THE HEDGEYE EDGE

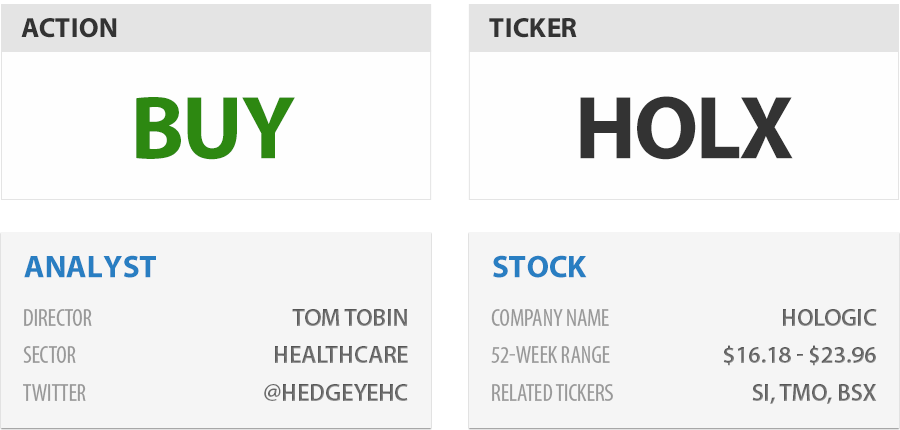

HOLX calls itself the “Women’s Health Company”. Its principal product lines are Breast Health (predominately mammography) and Diagnostics. HOLX is the US market leader in both mammography and Pap Tests.

The company has recently had difficulties with its Breast Health product line in F1Q13 (4Q12), and HOLX shares lost ground on the earnings release. We see this as buying opportunity as we view the current Breast Health weakness as temporary in nature, and not representative of its long-run potential.

In addition to its Breast Health business, we remain bullish on its Diagnostics segment, which is the company’s largest segment. In the near-term, we expect HOLX Diagnostics to benefit from both rising physician traffic and a recovery in US births. Longer-term, we see the HOLX’s Diagnostic segment as one of the largest beneficiaries to the Affordable Care Act insurance expansion set to begin in 2014.

TIMESPAN

INTERMEDIATE TERM (the next 3 months or more)

We’re expecting improving trends in F2Q13 (1Q13) in its Breast Health Segment, and we are already seeing signs of improvement in the macro indicators we follow. We expect the stock to rebound as the concerns over the Breast Health segment are mitigated by improving trends.

LONG-TERM (the next 3 years or less)

HOLX may be the most levered name in the Healthcare space to the pending Insurance Expansion set to take place beginning 2014. We see a long run-way in both the Diagnostic and Breast Health segment from the newly-insured members. Within Breast Health, Hologic is at the beginning stages of a long term capital cycle led by their launch of 3D-Tomosynthesis technology and capacity constraints emerging at the customer level.

ONE-YEAR TRAILING CHART