Sentiment has recently rolled on the EUR/USD, which is substantiated by CFTC data. The Hedgeye Macro team is calling for a strong USD, however we are nowhere near calling for parity in the cross as others on the Street are, which we think is a misguided thesis.

Below we show recent data that confirms a slow growth environment in the Eurozone laced with political risk that we expect to continue to play out in 2013 – we pare some of the positive charts we’re looking at versus negative ones to better express the landscape.

Our takeaway remains that while we expect to see flair-ups of sovereign and banking risk this year, with the largest threats from Italy and Spain, we believe the spotlight on Cyprus to be short lived, and continue to discount the risk. Here we see both Draghi at the ECB and the Eurocrats –in their belief in the European project – as stability mechanisms to prevent contagion and maintain the current 17-member union.

Specific to Cyprus, and despite the weak card and messaging that Eurocrats have sent to the markets and other Eurozone countries about deposit holders at risk to cover bailout packages, we do believe the Eurocrats when they say Cyprus is a unique case (despite the confusion around wording of the issue from Eurogroup head Dijsselbloem). In fact, we think the political backlash would be so harsh if similar measure were issued on larger economies with larger populations that the Eurocrats would be too frightened to even suggest it.

One area to highlight is the larger threat of political uncertainty playing out in Italy. While it’s still anyone’s guess just how the scene will unfold, we think it’s probable that Bersani will stumble to form a coalition (he continues to reject Berlusconi’s hand) and a technical government will have to be issued until new elections can be called. We view Italian (and Spanish) equities as relative laggards. Both are broken across the TRADE and TREND in our models.

EUR/USD

Interestingly, Hans- Guenter Redeker, the head of global currency strategy at Morgan Stanley, recently said:

“Within 2 1/2 years or so, you could be very close to parity, so the risk of an undershoot is quite significant… The long-term implication is that monetary transition in Europe is not working, there’s no credit, no growth, and fiscal policy is still fragmented. So, therefore, you need to be fairly pessimistic for the outlook.”

While we don’t disagree with Redeker’s latter point, we do not agree with the former that the EUR/USD is heading to parity. First off, we think it is reckless forecasting so far out into the future, however we return to a long-held conclusion about incentives that we believe will prevent anything close to parity:

- Eurocrats are out to save their own jobs and pursue stability in the EU and Eurozone projects. This means limiting contagion at all costs. (Importantly, Merkel is still on board to write the checks so long as she can win her election in September first).

- The ECB is on-board to use its balance sheet to aid the Eurocrats and their member states.

In the first of two charts below we present our key levels on the EUR/USD cross. In the second chart we show that net positions in the EUR/USD according to CFTC data have turned decided bearish since the last weekend of February (Italian elections), which reflects sentiment.

