The Supplemental Nutrition Assistance Program (SNAP, aka Food Stamps), saw one of the largest month-over-month declines in participation during January. While it may be due to policy changes in North Carolina, in general, it appears that people are beginning to jettison the program from their lives. This comes after the SNAP participation rate hit a 30-year high in late 2012, as people without jobs and those who had given up on looking for a job jumped on the bandwagon.

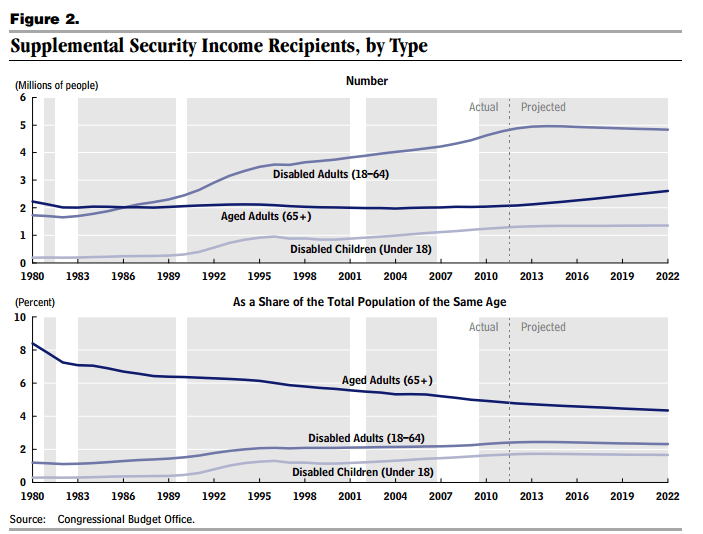

As more people drop out of the labor force in America and latch on to SNAP and Supplemental Security Income (SSI), the American economy will suffer a decrease in tax revenue as well as other additional problems.