Takeaway: We expect no change on Thursday from the ECB in interest rates as the data is “accommodative”. EUR/USD continued downside support alongside Italian election uncertainty, Cyprus, and new Slovenian scares.

Real-time Positions in Europe: Short SPDR Euro Stoxx50 (FEZ)

ECB on Hold

On Thursday the ECB’s governing council convenes. We expect no change to the main interest rates. Our rate position is largely in agreement with consensus -- 46 of 48 economists polled by Bloomberg expect no change. We don’t rule out a rate cut in 2013, but aren’t calling for one tomorrow.

This position is grounded in recent data that is supportive of an “accommodative” hands off approach from Draghi – CPI came down over recent months and is resting at 1.7% Y/Y in MAR, below the ECB’s 2.0% targeted level. PMIs across the region continue to look dim, but across the core were revised up in MAR versus initial estimates. While the Eurozone unemployment rate has ticked up to all-time highs of 12%, Draghi will offload this concern to the labor market reforms needed at the country level. Also, the aggregate unemployment rate has historically been higher than in the U.S. and is tame compared to peripheral figures.

While we think that investor sentiment is lower on the region currently due to concerns over Italy, Cyprus, and now possibly Slovenia (more below) – as compared to the optimism in the back half of 2012 following the announcement of Draghi’s OMT –– we expect Draghi to keep his policy powder stowed on Thursday until there is a more meaningful flair-up in risk or greater change to the underlying data that the bank tracks. We believe the bank is also waiting and watching to see the outcome of the political scene in Italy.

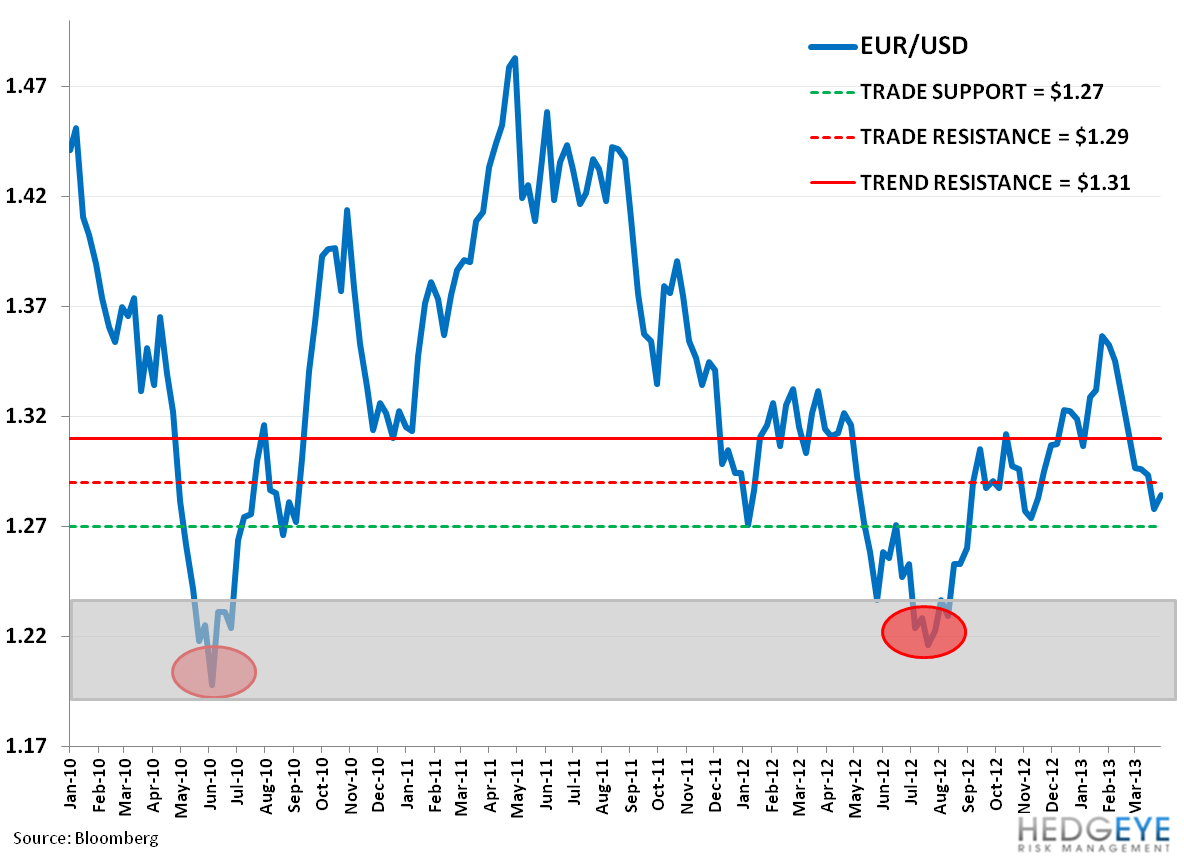

EUR/USD Levels

Broadly we think the uncertainty around the next Italian government, the tail of Cyprus, recent scares over Slovenia (more below), and the ECB interest rate stance on hold will put downside pressure on the EUR/USD. We’re no closer since the Italian election of late February in determining if a coalition can be formed as both Pier Luigi Bersani’s center-left and Beppe Grillo’s Five Star Movement refuse to accept a coalition.

Our critical quantitative lines on the EUR/USD are outline in the chart below. We do not see any meaningful support until around $1.22.

The most recent weekly CFTC data (from 3/26) shows a continued net bearish positioning in the EUR/USD.

Slovenia Joins the Mixer

Interestingly, the financial risks associated with Slovenia have received more attention this week. Take a look at the charts of the 8YR Yield on Slovenian debt, which began its hockey stick move on 3/15 to top out near 7% on 3/27, and 5yr CDS that jumped up since 3/22, but still remains below associated Greek freak-out levels last summer.

If we have a Slovenian moment it will be very similar to Cyprus – a blip on the radar in terms of shaking the Eurozone apart – and we would not expect a similar deposit levy to be issued. Slovenia is much too close to the heart of Europe, it has different banking issues than Cyprus, and we believe the levy in Cyprus was largely a misstep on the part of the Eurocrats anyways.

To provide a bit of context on Slovenia, the country has been in the cross hairs (so to say) regarding its fiscal state for over a year, with the government at times saying either that it doesn’t need a bailout, or if it did, would not ask for external help. But who can you trust these days? Certainly not the Slovenian government.

The government actually fell in FEB 2013 over then PM Janex Jansa receiving slush funds, and on 3/14 was replaced by a coalition government led by the center left.

It’s a rather small country (population of 2MM), with little great industry to speak of versus say its near neighbors the Austrians, Hungarians, or Slovaks. Its banks, much like most countries in the region, are stuck with a bunch of bad loans (many construction related), with estimates to the tune of €7 Billion.

Here are a few economic facts:

- GDP ~ €35 Bill (or 0.3% of Eurozone) vs Cyprus of €20B

- GDP was down -2.3% in 2012

- Debt as a % of GDP = 53.2% (as of 2012)

- Deficit as % of GDP = -6.4% (as of 2011) vs -5.7 in 2010

- CPI = 2% Y/Y

- Industrial Production -1.8% (trending lower for last 15M)

- Unemployment Rate at 13.6% JAN

We’ll continue to monitor and dig in on Slovenia as the market turns. In any case, our bottom line is that should there be a need for a bailout, the Eurocrats will again jump at the opportunity to throw good money at bad and sweep Slovenia, like Cyprus, under the rug.