There's a lot of both positives and negatives for me on HBI right now. Given that the stock has nearly doubled since management loaded up in Feb/March, it's tough for me to chase it here. Every quarterly release is an event for HBI, so here's a few things I'd look out for...

1) At face value, I don't love the revenue compares right now, but when I stack it up against retail sell-through (as reported by Sportscan) it suggests that we've gone through 1+ years of severe inventory destocking.

2) When I put that into context with the fact that 1) inventories that have been way out of whack for HBI for the past 3-quarters, and 2) the spread between revenue and retail sales appears to be narrowing, I can't help but get intrigued that the supply/demand balance is finding itself.

3) While revenues decelerate on both a 1yr & 2yr basis, Q2 will benefit from a BTS shift in 2008 that resulted in ~$50mm in revs to being pushed into Q3.

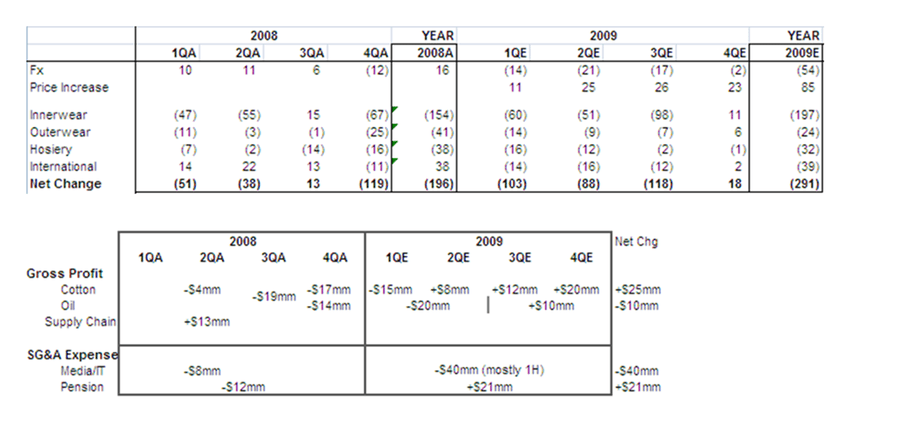

4) A 4% price increase was implemented at the end of January that effects Innerwear will not be enough to offset the Fx impact in Q1, but will more than offset Fx related losses for the balance of the year.

5) Cotton, oil and other sourcing/input costs should start to be a tailwind in 2H - at the same time we see easier balance sheet compares.

This name may be a rocky ride for a quarter or two, but worth looking at into 2H.