Key Takeaways:

Overall, risk remains in check in spite of Europe's deposit scare. We remain vigilant based primarily on where we are in the calendar, but as yet the key metrics we watch are not showing signs of degradation. For now, we're sticking with our bullish bias on the Financials sector.

* XLF Macro Quantitative Setup – In the short-term, our Macro team’s quantitative setup in the XLF shows better upside than downside with +1.7% upside to TRADE resistance and -0.6% downside to TRADE support.

* Markit MCDX Index Monitor – Last week the 16-V1 series saw spreads tighten 4.6 bps, ending the week at 79.5 bps versus 84.13 bps the prior week. In spite of Stockton, CA, systemic risk perception around the muni market's default risk continues to drop.

* ECB Liquidity Recourse to the Deposit Facility – In spite of Cyprus, the ECB's overnight deposits have remained stable in the past month, and declined by 9.5bn Euros last week.

* Euribor-OIS Spread – The Euribor-OIS spread was unchanged week-over-week at 13 bps.

* European Financial CDS - Most European banks were tighter last week with an average tightening of 10 bps anda median tightening of 5 bps. This was the first week of improved performance since the Cyprus news broke.

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 4 of 12 improved / 2 out of 12 worsened / 7 of 12 unchanged

• Intermediate-term(WoW): Negative / 1 of 12 improved / 7 out of 12 worsened / 5 of 12 unchanged

• Long-term(WoW): Positive / 7 of 12 improved / 2 out of 12 worsened / 4 of 12 unchanged

1. U.S. Financial CDS - Citi and Morgan showed the worst performance week-over-week, rising by 7 and 5 bps, respectively. On a month-over-month basis, however, Morgan is tied with BofA for worst at +20 bps apiece. Overall, swaps widened for 19 out of 27 domestic financial institutions.

Tightened the most WoW: AXP, GNW, XL

Widened the most WoW: MMC, AGO, C

Tightened the most WoW: XL, ALL, GNW

Widened the most MoM: MTG, JPM, BAC

2. European Financial CDS - Most European banks were tighter last week with an average tightening of 10 bps anda median tightening of 5 bps. This was the first week of improved performance since the Cyprus news broke.

3. Asian Financial CDS - While Japanese bank stocks have soared on the back of QE-Quadrill-Yen, default risk measures have ticked up modestly for most Japanese banks.

4. Sovereign CDS – Sovereign swaps were tighter across the planet last week, except for Japan where they were flat. The biggest improvements were in Italy and Spain, where swaps dropped 19 bps apiece.

5. High Yield (YTM) Monitor – High Yield rates fell 3.0 bps last week, ending the week at 5.78% versus 5.81% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 1.3 points last week, ending at 1788.1.

7. TED Spread Monitor – The TED spread rose 0.8 basis points last week, ending the week at 21.64 bps this week versus last week’s print of 20.86 bps.

8. Journal of Commerce Commodity Price Index – The JOC index fell -1.6 points, ending the week at 8.25 versus 9.9 the prior week.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged week-over-week at 13 bps.

10. ECB Liquidity Recourse to the Deposit Facility – In spite of Cyprus, the ECB's overnight deposits have remained stable, and declined by 9.5bn Euros last week. The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

11. Markit MCDX Index Monitor – Last week the 16-V1 series saw spreads tighten 4.6 bps, ending the week at 79.5 bps versus 84.13 bps the prior week. In spite of Stockton, CA, systemic risk perception around the muni market's default risk continues to drop. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states.

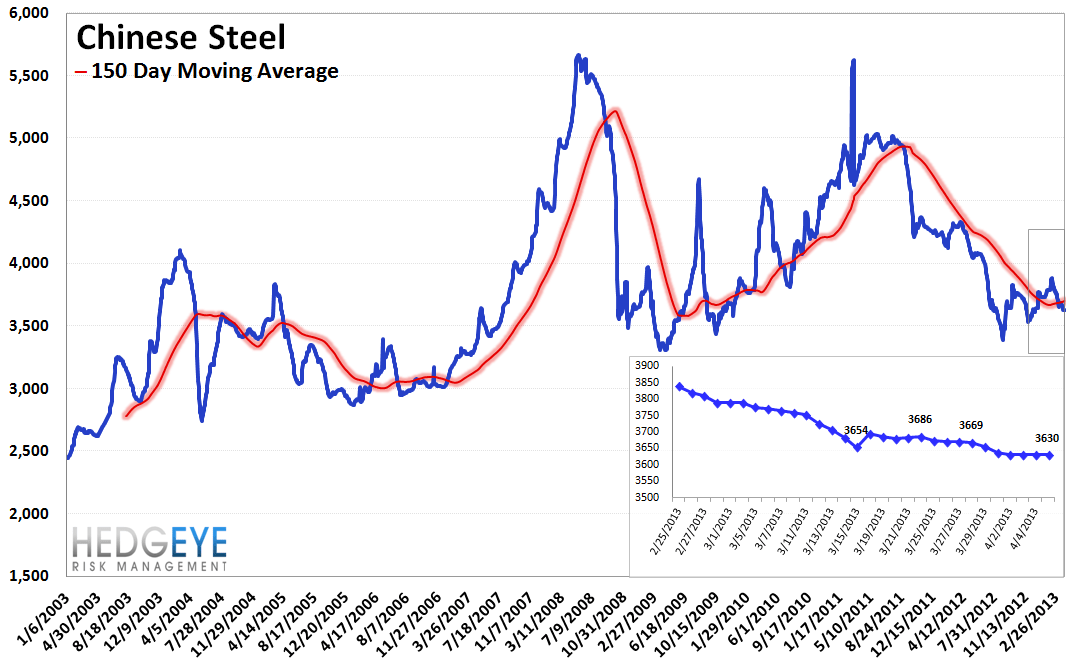

12. Chinese Steel – Steel prices in China fell 0.7% last week, or 25 yuan/ton, to 3,630 yuan/ton. Taking a step back, Chinese steel prices have been declining since mid-February of this year. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 162 bps, -4 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 1.7% upside to TRADE resistance and 0.6% downside to TRADE support.

Joshua Steiner, CFA