Shifting Sentiment

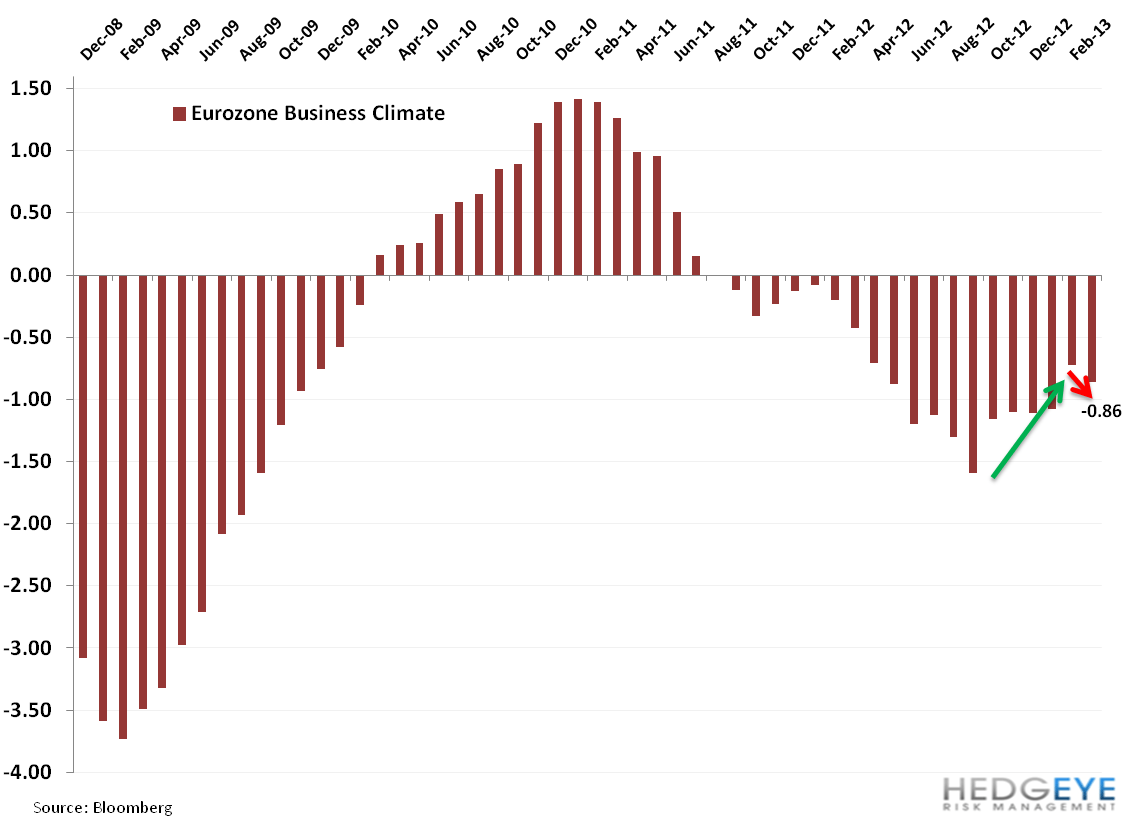

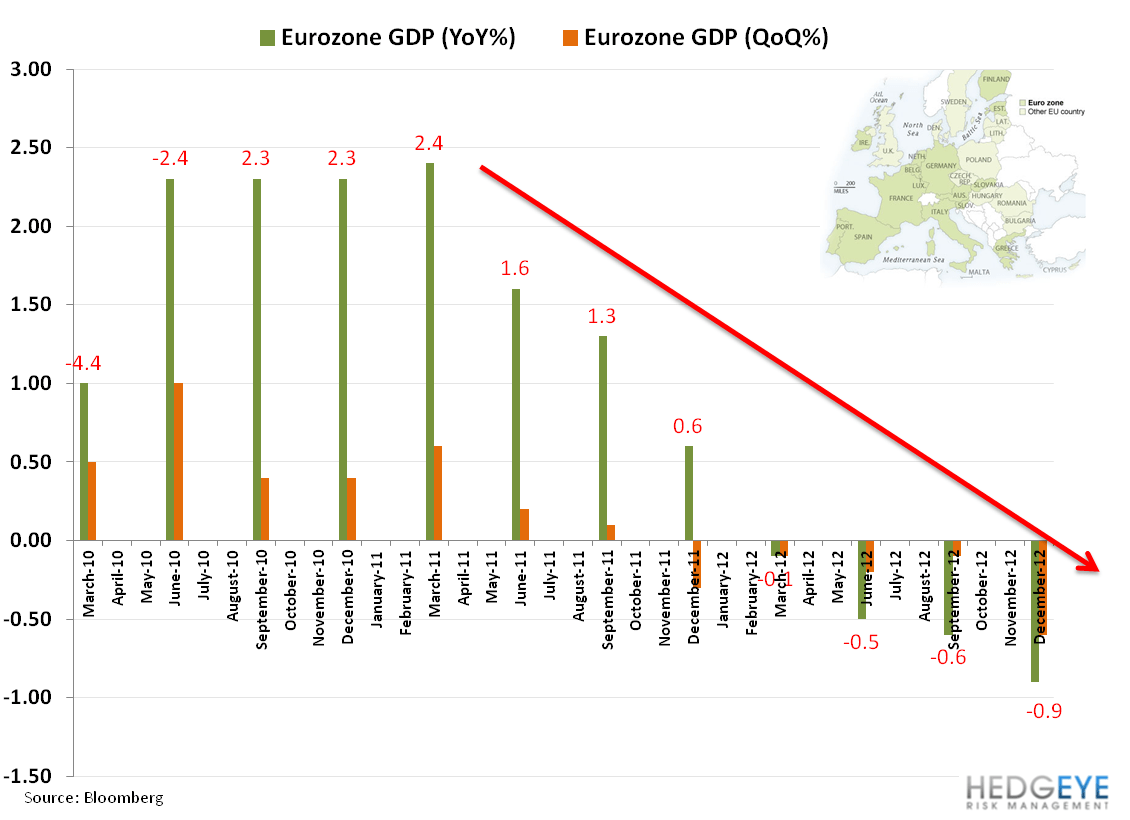

In the three charts below we take a look at confidence metrics across the Eurozone. We think market reactions are resetting to slower growth expectations across the region, particularly in the peripheral. Data across much of the region has not improved and governments continue to revise down their GDP targets as they reduce (or are excused on) deficit reduction targets, a perfect storm for increased bearish sentiment.

