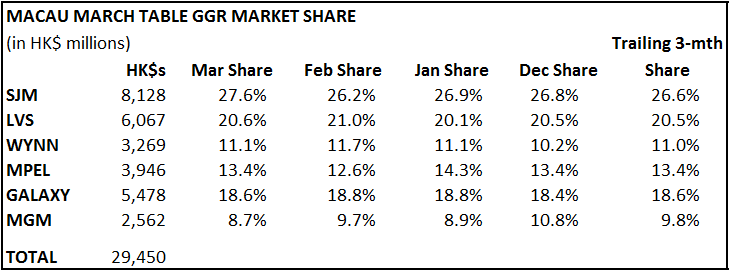

Please find the monthly table market shares and average daily table metrics below. Total March GGR (including slots) increased 25.4% YoY to HK$30.4 billion, in-line with recently raised expectations but well above projections given prior to the first week of March. We don’t yet have the full property detail so it remains to be seen how much hold contributed to the outstanding and record month. Anecdotally, we’ve heard that VIP hold was high but that volumes were also very strong. We believe volume growth played the majority role in the YoY growth.

With the exception of SJM and MGM, the concessionaires posted shares almost exactly in-line with trend. SJM’s 110bp increase in share over recent trend was pulled almost directly from MGM.