Last week we saw a sequential downtick in both athletic apparel and footwear, which was fairly consistent with the tough week that retail had in aggregate. In fact, it was not a bad showing at all given that the ICSC numbers put up the biggest sequential slowdown relative to prior-year levels in at least two years. The saving grace for both apparel and footwear is that price point integrity remains extremely high, with footwear ASPs up in the +10% range, and apparel up in the teens. A negative swing in ASPs would likely coincide with heavy promotional activity -- and we're not seeing it.

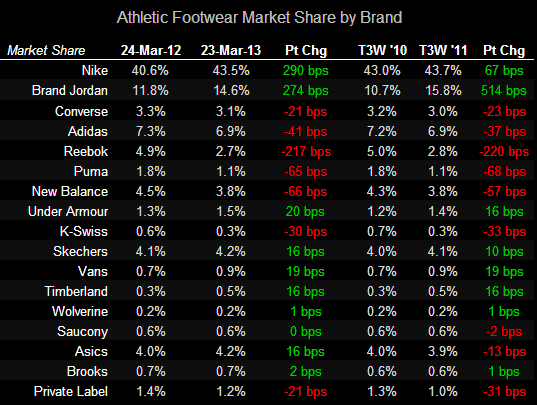

No surprises as it relates to winners and losers by brand. Nike and Jordan still dominating. Adidas and Reebok still trying to find a bottom, and Underarmour making very slow and steady improvement.

Source: SportscanINFO, NPD, and Hedgeye

ICSC RETAIL SALES INDEX (Sequential % Chg -- 80 Store Sample)

Source: International Counsel of Shopping Centers

Source: SportscanINFO, NPD, and Hedgeye

Source: SportscanINFO, NPD, and Hedgeye