Conclusion: The financial composition of athlete endorsement structure is more different in comparing Nike vs. UnderArmour than one might think. UnderArmour has wiggle room to be less conservative and take on more implied leverage with longer-dated sponsorship agreements as Nike’s long-dated deals outpace UA’s by over 200x. This could offer UA margin leverage on a TREND and TAIL duration, which it sorely needs. But NKE’s size, scale and balanced portfolio of deals is tough for anyone to compete with. This is not enough for us to get constructive on UA today, but it's something we'll watch develop.

FULL DETAILS

Much like off-balance-sheet leases, companies are also required to disclose any contractual obligations as it relates to endorsements and/or sponsorships. In the case of Nike and UnderArmour, this is Athlete Endorsements – and the numbers are quite significant. These are minimum payments that are required regardless of whether or not the athlete performs or even plays. We’re given good disclosure here, even though they are rarely analyzed or discussed by most of Wall Street.

Here are some notable differences in the financial composition of Nike’s athlete endorsement portfolio versus what we see at UnderArmour.

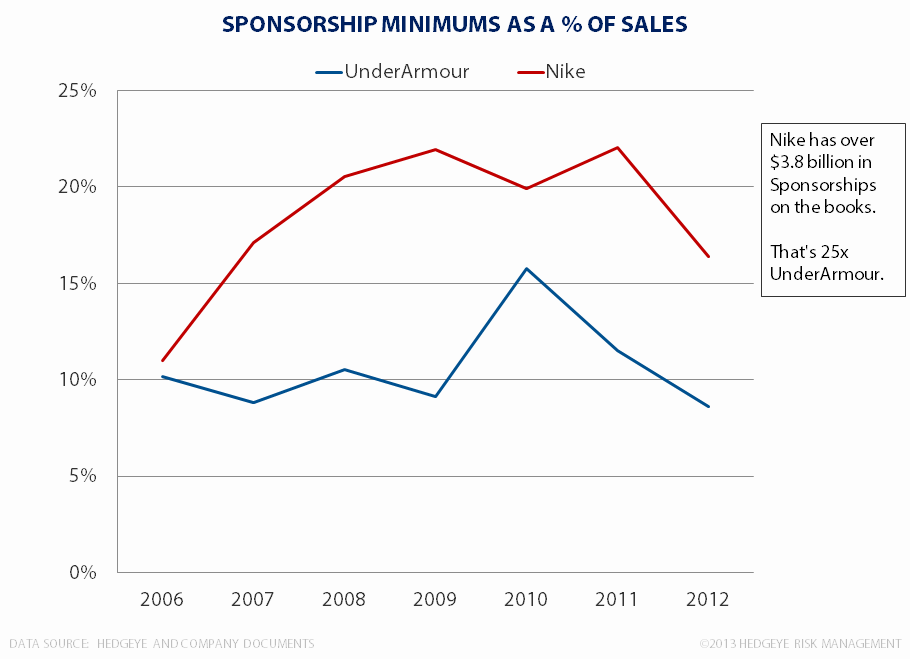

- Size Matters: The obvious difference between the two is the raw size, with Nike logging in $3.8bn in sponsorships on its books. UnderArmour is $158mm. While you could argue that this is to be expected given the size gap between the two companies, NKE’s obligations net out to be 16% of current year sales, while UA is only 9%. Nike is 13x the size of UA, but it’s athlete endorsement pool is 25x the size of UA.

