founder and CEO of MarketPsych Data, where he leads a global team of ten brilliant analysts with diverse expertise developing quantitative models using emotional indicators to identify market trends.

You’re So Predictable!

Dr. Peterson’s work as a psychiatrist showed him there are patterns to human behavior. His work developing trading algorithms showed that there are patterns in markets. And, since markets are made up of decisions made by human beings, it wasn’t long before Dr. Peterson started to identify market patterns based on the emotions that go into our decision-making.

In brain scientific terms (don’t worry, this is all we’ll include), strong emotions tend to shut the cortex – the “rational brain” – out of the decision-making system and turn everything over to the amygdala – the instinctive “animal brain.” If you think this probably leads to poor decision-making, Dr. Peterson would agree 1,000%!

MarketPsych Data, founded in 2004, has developed a massive database of global sentiment, using data derived from social media: blogs, Twitter, Facebook, and a plethora of global forums. They combine sentiment with reported news to identify trends, asking modeling questions like, How do most people view a political development, and how will that affect a nation’s currency?

MarketPsych’s database draws information from over two million actively monitored news and social media sites, going back to 1998. It covers over 3,000 sentiment points and individual topics relating to 40,000 separate assets or entities. The data spans 200 countries, 60 commodities, 30 currencies, and 5,000 individual public companies in 40 different industries. MarketPsych’s data output is produced in a series of proprietary indices distributed under license through Thomson Reuters, and available by subscription.

If It Feels Good – Don’t Do It!

The big surprise – or not – in Dr. Peterson’s presentation is, whatever you feel like doing, you’re probably wrong.

As laid out in highly readable detail in his book, Dr. Peterson explains that most investors are unconsciously driven by emotions. In his research, Dr. Peterson asks two questions:

1) Why are people non-rational in their decision making? And;

2) Can we change their approach?

It’s a twist on the old joke about psychiatry: How many investors does it take to change a limit order? The limit order has to want to change.

MarketPsych’s global team of experts find certain types of news stories spark strong emotions. Stories around vivid events, with potentially catastrophic outcomes, trigger powerful emotions, especially fear and anger. And, since the newsmedia report nothing but Vivid Events with potentially Catastrophic Outcomes, Fear and Anger are rampant.

Which is bad for your investment portfolio – but very good for Dr. Peterson and his clients.

Dr. Peterson’s work – and other work available in such recent bestselling books as Thinking Fast and Slow, by Nobel Prize-winning behavioral economist Daniel Kahneman – indicates just how delicate the brain / emotion link is, and how little it takes for the emotions to completely take over our decisions. Experiments indicate that even a random fleeting glimpse of a photograph of a happy, sad or angry face can have a huge impact on a person’s subsequent decisions. Imagine how your trading must be affected after you read a headline saying “North Korea Authorizes Nuclear Attack on the US.”

Happy Is The Land

As concrete examples of his work, Dr. Peterson shared some recent strategic insights. Analysis of national sentiment indicates that extreme sentiments are typically followed by contrarian reversals. Thus, MarketPsych ranked the top 40 nations on a “country joy index” and built an investment approach around shorting the four most joyful nations, while going long the four least joyful, resulting in a “pairs arbitrage” position. The reasons markets top out is because everyone has become optimistic. When the last buyer has gleefully bought into a rising market, there is no one left to take that market higher. Similarly, when everyone is bearish, that’s when markets make bottoms. At a national level, the next move for a joyful populace should logically be towards dissatisfaction, and for people who are thoroughly unhappy, there’s nowhere to go but up.

Simplistic as it sounds, the work that goes into building these models is robust, and the outputs continue to be rigorously tested and refined.

Government instability frightens investors away – leaving buying opportunities for contrarians. MarketPsych’s country ideas include one-year long positions on Russia and Pakistan (high government instability, looming disasters, low joy). Meanwhile, currency ideas include a one-year long position on the Australian dollar, in the face of rising commodity pessimism and fears it will wreck their economy.

Fed Up?

At the national government level, going short trust / long mistrust turns out to be a fruitful strategy. Shorting a well-respected central bank, while going long a despised one could pay off. (We leave it to you and your financial adviser to figure out the implications for Mr. Bernanke’s Federal Reserve.) Significantly, Dr. Peterson’s work indicates low budget deficits are a negative for investing in a country (too much stability).

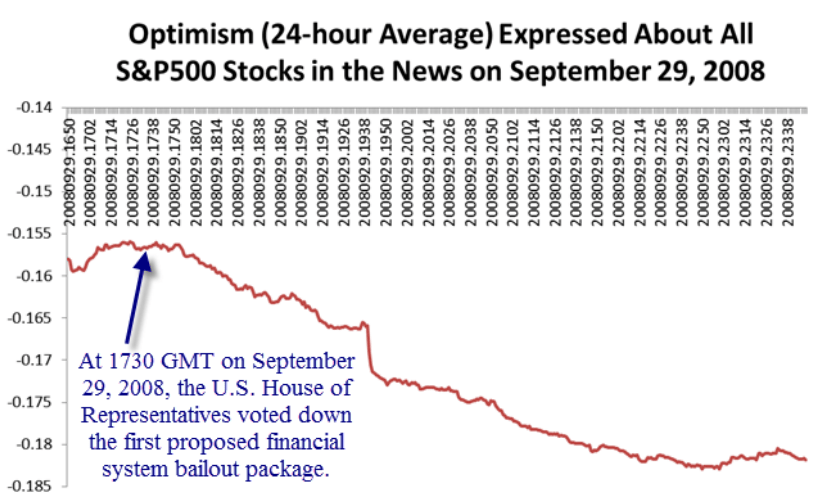

Perhaps the most graphic depiction of this is a chart indicating that Optimism is one of the greatest enemies of market stability. MarketPsych provides a graph of the precipitous decline in the S&P 500 index triggered when, in September 2008, Congress rejected the first proposed rescue package, saying the financial sector was strong and did not need bailing out.

On the equities side, Dr. Peterson singled out Carnival Cruise Lines (CCL) – a stock Hedgeye has been negative on. Dr. Peterson’s work indicates CCL could be an attractive long position: lots of anger, lots of disaster – both actual and anticipated – a company that has fallen from grace and is now almost universally demonized.

Conclusion: The #1 Mistake Investors Make

Dr. Peterson says the single most controversial aspect of his work continues to be the mere notion that our investment decisions are driven by emotion. For starters, this means you should drop out of that MBA program and get master’s degree in psychology. It also means you are better guided by seeing your shrink, rather than your stockbroker.

One of the key points in Dr. Peterson’s book, in fact, is that investors are willing to pay a premium for professional advice, even when it is consistently average – or even wrong. Facing powerful emotions all day long takes its toll – ask any seasoned trader. (Ask any seasoned psychiatrist!) Writes Dr. Peterson (p. 83) “Investors feel less emotional when deferring some responsibility for financial outcomes onto another.” This raises the same troubling issue that Hedgeye has been battling since we came into existence: the financial industry is highly conflicted. Its primary interest is in creating ways to pay itself, rather than coming up with ways to make you money. Not everyone can be the Smart Money. But in a field so shrouded in mystery, it doesn’t take much skill to serve as an emotional crutch.

Dr. Peterson says that by far the biggest mistake investors make over and over again is that they hold onto losers far too long, suffering greater and greater losses.

We would add the Hedgeye Corollary: Most investors hold onto mediocre advice far too long. Because let’s face it, it’s hard to be wrong about your investments so often. Much better to have a professional who you pay to be wrong for you.

For more information about Dr. Peterson’s work, please email info@marketpsychdata.com.