One consistent theme in the market in 2013 has been lower volatility – except for random, brief events the trend in the VIX (CBOE Volatility Index) has been lower to start the year. As an exercise, we have been following a couple of ETF’s that seek to track lower volatility:

- SPLV – PowerShares Low Volatility Portfolio

- USMV – iShares USA Minimum Volatility Index Fund

As one would expect, both ETFs have performed extremely well in 2013 (I know, blinding glimpse of the obvious). Both have also seen significant inflows – SPLV $903 million YTD (versus $2,067 million in all of 2012) and USMV $1,728 million YTD (versus $735 million in all of 2012).

The top holdings of each are interesting as well for the purposes of our analysis.

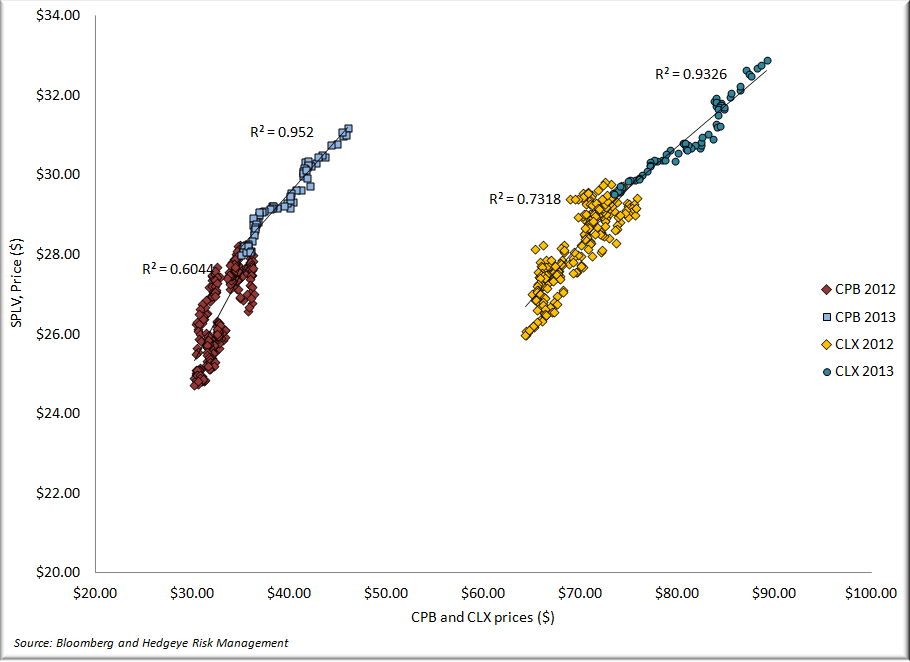

SPLV

- · PEP (#2)

- · CLX(#3)

- · GIS (#4)

- · CPB (#7)

- · KMB (#12)

USMV

- · GIS (#3)

- · PEP (#11)

- · KMB(#12)

Since the start of the year, the performance of a number of consumer staples names has been highly correlated to the performance of these low volatility ETFs and, by extension, the VIX. No doubt, the associated money flows into these ETF's have been partly responsible for the significant outperformance of names such as CLX, GIS, CPB and KMB.

We offer this analysis as another data point to suggest that something other than business fundamentals are driving the share prices of these companies and that someone (or something) other than fundamental investors are buying them. It's hard to fight these kind of moves, but it will end, and when it does dedicated staples investors will be left with names that have far outstripped any reasonable valuation metric.

Unfortunately, we don't know when this will end, but perversely, these ETFs are now likely faultily constructed, as these names at these levels don't represent (to us at least) "low volatility". At some point, the long-term betas used in the construction of these ETFs will catch up to the reality of the recent move.

Call with questions,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst