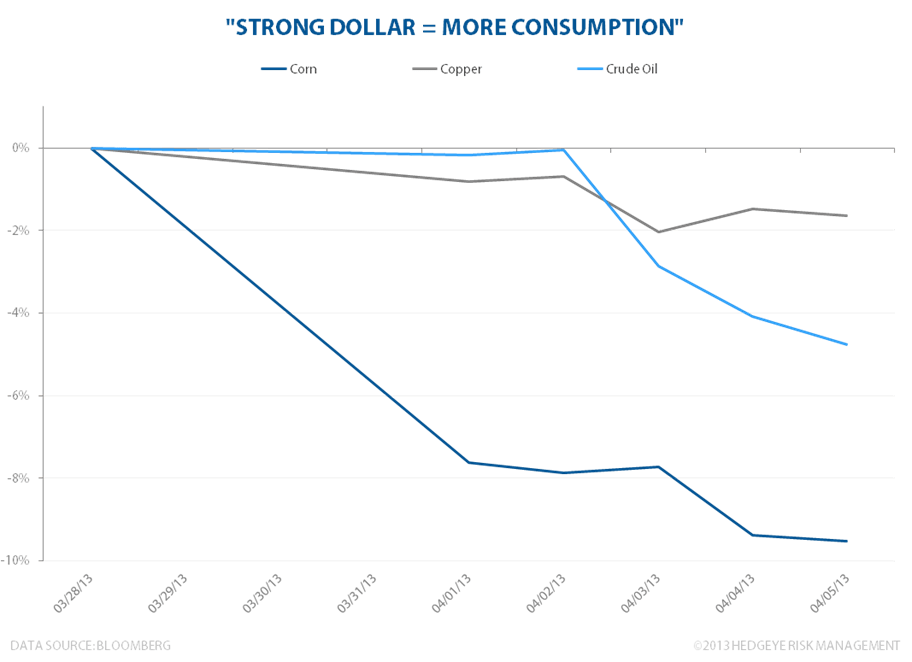

Over the last 8 weeks, the US dollar has appreciated in value at an impressive clip. In turn, commodity prices have fallen considerably in tandem with the dollar's appreciation. Most notably, corn, copper and crude oil prices have dropped in price significantly, which is a boon for the American consumer. Lower gas prices and lower food prices are what help drive consumption and in the end, more consumption = more growth, which helps with corporate earnings.