- Spain today revised its 2012 public deficit to 6.98% of GDP from 6.74% previously.

- Spain yesterday dropped its 2013 GDP forecast to -1.5% versus -1.4% previously.

By the Charts: The Haves

Below are three charts to keep in mind on the bullish side of the coin:

- Draghi’s willingness to leverage the ECB balance sheet, which is 15% smaller since last summer, due to factors such as the repayment of LTROs.

- CPI is below the ECB’s 2.0% target and the reduced tax on consumers hit hard by austerity and weak economic performance is a positive.

- External trade balances outside of the EU are heading in the positive direction.

By the Charts: The Have Nots

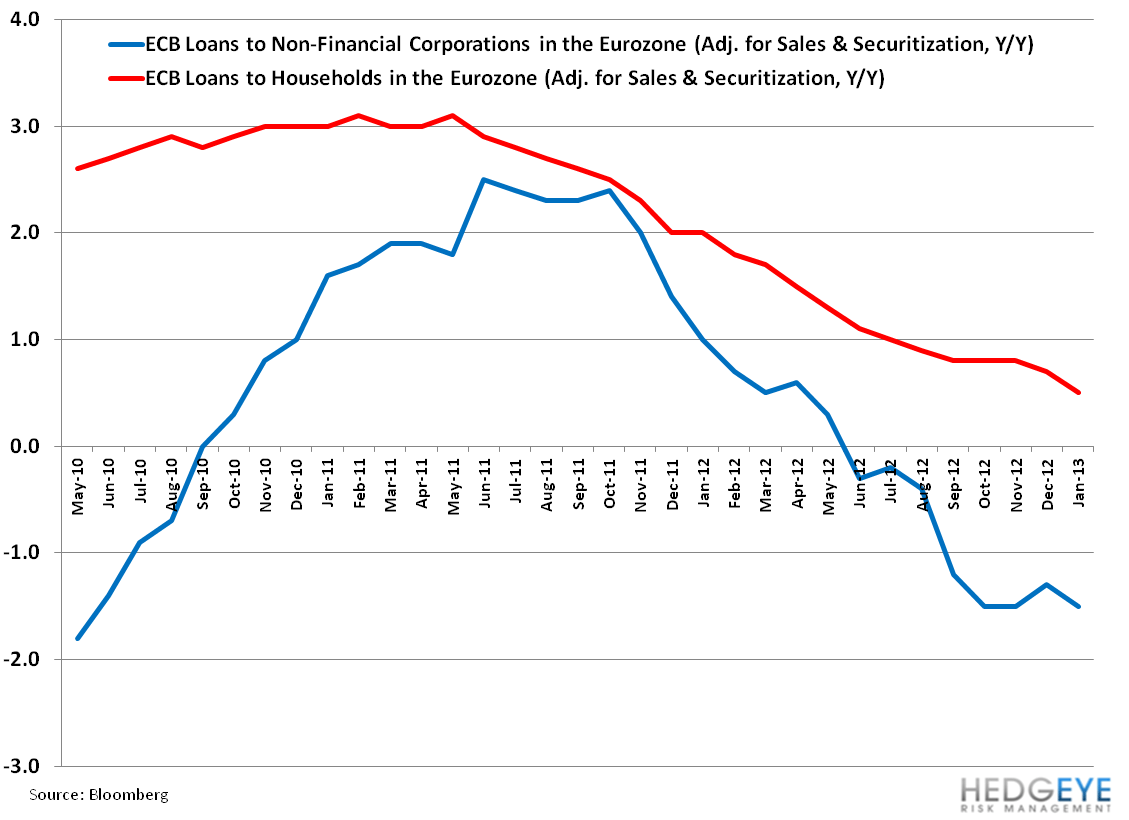

Below are five charts that reflect a constrained economic region, one that depends largely on the member states as its main trading partners for goods and services. This is represented by PMIs (mostly under 50 = contraction), GDP, Industrial Production and Retail Sales, and Car Registration. Finally we show ECB loans to Non-financial corporations and households that continue to show an anemic trend.

Italy

While it’s still anyone’s guess how the political scene will unfold in Italy, we think the political uncertainty will continue to pull the arrows in these charts lower.

Matthew Hedrick

Senior Analyst