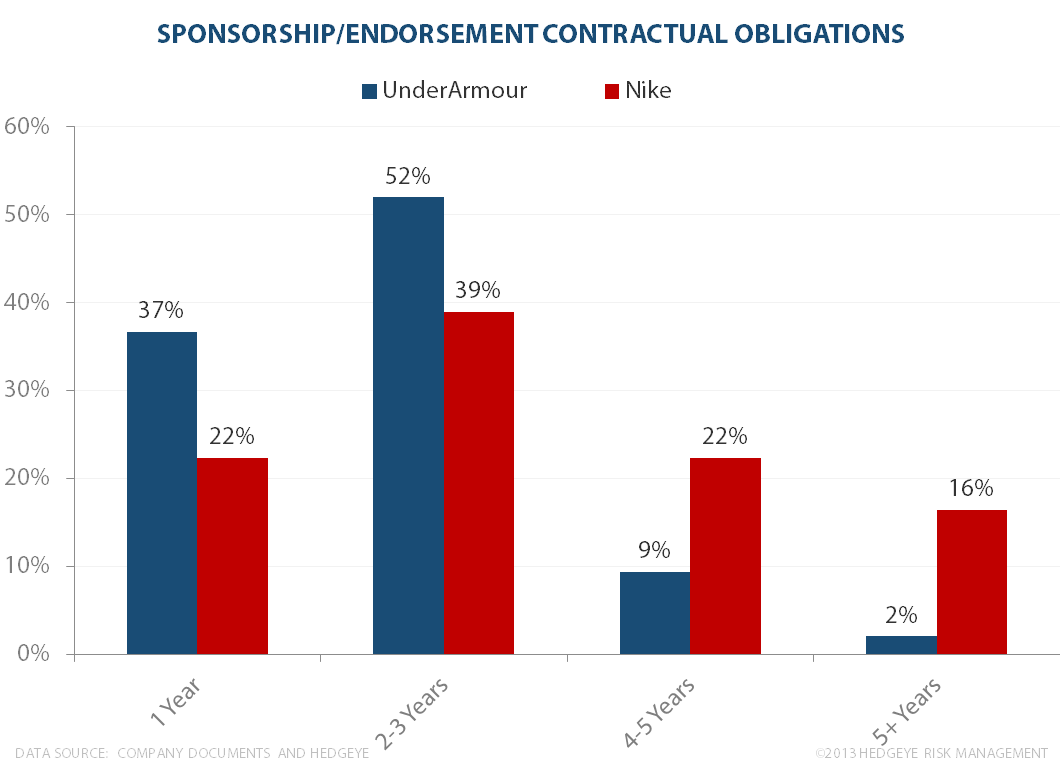

- Nike is More Balanced, But Opportunity for UA: It’s important to look at the duration of the obligated payments. As a percent of total, nearly 90% of UA’s payments are scheduled in less than 3-years. That compares to Nike at 61%. Conversely, 22% of Nike’s payments take place in years 4-5, and 16% are after year 5 (UA is 2%). We’re mixed on the implications here.

On one hand, Nike’s portfolio is balanced between short-term deals, longer-dated agreements that are soon coming to an end, and long-term agreements (ie the $628mm for NKE covers NFL, LeBron and the Tigers of the world). We like that.

On the flip side, NKE’s $628mm compares to UA’s long-term dollar tally of only $3mm. NKE’s long-term agreements are 209x UA’s. While this shows the opportunity for UA to sign more deals that are longer-dated (and presumably requiring lesser up-front investment), it shows how much powder Nike has even relative to a powerful competitor like UA. Deep pockets breed deeper pockets.

- Percent of Demand Creation/Marketing: Last year, 32% of Nike’s Demand Creation budget was ‘locked’ under these contractual agreements, and it’s noteworthy that in any given year over the past seven, the lowest Nike ever got was 27%. That’s incredibly stable. UnderArmour was remarkably close to NKE at 28% last year, but that number is up from 15% in 2006. Simply put, as UA matures, a greater proportion of its Marketing budget is being allocated to Athlete Endorsements as opposed to flat-out brand marketing. We’re ok with this, as it is a sign of a company maturing in this industry. But we’d rather not see it much higher (same goes for NKE).

- Note: The only way these minimum payments can cease to exist is if there is a breach of contract on the part of the athlete/team in question. That could be failure to participate in advertising/marketing campaigns, but that’s rare. More often, the factor comes down to an athlete breaking Morality clauses that are built into nearly all such agreements. When certain events are triggered, the Brand can look the other way (rare), sever the agreement (more frequent), or often in the case of Nike (Tiger, for example), the minimum obligation is materially lowered and the performance-based piece goes up materially.