“I’m thinking, Mom, I’m thinking.”

-Bill Gates

That’s how Joey Reiman starts Chapter 2 of Thinking For A Living – “The Golden Age of Ideas and Nine Thinkers Who Figured Out How To Make It Work For Them.” It’s a quick read and I’m enjoying it. Studying success inspires me more than Cyprus does.

Thinking for yourself isn’t easy. Maybe that’s why I find being on the road therapeutic. Since I’m not the brightest bulb on the tree to begin with, I’ll take every competitive advantage I can get. One of the big ones is having broad diversity in our client base. Thinking for a living about markets wouldn’t be complete without feedback loops. Thoughtful clients provide those. So does Twitter.

I was in Philadelphia for the day yesterday and had a dinner in Delaware last night. I’ll be in Baltimore today. Every client has a different style. They have different questions too. Selfishly, sometimes the best answer I can give in a meeting is ‘I don’t know.’ It means I haven’t thought about that enough; it means I need to be more thoughtful; and it means there is work to be done.

Back to the Global Macro Grind…

Got US #GrowthStabilizing and #HousingsHammer in the bag as your Big Macro Theme thoughts for Q113?

- US Durable Goods ramped +5.7% in February to a new intermediate-term TREND cycle high

- Case-Shiller’s US Home Price Index ramped to a new high of +8.1% vs 6.9% last month

- In response, the SP500 closed at its 2013 high of 1563 yesterday, two points off its all-time high

What about the Italian Election? What about Cyprus? What about the coffee you spilled on your white shirt?

There’s always something to be worried about in this good life. When it comes to your performance, the question is are you worried about the things that actually matter? And, if you are, have you expressed those concerns correctly in terms of your portfolio’s positioning? If you are bearish on Spain and Italy, why sell US Equities? Why don’t you just sell Spain or Italy?

To be sure, at the end of the world all of this will come home to roost. And the timing on that is something I think about a lot. It’s called mortality. But, in between now and then, I still need to grind through our interconnected Global Macro Risk Management Signals and see what we might want to be thinking about this morning:

USA

- US Dollar: up for the 7th week in the last 8, #StrongDollar continues to be a pro-growth signal (for the USA) in our model

- US Stocks (SP500): making higher-lows and higher-highs, they remain in a Bullish Formation with a risk range of 1

- US Equity Volatility (VIX): making lower-highs and lower-lows, fear remains in a Bearish Formation (risk range 10.82-14.42)

ASIA

- Chinese Stocks (Shanghai Comp): bullish TREND support of 2206 holds as economic data sets up to accelerate in March

- South Korean Stocks (KOSPI): trading back above its TRADE and TREND (1975) lines of support this morning

- Broad Based Rally: overnight, Philippines +2.7%, Indonesia +1.8%, Thailand +1.4%

EUROPE

- The Euro (vs USD): continues to break-down (lower-highs and lower-lows) with a bearish risk range now of $1.27-1.29

- German Stocks (DAX): testing immediate-term TRADE support of 7861 this morning; bullish TREND remains intact

- Spanish and Italians Stocks: both the IBEX (Spain) and MIB Index (Italy) are bearish on our TRADE and TREND durations

BREAKING NEWS: Italy is not the Philippines. Seriously.

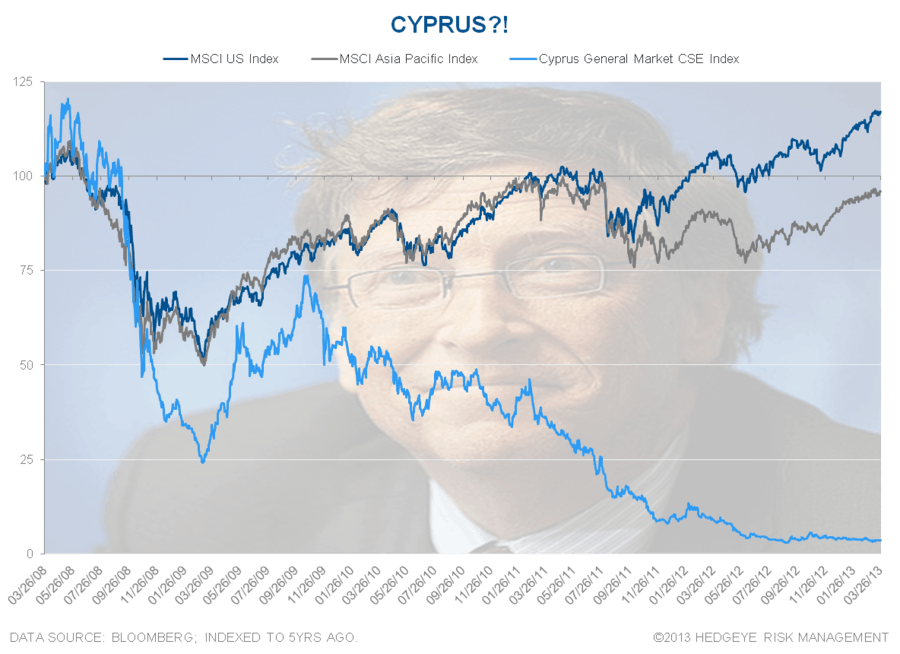

Who cares about 92 million people and a stock market that’s up +15% YTD (Philippines) when we can freak ourselves out about 1 million people in Cyprus whose stock market is down 98% since 2007?

Who cares about the Philippines getting its sovereign debt upgraded to investment-grade for the first time ever (Fitch this morning – ever is a long time), when we can still try to sell crisis coverage advertising when Italy’s debt gets downgraded?

I am obviously not thinking about the #EOW (end of the world) thesis correctly. But neither are the Asian and US equity market bears. Henry Ford said, “thinking is the hardest work there is, which is probably why so few engage in it.” Indeed.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, Russell2000, and the SP500 are now $1, $106.74-110.29, $82.65-83.38, 94.02-96.71, 1.88-1.96%, 10.82-14.42, 941-955, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer