We recently received a follow-up question from a client who was "surprised by the long Germany call" when, to his point, so many German jobs are tied to the ailing automotive industry. The client brings up a good point which was not included in our post on 4/21 "EWG: Why We Bought Germany Today." Below you'll find our response to the question, which argues that although the German automotive industry has taken a huge blow in this global recession, the strength of German unions and the subsidy measures granted by the government to prop up the industry have helped to maintain jobs and offset double-digit sales declines as the industry rides off decreased global demand.

As a point of reference in case you didn't read the original post, part of our reasoning in taking a long Germany position is to hedge against our short exposure to Switzerland via the etf EWL.

---------Thanks for your response. I'm not an automotive analyst, but I have spent a fair amount of time looking at Germany. As you're well aware the automotive industry lies close to the German soul and therefore everything is being done to save it; concurrently GM's Adam Opel in Germany is looking for a buyer. The government has yet to step in, hoping to find a private buyer, yet you can bet that both acting Chancellor Merkel and her incumbent Frank-Walter Steinmeier will be making this a central issue to resolve as election day nears in September.

Firstly, it's important to keep in mind the historical and cultural framework of the German workforce to get at an understanding of the auto industry. German schooling (much like other European countries, but arguably more so) is very rigid from an early age, tracking children to particular schools (university track, technical, vocational). This leads to the cultural mentality that each individual is suited for one particular industry/profession, which leads both employees and employers to value job security above all else. German business/organizations are very hierarchical and the lack of entrepreneurship compared to the US is strong.

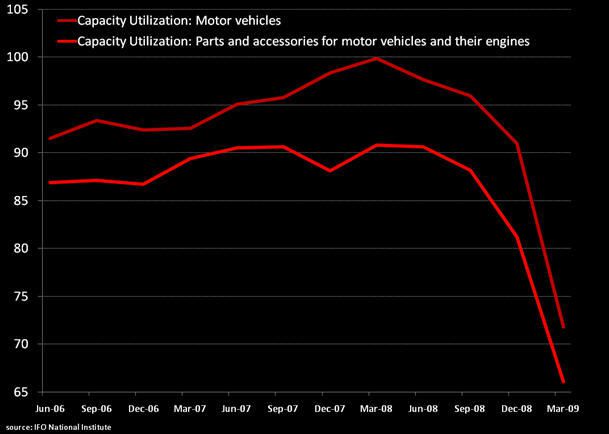

In short, German automotive jobs are relatively resilient (see chart below) for German trade and labor unions play a large part to insure job security. As an example, the government recently extended subsidies so that companies can keep workers on payrolls for as long as 18 months-it used to be 6-even if layoffs might be easily justified. For cyclical industries like autos, this could mean the difference in riding out the global recession that has destroyed demand. The government has also created a short work program from more than 670,000 workers and in March the number of applicants was up 55 times.

To use Daimler as an example of labor's pull...although the company threatened a first round of job cuts at its annual meeting last week, management can't carry it out before the end of 2011. In short, it's hard to fire people.

While EWG, the ETF we purchased, has a sector exposure to industrials of only about 15%, your point about the overall exposure of the German economy to the Automotive Industry is well taken. (My sources show 1 in 8 Germans are tied to the auto industry).

Yet, Germany is working to help incentivize the auto industry in particular (so much so other industries are crying foul). Germany has issued an auto rebate program (Abfrakpraemie) by which individuals can trade in their old cars (9 years+) and receive 2500 Euros towards a new car that meets certain emission standards. The program has been a huge success and has helped to drive sales. The government said it expected 2 million purchasers to apply for subsidies, costing it 5 Bill Euros this year. While German auto sales were down globally on the whole in the first two months/1Q of 2009, both Daimler and BMW announced that the drop in sales in March relative to the same month last year was less than the year-on-year drop measured in previous months. Further, most major German automakers reported that sales rose considerably in China.

Additionally, Daimler received a 2 Billion euro investment from Abu Dhabi's sovereign wealth fund in return for 9.1% of its stock. Perhaps investment from abroad could pick up in the near term at the right price. Therefore I'm of the opinion that despite the country's leverage to Autos, it is relatively stable, despite the global recession's impact on the automobile industry.

Matthew Hedrick

Analyst