Research Edge Postion: Long XLE; Long USO

We had an interesting conversation with a prospective client on Friday. He has been managing a global macro fund since the early 1990s, has CAGRed 18% in that time period with only one down year (down single digits), and currently manages in the billions. To say that this gentleman knows what he is doing is, obviously, an understatement. The one comment he made to us, which we found particularly interesting, was that he thinks he is the only commodity bear left.

In the year-to-date, it has been challenging to be bearish of most commodity classes. We use price as a primary factor in our models and, admittedly, that discipline has helped us have a positive return in commodities this year, despite clearly negative short to intermediate term fundamentals in many commodity classes. In particular, oil, at least from a domestic perspective, has flashed consistently bearish fundamentals this year.

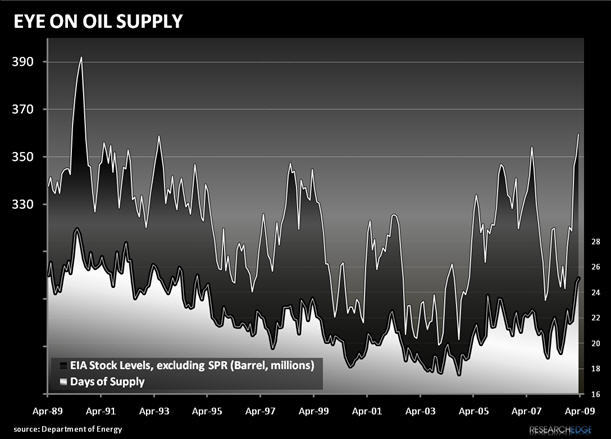

Specifically, inventory has been piling up in the U.S. This point was highlighted in a Bloomberg news article from Thursday of last week which was entitled, "Oil Rises Fourth Day as Stocks, Dollar Outweigh Demand Concern." The article went on to highlight that oil inventory in the U.S., as measured by the Department of Energy, had hit the highest level since 1990.

This increase in inventory year-to-date has had a seemingly minimal impact on the price of oil. We have attached two charts to this point. The first chart highlights a much more interesting point, which is that on a month-over-month basis there has been little correlation between inventory building and the direction of the price of oil over the last three years. In fact, over the last three years we calculated this correlation at ~0.20. The second chart highlights the current inventory build, which is at a 19 year high in raw inventories and days of supply.

Over time, we would presume that fundamentals will and do matter. That being said, the lesson of the last three years is that looking at supply data from the U.S. is literally irrelevant in trying to predict the direction of the price of oil in the short term. Recent history is clearly indicating to us that oil is being supported by drivers other than physical supply and demand data from the U.S. Clearly, a large portion of the driver is financial demand, which may move price, but not have a direct impact on the actually physical supply. Therefore, incorporating a view of increasing financial demand may be as relevant as having updated physical supply / demand models for oil.

We are going to touch more on this in coming notes, but as a frame of reference I wanted to attach an excerpt from Michael Masters' May 20th, 2008 testimony to Congress, which discussed the burgeoning and irrational demand in the financial markets for oil. No surprise this testimony and congress' rhetoric coincided with the top of the oil market in 2008, but the actual thesis is still relevant today.

"Commodities prices have increased more in the aggregate over the last five years than

at any other time in U.S. history. We have seen commodity price spikes occur in the

past as a result of supply crises, such as during the 1973 Arab Oil Embargo. But today,

unlike previous episodes, supply is ample: there are no lines at the gas pump and there

is plenty of food on the shelves.

If supply is adequate - as has been shown by others who have testified before this

committee - and prices are still rising, then demand must be increasing. But how do

you explain a continuing increase in demand when commodity prices have doubled or

tripled in the last 5 years?

What we are experiencing is a demand shock coming from a new category of

participant in the commodities futures markets: Institutional Investors. Specifically,

these are Corporate and Government Pension Funds, Sovereign Wealth Funds,

University Endowments and other Institutional Investors. Collectively, these investors

now account on average for a larger share of outstanding commodities futures contracts

than any other market participant.

These parties, who I call Index Speculators, allocate a portion of their portfolios to

"investments" in the commodities futures market, and behave very differently from the

traditional speculators that have always existed in this marketplace. I refer to them as

"Index" Speculators because of their investing strategy: they distribute their allocation of

dollars across the 25 key commodities futures according to the popular indices - the

Standard & Poors - Goldman Sachs Commodity Index and the Dow Jones - AIG

Commodity Index."

Whether we agree totality with Masters is not the point, but rather the point is to highlight that it is important to not overweight physical supply data points given the financial demand backdrop outlined above. While oil is down this morning ~5%, the fact that many commodity related stock markets around the globe are up year-to-date, Canada, Saudi Arabia, and Russia as examples, continues to signal to us that there is more risk to being a bear on oil at its current price.

Daryl G. Jones

Managing Director