TODAY’S S&P 500 SET-UP – March 21, 2013

As we look at today's setup for the S&P 500, the range is 19 points or 0.82% downside to 1546 and 0.40% upside to 1565.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.70 from 1.71

- VIX closed at 14.39 1 day percent change of 7.71%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Init Jobless Claims, March 17, est. 340k (pr. 332k)

- 8:30am: Cont. Claims, March 9, est. 3.05m (prior 3.024m)

- 8:58am: Markit US PMI Prelim, March, est. 54.8 (prior 54.3)

- 9am: House Price Index M/m, Jan., est. 0.7% (prior 0.6%)

- 9:45am: Bloomberg Economic Expectations, March (prior -7)

- 9:45am: Bloomberg Consumer Comfort, March 17 (prior -31.6)

- 10am: Freddie Mac mortgage rates

- 10am: Philadelphia Fed, March, est. -2.5 (prior -12.5)

- 10am: Existing Home Sales, Feb., est. 5.0m (prior 4.92m)

- 10am: Existing Home Sales M/m, Feb., est. 1.6% (prior 0.4%)

- 10am: Leading Indicators, Feb., est. 0.4% (prior 0.2%)

- 10:30am: EIA natural-gas storage change

- 11am: Fed to buy $1.25b-$1.75b notes in 2036-2043 sector

- 1pm: U.S. Treasury to sell $13b 10Y TIPS in re-opening

GOVERNMENT:

- Obama meets w/ Palestinian Authority President Mahmoud Abbas during 3-day visit to Middle East

- 8am: House of Representatives Steel Caucus briefing w/ Nucor CEO John Ferriola, US Steel CEO John Surma

- 10am: Federal Transit Admin. Peter Rogoff testifies on effects of sequestration, grants made to local transit systems

- 11am: NOAA delivers 90-day temperature, precipitation outlook

WHAT TO WATCH

- Blackstone said to approach Hurd about running Dell

- HP directors rebuked in re-election by slim holder majority

- Intuitive Surgical announces $1b share buyback program

- Bernanke says he’s dispensable, suggests tenure winding down

- Sales of existing U.S. homes probably climbed to 3-yr high

- Cypriot president seeks new finance plan; banks still closed

- Delta said to weigh order for $4.3b of wide-body jets

- EU to curb banker bonuses after deal on Basel III law

- GM turnaround plan for Opel to be tested by union vote

- General Moly suspends loan work after China detention report

- GE Capital to buy Allianz’s commercial lending unit in Australia

EARNINGS:

- KB Home (KBH) 5:30am, $(0.22) - Preview

- IHS (IHS) 6am, $0.85

- Athabasca Oil (ATH CN) 6am, C$(0.03)

- Lululemon (LULU) 7:15am, $0.74

- ConAgra (CAG) 7:30am, $0.56

- Worthington Industries (WOR) 8:20am, $0.49

- Ross Stores (ROST) 8:30am, $1.07

- Micron Technology (MU) 4pm, $(0.20)

- Tibco Software (TIBX) 4:05pm, $0.18

- Nike (NKE) 4:15pm, $0.67

- Silver Wheaton (SLW CN) After-mkt, $0.49

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

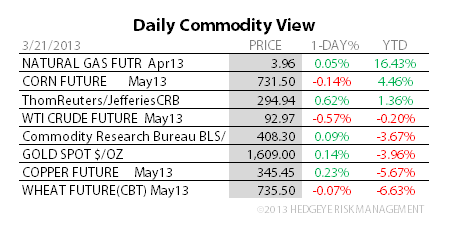

- WTI Crude Drops as German Data, Cyprus Plan Spur Europe Concern

- Gold Giants Shrink to Fit as Paulson Pushes Breakup: Commodities

- Cotton Harvest Worldwide Seen Slumping as Farmers Shift to Grain

- Gold Trades Near 3-Week High as Investors Weigh Europe Debt Woes

- Lead and Zinc Gain as Chinese Manufacturing Expansion Speeds Up

- Soybeans Advance to One-Week High on Shipment Delays in Brazil

- Palm Oil Gains to One-Month High as Inventories Seen Declining

- Gold Demand in India Climbing May Weaken Attempt to Curb Deficit

- Commodity Catch-Up With Stocks Seen as Elusive: Chart of the Day

- Cotton Rally Encouraging Farmers to Sow More Than USDA Forecast

- Rebar Advances for Third Day as Chinese Manufacturing Expands

- Biggest Solar Collapse in China Imperils $1.28 Billion: Energy

- Feud Threatens Russia Port Profits as CEO Is Suspended: Freight

- China Cotton Imports Seen Exceeding USDA Estimate as Prices Rise

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team