This note was originally published at 8am on March 12, 2013 for Hedgeye subscribers.

“How with this rage shall beauty hold a plea?”

-Shakespeare

As our Director of Research, Daryl Jones, said on CNBC last week, “this is the most hated rally we’ve ever seen.” Hating the truth isn’t cool. But, as the late Andre Gide noted, “it’s better to be hated for who you are, than to be loved for someone you are not.”

Reality is that if you hate this market, you are raging against one of the more impressive 4-month changes in Asian and US growth prospects that we have seen in a decade. Cheering for the end of the world isn’t cool either.

A strong US currency, at the big turns (for both Reagan in the early 1980s and Clinton in the early 1990s), can be a Beautiful Rage. If sustained, it’s a pro-growth signal. So, from here, to have or not to have a #StrongDollar, remains the question.

Back to the Global Macro Grind …

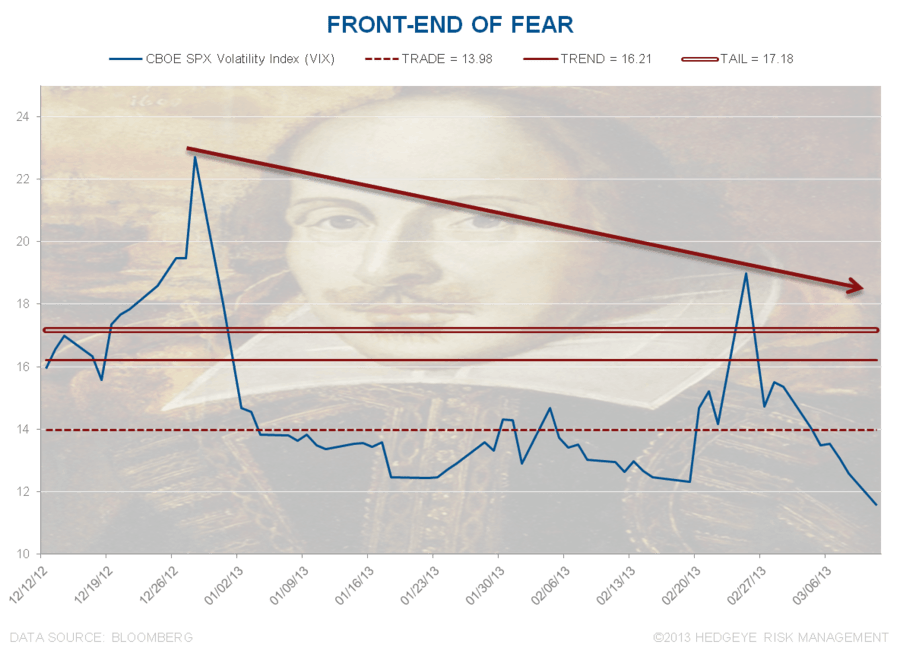

One of the most obvious places we’ve been monitoring Bear-Rage is in the term-structure of US Equity Volatility (VIX). At every lower-high (and lower-low) we’ve seen in the front-month VIX, many have still held onto their future fear expectations. That’s not working.

Looking at the Front-end of Fear (where front-month VIX is trading):

- VIX was down another -8.2% yesterday to close at a fresh 5yr low of 11.56

- VIX just crashed (and quickly), down -40% from its FEB25, 2013 “Italian Election” day lower-high

- VIX has been crashing, down -49%, from its DEC28, 2012 Congress New Year’s Eve lower-high

When I say lower-highs, I mean long-term lower-highs. And this has really been our point throughout the last 2-3 months. What was long-term support for the Front-end of Fear (14-15 VIX), is now solidifying itself as intermediate-term TREND resistance.

Just to put some risk management levels around that – across our core risk management durations:

- VIX immediate-term TRADE resistance = 13.98

- VIX intermediate-term TREND resistance = 16.21

- VIX long-term TAIL resistance = 17.18

So, the Front-end of Fear is being pulverized into what we call a Bearish Formation (bearish across all 3 of our core risk management durations – TRADE, TREND, and TAIL).

And, all the while, all you’ll hear from the hedge fund community is how the “term structure” of VIX doesn’t agree. In other words, consensus doesn’t agree with higher-highs in US stocks (perpetuated by lower-lows in volatility). That’s why it keeps working.

Bridgewater’s Ray Dalio outlines what an oversupply in consensus hedge funds has meant for returns. The correlation of hedge fund returns to US stock market beta = +0.9. If you want to be freaking out about something, freak-out about that.

Why is the asset management business changing? Well that’s pretty simple. It’s called evolution. Plenty of our pension fund, mutual fund, and RIA clients are changing what it is that they do as this globally interconnected game of global macro risk changes.

That has big implications. Don’t forget that the RIA (Registered Investment Advisor) community is as large (in terms of assets under management) as the hedge fund community.

Country, Currency, Commodity, etc. ETFs and the like are allowing lower-fee structures and strategies to compete, head-to-head, with Global Macro Hedge funds. Don’t fear that – competition is a beautiful thing too.

Some other tactical points to consider (in the immediate-term) as the VIX is crashing:

- Things that are crashing tend to bounce, fast – so watch what US stocks do once VIX tests our 11.21 oversold level

- SP500’s immediate-term Risk Range of 1534-1565 is finally signaling more downside than upside in US stocks

- Immediate-term Risk Ranges change as fast as price, volume, and volatility factors do – so keep moving

We’re not suggesting that we are smarter than anyone else. We have a broad spectrum of clients we are collaborating with. We are using quantitative signals and research to highlight what we think are becoming more probable non-consensus market moves.

In order to convince you that our risk management process is both flexible and dynamic, we have to Embrace Uncertainty. Selling certainty is like selling fear; over long periods of time, you’ll get run over by being anchored to either one or the other.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, Russell2000, and the SP500 are now $1556-1593, $109.51-110.98, $82.21-82.93, 93.56-96.81, 1.95-2.09%, 11.21-13.98, 928-951, and 1534-1565, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer