This morning's awful seasonally adjusted initial jobless claims print appears to have been negatively impacted by the Easter week holiday. Taken together with the weak ADP report and the weak Challenger report, the market is clearly developing a bearish bias in the short term around labor conditions. We'll see what tomorrow's river card brings.

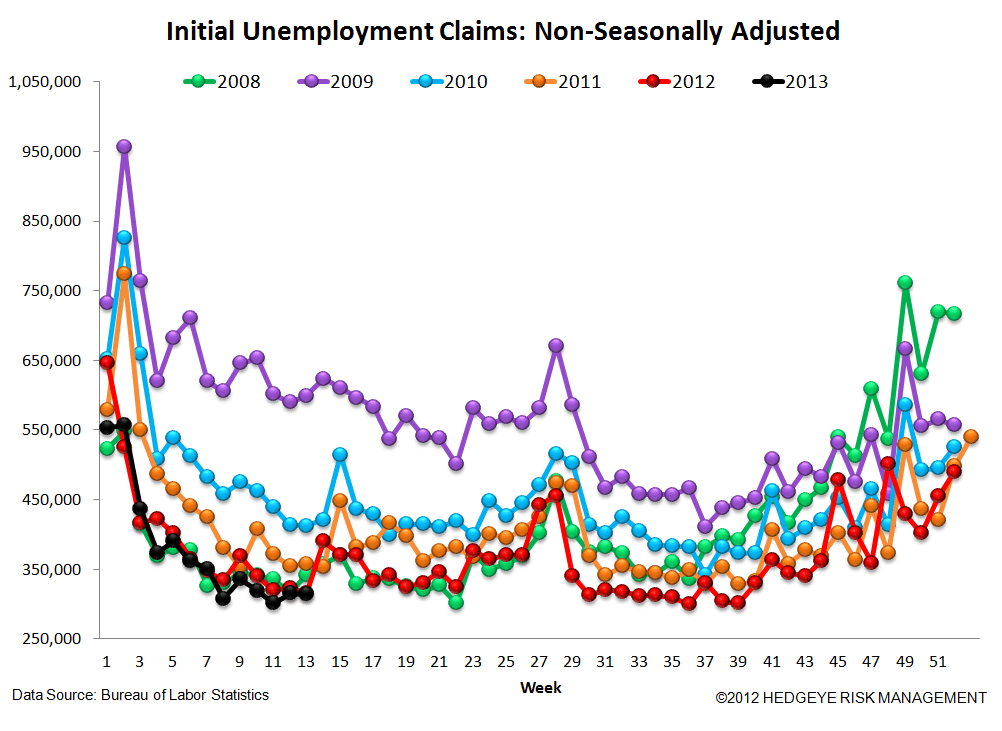

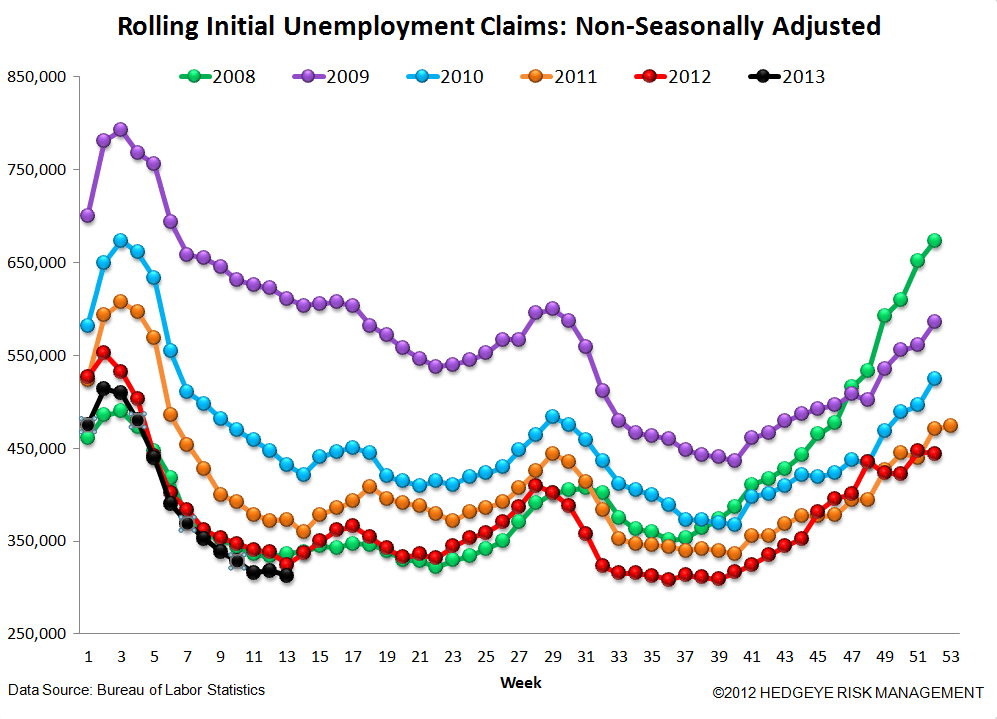

The non-seasonally adjusted claims number was essentially flat week-over-week. Looking at the trend in the non-seasonally adjusted data, it's still trending better year-over-year, but only just barely. This week's print was better by just 0.5% vs. the same week last year. The trend in this dynamic over the last five weeks has been: -0.5%, -2.4%, -5.8%, -6.1%, -8.9%. Clearly the rate of year-over-year