As I see it, the news on housing can only get worse from here due to two factors. First, consumers stop buying new homes and second, the supply of foreclosed homes is so massive that there is an acceleration in the decline of home prices.

We learned today that the sales of new homes are showing indications that the housing decline may be near a bottom. As reported by the Commerce Department new home sales fell 0.6% last month to a seasonally adjusted annual rate of 356,000. Importantly, February was revised up from the originally reported 337,000 to 358,000. So the last three months were revised higher and the new data point was better than expectations. Great!

More importantly, at the current sales pace, it would take 10.7 months to work through existing inventory versus 11.2 last month and 13 in January.

As said yesterday, one nagging concern is the end of the foreclosure moratorium and the implications for the supply of unsold home within the financial system. Not to be trite, but what you can see is probably not there. Yes, foreclosures are on the rise, but the supply of foreclosed homes is probably not as bad as the depressionistas want you to believe. If they can't see it how do they know what the number is?

The most important factor in all of this is the consumer and is he/she willing and able to buy a home today? The data suggest yes!

On the issue of affordability we looked at median home prices, mortgage rates, monthly mortgage payment, and median family income. Given the dramatic decline in both home prices and mortgage rates, affordability is literally at a ~40 year high (most affordable) on this basis.

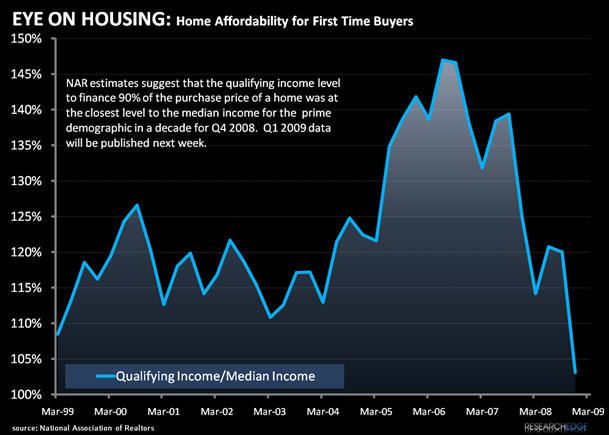

Obviously, there other variables to incorporate, but the NAR tracks this data back to 1960 using the same methodology, and February, the most recent data point, showed home prices on this basis (price, mortgage rates, and payments as a percentage of median income) to be literally the most affordable since 1971. The reading in February was 173.8, which was based on a median priced home of $164,600, mortgage rate of 5.12%, monthly payment of $717, median family income of $59.7K, and payment as a percent of income of 14.4%. Critically, as the chart below shows, the affordability of homes for first time buyers also reflects this price trend, with more young people positioned to buy as liquidity returns to the system.

Market prices don't lie, people do. Mr. Market is telling us that we are right and the US Housing bottom will be in the rear view soon.

Howard Penney

Managing Director