TODAY’S S&P 500 SET-UP – April 5, 2013

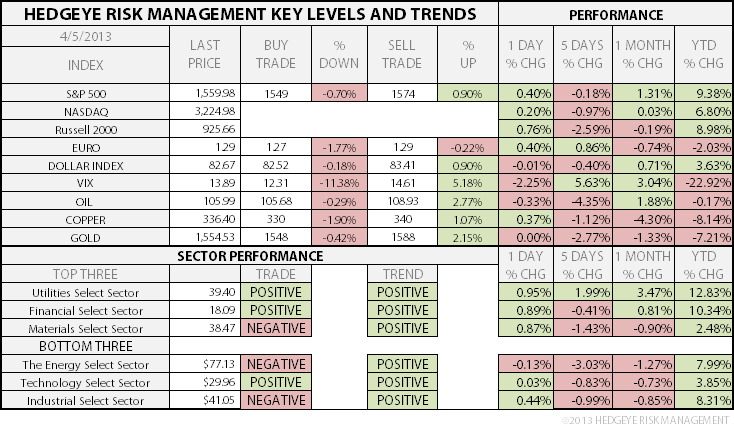

As we look at today's setup for the S&P 500, the range is 25 points or 0.70% downside to 1549 and 0.90% upside to 1574.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.53 from 1.54

- VIX closed at 13.89 1 day percent change of -2.25%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Trade Balance, Feb., est. -$44.6b (prior -$44.4b)

- 8:30am: Nonfarm Payrolls Change, March, est. 190k (pr 236k)

- 8:30am: Unemployment Rate, March, est. 7.7% (prior 7.7%)

- 1:30pm: Baker Hughes rig count

- 2:30pm: Philadelphia Fed vice president Nason speaks

- 3pm: Consumer Credit, Feb., est. $15b (prior $16.15b)

GOVERNMENT:

- CFTC holds closed meeting on surveillance and enforcement matters, 10am

- Talks resume on Iran’s nuclear weapons program in Kazakhstan

WHAT TO WATCH

- Payrolls in U.S. probably rose in March as demand picked up

- Blackstone said to sidestep Michael Dell’s role in buyout talks

- Soros joins Gross in warning Kuroda plan risks rout in yen

- BP to ask judge to halt some oil spill settlement payments

- Olam to discontinue legal action against Muddy Waters, Block

- Euro-area Feb. retail sales fell less than est. from Jan.

- German Feb. factory orders may rise from Jan.: survey

- Grohe owners said to mull IPO, sale of bathroom fixtures maker

- Banks warn stricter securitization rules risk credit drought

- North Korea regime uncertain, maintains stability: South Korea

- Japan considers shooting down North Korea missile: Sankei

- U.S. budget, Bernanke, China, Masters: Wk Ahead April 6-13

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Set for Biggest Weekly Drop Since September Amid Iran Talks

- Gold Traders Split With Bullion Nearing Bear Market: Commodities

- Soybeans Fall for Third Day as Bird Flu in China May Hurt Demand

- Platinum to Slump as Europe Car Sales Tumble: Chart of the Day

- Copper Swings on Chile Export Curbs and Signs Economies Struggle

- Cocoa Falls a 3rd Day as Rain May Help Crop; Sugar Also Declines

- SGX to Introduce Iron Ore Futures as Investors Bet on China

- Russian Grain Crop Seen by Rusagrotrans Up 28% in Coming Season

- Le Fracking for Geothermal Heat Draws Ire of French Oil: Energy

- Coal Strike Looms as Workers Protest Stake Sale: Corporate India

- Meat Industry Renames Beef, Pork Cuts Before U.S. Grill Season

- RIN Ethanol Price Risk Remains Skewed to Upside, Goldman Says

- Aluminum Premiums Reach Record as Warehouse Releases Limited

- Gold Trades Near 10-Month Low in London on Recovery Outlook

CURRENCIES

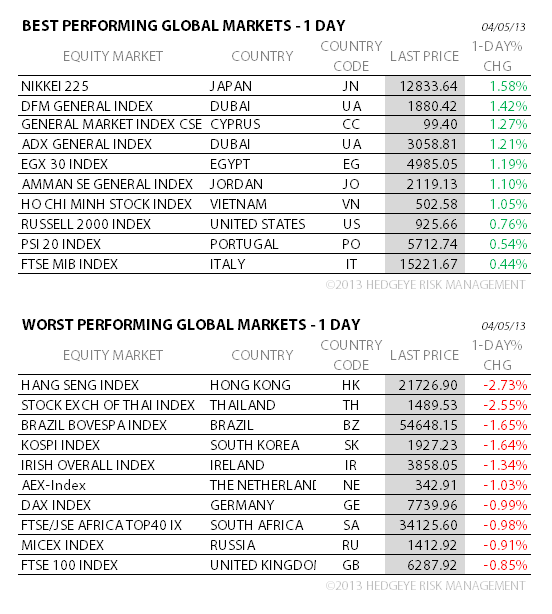

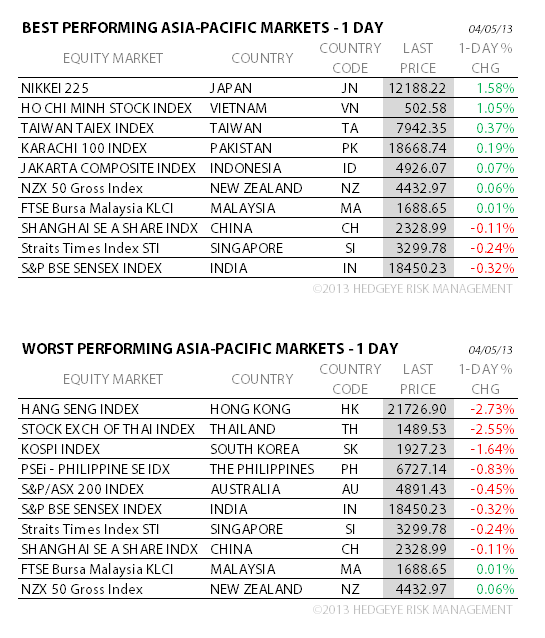

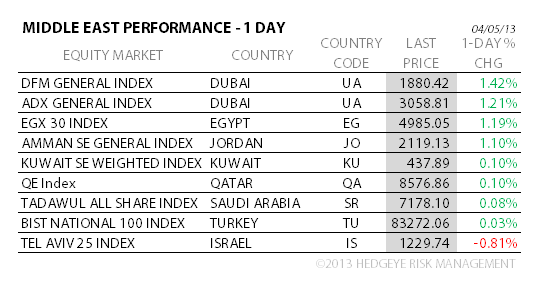

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team