GDP: The Final GDP numbers for 4Q12 came in largely as expected with the final revision reflecting 0.4% growth for the quarter vs. expectations of +0.5% and against the preliminary and 1st revision numbers of -0.1% and +0.1%, respectively. A summary of the final numbers and revision impacts below.

Revision Breakdown - All changes are vs. 1st Revision:

- C (Consumption): Contribution to Chg in GDP = revised down -19 bps; Final Q/Q growth = +1.8%

- I (Investment): Contribution to Chg in GDP = revised higher by +37 bps. Final Q/Q growth = +1.3%, Residential Investment & Non-residential fixed investment Growth of 17.6% and 14.0%, respectively

- G (Government): Contribution to Chg in GDP = essentially flat, revised lower by -3 bps. Final Q/Q growth = -7.0%

- E (Net Exports): Contribution to Chg in GDP = revised higher by +9 bps.

- Inventories: Change in Private Inventories revised +3 bps

- Real Final Sales (Demand for U.S. Products ex Inventory change): Final Q/Q Growth = +1.9%, revised +20 bps

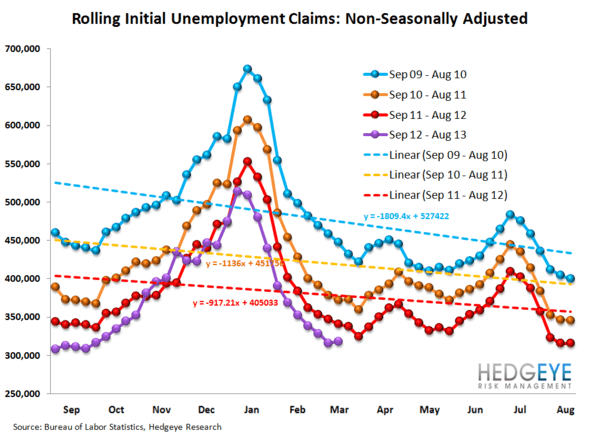

INITIAL CLAIMS: STILL IMPROVING, ALBEIT AT A SLIGHTLY LOWER RATE

Below is the detailed breakdown of the claims data from our head of Financials, Josh Steiner. If you would like to setup a call with Josh or trial his research, please contact

The good news is the labor market is still improving. The bad news is the rate of improvement isn't as strong as it had been. Rolling non-seasonally adjusted claims were lower YoY by 5.9% this week, as compared with 7.2% in the prior week. This rate of improvement is solid, but obviously a sequential deceleration. On a single week basis, the improvement slowed to -2.4%, down from -5.8% in the prior week. We place less emphasis on week to week moves as they've historically had significant volatility. The bottom line: the labor market is still improving, which is supportive for both credit quality and housing's momentum.

On the seasonally-adjusted side, the optical claims number was worse than expected rising 21k before revision to 357k. This brought the rolling SA print to 343.5k, an increase of 2.5k WoW. As this is what the market is paying attention to, it's logical that we're seeing the long end of the yield curve fall. This is incrementally bullish for housing, but obviously a continuation of headwinds on the margin. As a reminder, the SA data is now facing a small, but growing headwind over the coming six months. This headwind will peak in August 2013 and then turn into a tailwind for a final year.

Joshua Steiner, CFA

Christian B. Drake