This note was originally published at 8am on March 22, 2013 for Hedgeye subscribers.

“Reality is merely an illusion, albeit a very persistent one.”

-Albert Einstein

This has been an entertaining week at Hedgeye. For those that have been reading the Early Look or following us on Twitter, you have noticed that we have been having some fun with a few of the old guard of Wall Street research. One friend of Hedgeye actually wrote in and called Keith and myself: grumpy young men.

Candidly, that is probably more truth than illusion. To be fair, though, getting up early and grinding hard throughout the week probably does rightfully make a guy or gal grumpy. There is no doubt many of our subscribers can relate to this as well. While we have the pressure of running a profitable business and making 50+ employees happy, the pressure that many of you have associated with the fiduciary responsibility of managing money is also no illusion.

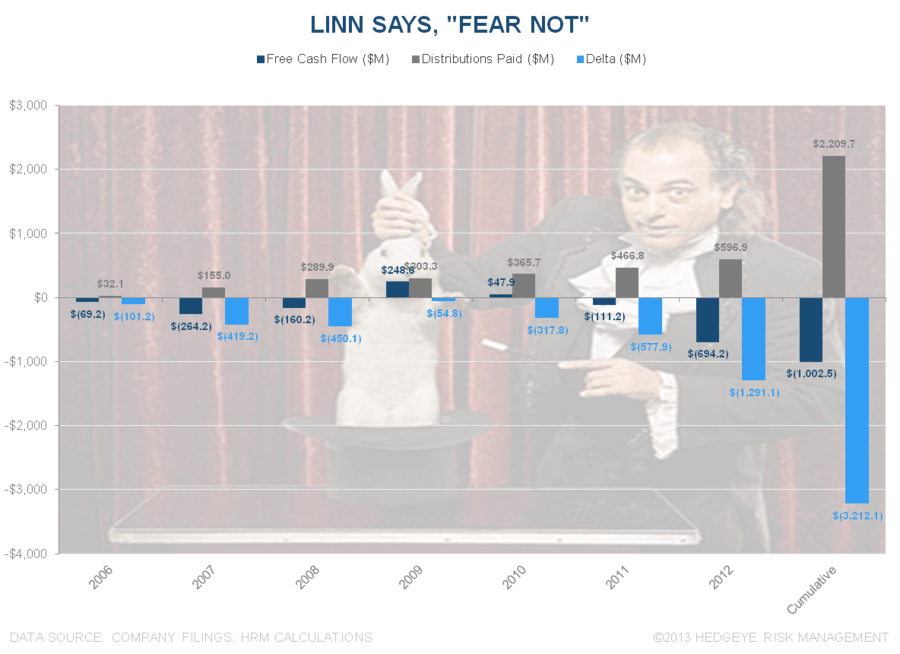

Speaking of illusions, our Energy Analyst Kevin Kaiser actually identified a great one this week in the cash flow statement of a company called Linn Energy (LINE). LINE is an upstream MLP, so in effect they use the tax advantage of a MLP structure to pay out large distributions. This is fine for predictable and mature businesses. Unfortunately, neither of those traits fit LINE.

In fact, LINE is an oil and natural gas producer. So not only is it not a mature to slightly growing business, it is actually a business with natural decline rates that requires meaningful capital expenditures to maintain the cash flow stream. In the Chart of the Day, we’ve included a slide from the presentation that looks at distributions paid from 2006 to 2012.

In that time period, LINE paid $2.2 billion in distributions. Strangely, in the same period the company only generated $1.7 billion in cash flow from operations. Moreover, if we look at free cash flow, which we define as cash flow from operations less capital expenditures, LINE generated a negative -$1.0 billion in cash flow. Despite these cash flow deltas, LINE management has done a decent job pulling rabbits out of the proverbial cash flow hat and paying distributions, largely from financing cash flow.

So, as Kaiser summed up about the company at the end of his presentation:

The illusions:

- LINN’s assets are mature oil and gas fields with low decline rates;

- LINN’s cash flows are stable because of its hedging strategy;

- LINN generates sufficient cash flow to pay and grow its distribution;

- With an 8% yield, LINN is an attractive fixed-income alternative; and

- LINN is creative and innovative.

The reality:

- LINN’s base decline is 20 - 25% per year;

- LINN’s cash flows are overstated because of its hedging strategy;

- LINN does not generate any FCF, and must raise additional capital to pay its distribution;

- LINN equity is more than 50% overvalued today; and

- LINN is financially creative and innovative.

If Houdini were a hedge fund manager, he would likely be all over this company!

In the global macro world this week, the primary illusion has been in regards to the cash in Cypriot bank accounts. Is it there? Will it stay? How much will the government take? Coming in to the week, many pundits predicted that the arbitrary decision to “tax” money in bank accounts in Cyprus would lead to a run on the banks across the peripheral countries in Europe. Much to the chagrin of alarmists, this hasn’t happened.

Of course, this is not to say that the EU decision to try and force a bank levy on Cyprus makes any sense. The larger risk is not that the EU will do try to this in Greece, Portugal, or Spain next, but rather that the illusion is created that they will. A run on banks across the peripheries is literally a worst case scenario for the EU. Unfortunately, investor and depositor confidence erodes very quickly with seemingly arbitrary decisions.

The latest news flow suggests that the Cyprus situation will continue into next week. Russians have a large amount of capital in the Cypriot banking system, but Cypriot Finance Minister Michael Sarris spent all week in Russia and returned with his hat in hand and no bailout monies. The European Central bank has also said that effective this coming Monday they will cut off liquidity lines unless Cyprus gets a deal in place. So yes, the illusion that ECB officials have the situation under control is alive and well.

As for the Cypriots, well as of this morning the statement the government was supposed to issue is now more than 60 minutes late, but according to Twitter they are working on it. As for the average Cypriot, their bank withdrawals from ATMs are limited to literally a couple hundred Euros. Talk about dysfunction!

The slow and steady recovery of U.S. economic activity continues to be solidly in the category of non-illusions. The key data point we received this week was in the way of non-seasonally adjusted jobless claims, which declined by -7.5% year-over-year for the week. In aggregate, the improvement in jobless claims is starting to mirror 2012.

Our Financials Sector Head Josh Steiner has noted many times, improving jobless claims are one of the best leading indicators for housing trends, credit quality, and loan growth. Even as the dysfunction in Europe percolates, the U.S. economy stabilizing is no illusion. This is a key reason U.S. equities remain one of our favorite global asset classes.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1594-1620, $107.01-108.99, $3.39-3.49, $82.23-83.39, 94.12-97.08, 1.89-1.98%; 10.73-14.74, and 1542-1565, respectively.

Enjoy your weekends.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research