THE HEDGEYE EDGE

We have been writing for several quarters of our belief that Darden’s multi-brand portfolio is inefficient and, far from achieving the economies of scale that management touts, has led to subpar cash return on investment.

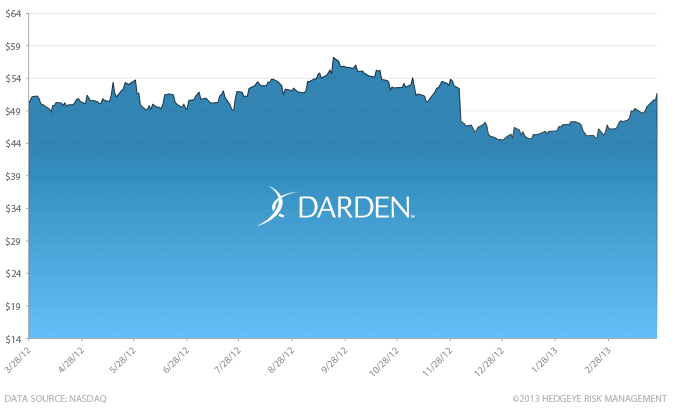

Following our call to short the stock in July of 2012, we saw a depreciation in the stock price and a general consensus emerge among the investment community that fully bakes in our negative views of the company’s fundamentals.

At this point, we believe that the potential for improvement at Darden is too great, and the mismanagement so egregious, that it is difficult to imagine either activism in the shareholder base or management offering a mea culpa and following a more prudent strategy with respect to capital allocation. In either scenario, the stock should appreciate and $1 billion in EBITDA makes the dividend yield safe and, we believe, supports the stock in the mid-to-high $40’s valuation range.

TIMESPAN

INTERMEDIATE TERM (the next 3 months or more)

Over the intermediate-term, we believe that sequentially improving restaurant trends within the casual dining industry should provide support to Darden’s same-restaurant sales results. Darden’s blended “Big Three” (Olive Garden, Red Lobster, LongHorn) sales will almost certainly continue to lag the industry, but until management, willingly or otherwise, attacks the middle of the P&L, we believe a true turnaround will take some time.

LONG-TERM (the next 3 years or less)

The long-term is where there is real upside in Darden. This kind of opportunity does not arise in this space on a regular basis. Darden’s operating margins are in line with Brinker’s while its restaurant-level operating margins are 400-500 bps wider; we see this as indicative of a corpulent cost structure at Darden.

By our estimation, $293 million could and should be cut from SG&A, adding roughly $1.40 per share in EPS or $20 of share price upside. Combining this with the difference between our sum-of-the-parts valuation ($67) and the share price, we see roughly $33 of upside in the stock.

ONE-YEAR TRAILING CHART