Macau has appeared bullet proof but one chink in the armor is emerging

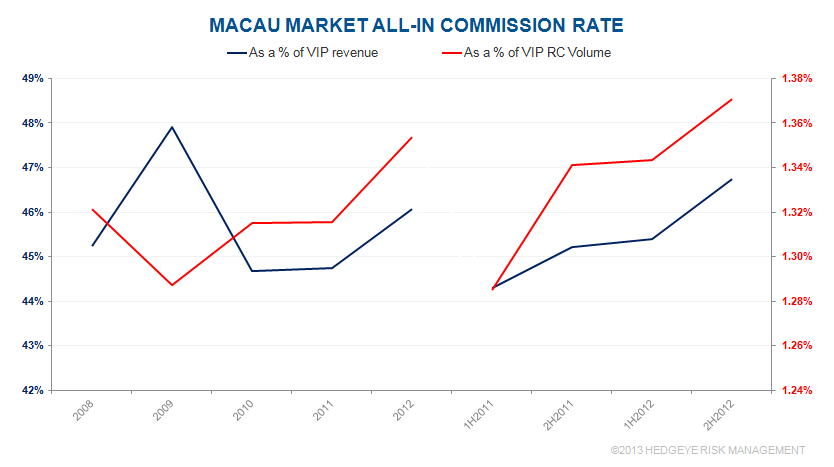

COMMISSION RATES RISING

Since bottoming in 1H 2011, the all-in commission rate paid by operators for VIP business has once again risen. Viewed as a % of win or as a % of RC, the conclusion is the same. The chart below shows 3 straight periods of higher commission rates.

RATE TIED TO VIP GROWTH

The rebate and comp portion of the all-in commission are contra-revenue items that reduce gross revenue. The junket commission impacts margins as it is a direct expense out of net revenues. Obviously, rising commissions are not a positive for the market and show how competitive the VIP segment has become. It will be interesting to see how commissions fare in 1H 2013 as VIP is undergoing somewhat of a resurgence, particularly here in March. As one can see from the following chart, commission rates tend to rise when VIP volume slows.

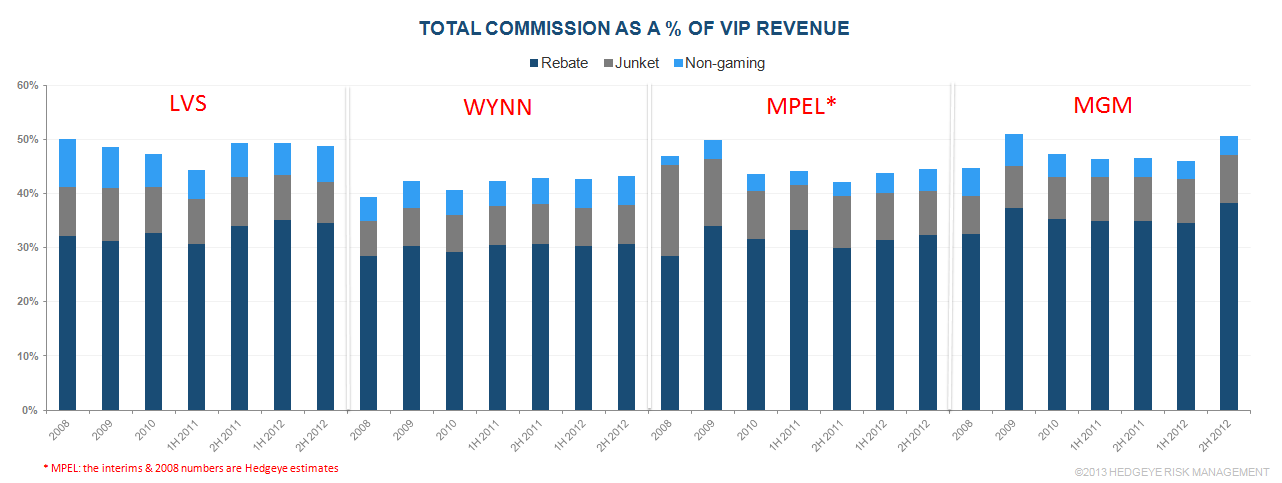

COMMISSION ANALYSIS BY COMPANY

The chart below shows the composition, by company, of all-in commissions among the straight junket commission, the rebate that goes back to the player, and non-gaming giveaways, all on a revenue share basis.

Takeaways:

- Rebates and comp’d non-gaming revenues are continuing to increase when measured as a % of RC and as a % of win while junket commissions actually declined on both a YoY and 2H12 vs. 1H12 basis. Part of the uptick that we are seeing in rebates and comps is likely driven by higher comps given to premium mass as that segment grows. While we know what rebates and comps are, we do not know how much of them go back to mass players.

- WYNN remains the least aggressive in its commission policy. From 2008 to 1H11, the spread between the average all-in commission rate paid by WYNN vs. average of LVS, MPEL & MGM narrowed from 7.57% to 2.85%. In 2012 it gapped out again to 4.14% and to 4.69% in 2H12.

- MGM took first place for offering the largest junket commissions in 2H12 at 8.9% (as a % of win) or 26bps (as a % of RC), ahead of MPEL which was formerly the most aggressive.

- Rebate rates

- The average rebate rate in 2H12 increased to 33.9% (as a % of win) or 100bps (as a % of RC) vs. 32.4%/96bps in 2H11

- WYNN had the lowest rebate rate in 2H12 at 30.7%/93bps

- MGM had the highest rebate rate in 2H12 at 38.2%/111bps

- Junket commission

- The average junket commission decreased 6% in 2H12 vs 2H11 on a % win basis, and 7% on a RC basis to 8.0%/23bps, respectively

- Wynn continued to offer the lowest commission rate of 7.2%/22bps

- MGM took the lead on offering the highest commission rate of 8.9%/26bps

- Comped non-gaming amenities

- The average non-gaming comps increased 12% YoY in 2H12 vs 2H11 to 4.9% as a % of win and to 14bps as a % of RC

- MGM offered the lowest comps at a rate of 3.5%/10bps

- LVS continued to offer the highest comps at a rate of 6.7%/20bps, which is not surprising given that they have the largest % of their revenue base coming from non-gaming amenities.

- The all-in commission rate

- The average all-in commission rate increased to 46.7% in 2H12 from 45.4% in 1H12 on a % of win basis and from 1.34% to 1.37% on a RC basis

- MGM paid the highest all-in rate at 50.6% or 1.47% in 2H12

- Wynn held the line at 43.2%/1.31% in 2H12