improvement has been slowing notably over the past month. A silver lining is that the trend in rolling NSA claims YoY is less negative, as we show in the second chart of this note.

The bottom line is this: labor conditions aren't as bad as they appear (in the SA numbers), but are, in fact, showing signs of genuine cooling.

The Data

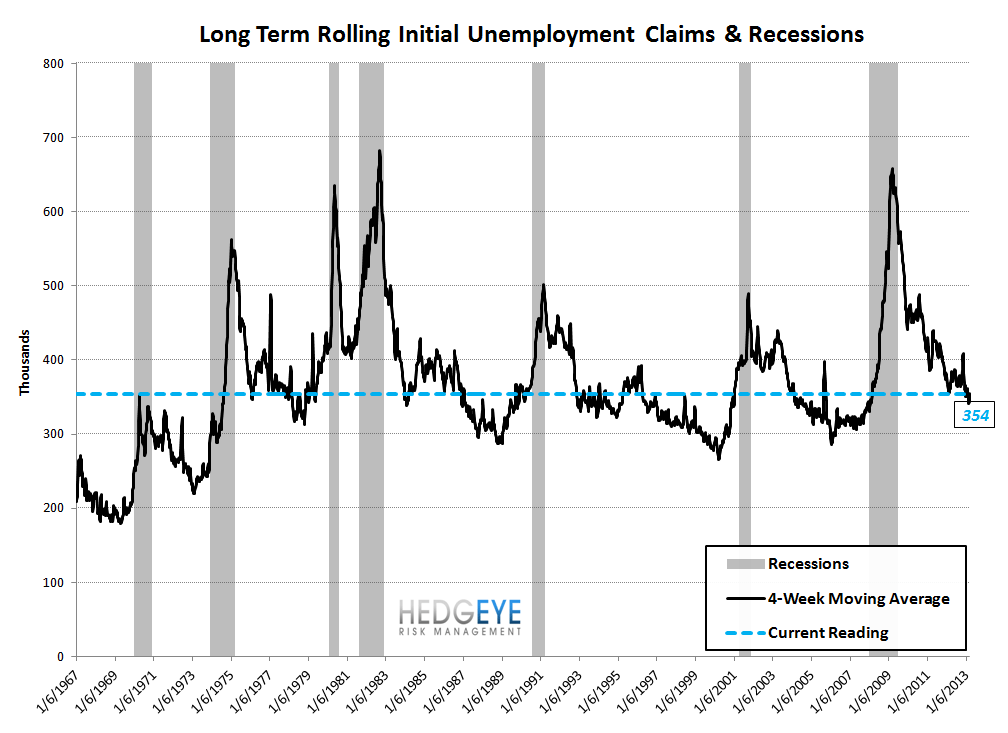

Initial jobless claims rose 28k to 385k from 357k WoW. The previous week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 10.75k WoW to 354.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -3.8% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -5.9%

Yield Spreads

The 2-10 spread fell -6.9 basis points WoW to 160 bps. In 1Q13, the 2-10 spread is averaging 167 bps, which is higher by 25 bps relative to 4Q12.

Joshua Steiner, CFA