Close to a 52 week high but here’s a compelling case for significant multiple expansion.

Why are we still positive on MPEL after the stock has reached an all-time high? After all, we could cut bait after first recommending the stock at $4 per share back in the summer of 2010, clap ourselves on the back, and take a victory lap. We understand that with the volatility in this group and especially MPEL, a couple of weeks of “sluggish” GGR growth could haircut the stock considerably. But we’ll take the lumps over the near-term because we firmly believe that this stock is ripe for some serious multiple expansion and on potentially higher numbers.

The long-term (Tail in Hedgeye speak) and intermediate term (Trend) thesis can be summed up quite succinctly. After a 2 ½ year period of consistent upward earnings revisions, outperformance in the best performing casino market in the world, three major growth drivers including highly profitable same- store revenue growth, and a $12 billion market cap, MPEL is now a real company deserving of a real multiple. Over the near-term, we’re projecting another beat for Q1 2013 – despite lower than normal hold – and for FY 2013.

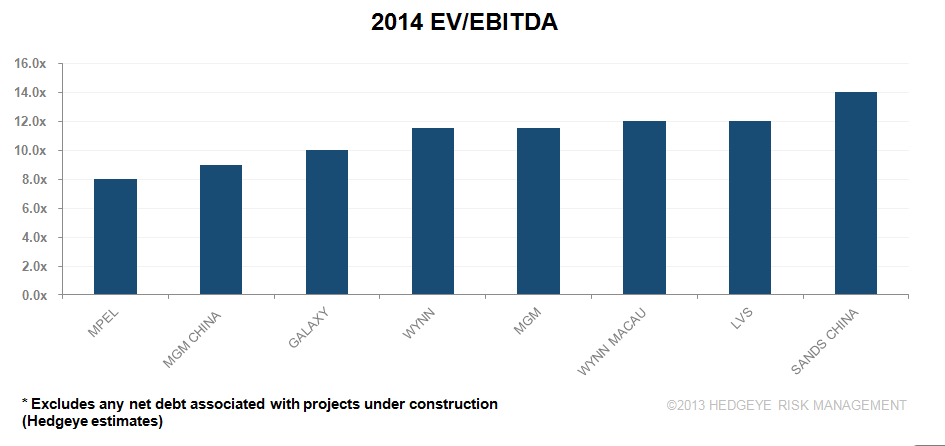

Shockingly, higher EBITDA drove most of the quintupling of the stock in 2 ½ years. That’s how good management has performed (or how bad they were performing 3 years ago). On a forward basis, despite the run, MPEL only trades at 8x 2014 EV/EBITDA after excluding Macau Studio City construction costs. Back at $4 in 2010, the multiple was 7x. The other US listed Macau operators currently trade between 9x and 14x. Remember that operators in Macau pay no income tax on casino profits, so an 8x multiple seems utterly ridiculous to us.

We don’t think MPEL is yet considered an investable stock by most investors. A glance at the top twenty shareholders indicates very few institutional long only investors, relative to a WYNN or LVS. We think more long only investors are inevitable – it’s happening already, trust us – which will push the multiple higher, in our opinion. What’s the right multiple? We think a 11-12x multiple is sufficient for now, which implies a $30 stock with upside from there as investors begin to look forward to the opening of Macau Studio City.

In summary, here is why we think MPEL deserves a higher multiple:

- Near-term: Macau booming again and MPEL maintaining/gaining share. Q1 and 2013 estimates – and thus implied 2014 – need to go higher.

- High ROI unit growth: Macau Studio City should open by 2015. With one of the best locations in Cotai, the fastest growing region in Macau, a 20-30% ROI is not unreasonable. Moreover, MPEL has structured a favorable investment/management contract in the Philippines with the Belle Casino.

- Huge cash flow and cash balance: Prohibitive covenants gone, net debt of roughly zero, and free cash flow (before project capex) well over $1 billion. In other words, Macau Studio City will be funded entirely out of free cash.

- Dare I say a proven management team? I’m not sure it can be denied any more following the turnaround they have engineered.

- Continued evolution of shareholder base toward more long only investors