Today’s ECB press conference was largely non-eventful. Rates were left unchanged, Draghi reiterated that the economic outlook remains weak, inflation expectations are anchored, and credit conditions remain tight. Below we show a chart of the weakening credit lines to households and corporations, which should continue to hamper real growth.

Click here to read Draghi’s prepared remarks.

There were many questions on Cyprus in the Q&A. Draghi was quick to state that the Cyprus levy is no template for the Eurozone (and acknowledged that Eurogroup head Jeroen Dijsselbloem misspoke on the topic), and that the original ECB proposals for a Cyprus bailout/in did not include a levy.

As we discussed yesterday in a post titled “ECB on Hold; EUR Pressured; Slovenia Scares” we think that the uncertainty around the next Italian government, the tail of Cyprus, recent scares over Slovenia as the next country in need of a bailout, and the ECB keeping the interest rate on hold will put downside pressure on the EUR/USD.

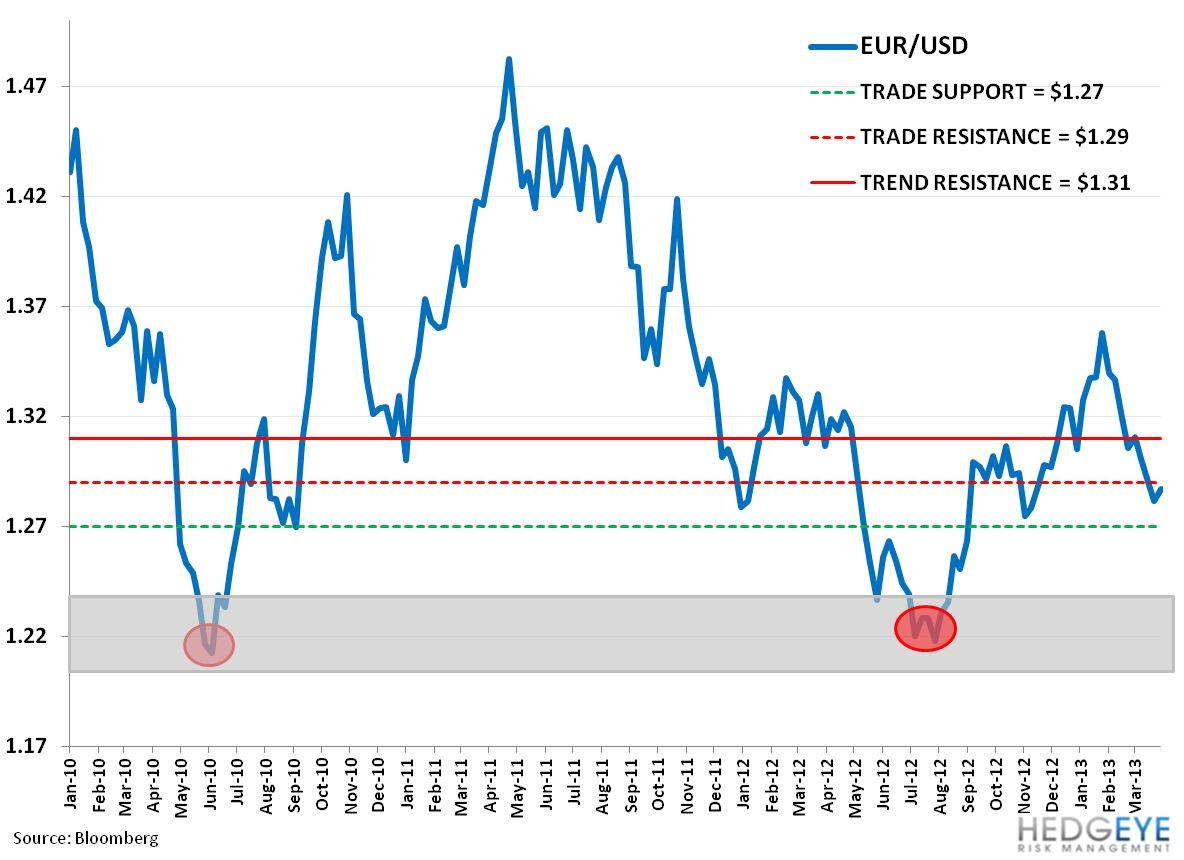

Our critical quantitative lines on the EUR/USD are outline in the chart below. Beyond immediate term TRADE support of $1.27 we do not see any meaningful support until around $1.22.

Matthew Hedrick

Senior Analyst