Starwood amended its credit facility to raise the maximum leverage covenant from 4.5x to 5.5x. In return HOT agreed to the following:

- The applicable margin (AM) on the revolver increased from a range of 37-80bps (at 4Q08 they were borrowing at an AM of 50bps) to 175-300bps above LIBOR

- The term loan AM increased to 200-350 bps from 45-100 bps

- Limits on HOT's ability to pay dividends and repurchase stock subject to the Company's FCF and Leverage ratio

- Decreased Permitted Lien basket to 5% of Tangible Net Assets from 10%

- An amendment fee of 50bps or $13.75MM

The positives to HOT are clear. Based on our projections, we had Starwood exceeding its 4.5x maximum leverage covenant in Q3 2009 and maxing out at 5.2x in 2010. This amendment should provide them enough cushion under the new 5.5x maximum leverage covenant. To the extent HOT can sell some assets or complete a securitization deal, this will provide them with incremental liquidity.

On the negative side, the amendment will cost the company about $35MM in pre-tax income or $0.12 in EPS. Moreover, HOT management should be able to give more reasonable (lower) guidance. Their 2009 guidance (from the last earnings release) was way too high and did not indicate a covenant breach. An amendment would not have been necessary if their initial 2009 EBITDA projections were achievable.

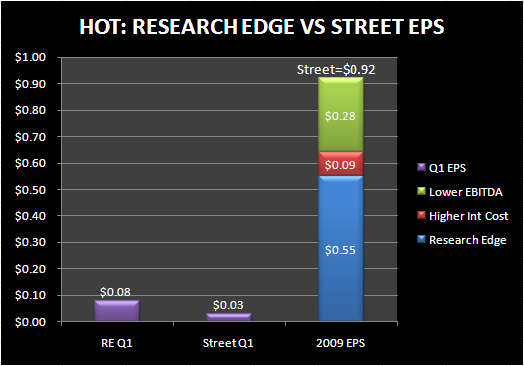

Look for another "beat and lower" quarter out of HOT. We are at $0.08 and $170MM in EPS and Adjusted EBITDA, respectively, for Q1 versus the Street at $0.03 and $155MM. However, our 2009 projections of $0.55 and $775MM, respectively, fall well below the Street at $0.92 and $850MM. 2010 should look even uglier.