FedEx: Clock Starts Now

- Specific Timing Positive: Excess FedEx Express capacity, particularly in Asia, has been a problem for a many quarters. While a smooth transition with intact service levels is obviously critical, the April 1 specific date for Asia capacity reductions is a positive. On the FY2Q earnings call, management commented that we should see margin improvement in FY4Q and the April 1 date seems consistent with that outlook. In short, we should see a FY4Q performance that is significantly better than FY3Q.

- Probably a Lower Bar: Since 2016 FedEx Express cost reductions of $1.6 billion are measured against 2013 results, the Express restructuring may now be against a slightly lower bar. While that is incrementally negative, the overall opportunity remains enormous relative to FDX's market value. We also suspect that the company can exceed its cost reduction goals. The company commented that the cost cuts are on track and that much of those benefits should be achieved by FY 2015.

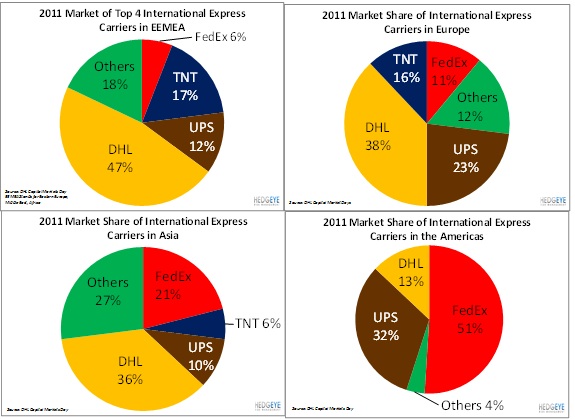

- It’s Always a Competitive Issue: International Express is a cost leadership industry, in our view. Operating with excess capacity, misallocated network capacity and old aircraft is a recipe for weak margins, since competitors can price based on their lower cost structures. Retiring 727’s “early” would have meant retiring them some years ago, in our view. Retiring them ASAP seems like a fantastic plan and an easy way to expand margins, as does removing excess capacity.

- Not Really Volumes: While Express volumes are not exploding higher, most of FedEx Express’s FY3Q pain seems self-inflicted. While painful for investors today, it should be fixable. International Express volume has been shifting toward slower, cheaper channels for a while and the company is finally responding.

- Ground Fine: FedEx ground continued to take share. Margins faced a tough comp on a one-timer last year. Growth in SmartPost is likely to limit margins, but is a result of a market expansion and not a market problem, in our view.

- Domestic Express Improved: Domestic Express apparently improved, with International Express the key laggard....

- International Delay Could Possibly Mean TNT Deal: That FDX did not take stronger actions in the quarter to rationalize International Express capacity may mean that it is waiting on a TNT integration. FDX management discussed network imbalances on the call. That is speculation on our part, but a TNT transaction would more effectively balance the international network, in our view.

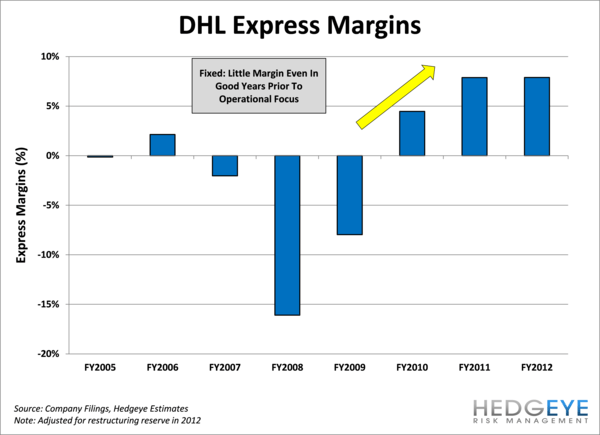

- If DHL Can Do It…: We have confidence that FedEx Express can dramatically improve its margins toward peer levels for a number of reasons. First, the industry is well structured with two competitors domestically and basically three and a half internationally. FedEx has strong market positions in the Americas and Asia. Another indication that FedEx Express can restructure successfully is that Deutsche Post’s DHL Express Division did so from a much worse operating position.

- A Long-term Long Story: Since our FDX black book, we have expected that FY4Q 2013 (next quarter) should be the inflection point for Express margins. We obviously did not expect the sequential margin drop this quarter, but do not see it as a meaningful risk to our thesis. If FedEx Express can match competitor margins by FY2016, FDX should find itself with two businesses that are each worth roughly what the company currently trades for. To the extent that margins start to expand next quarter, the market may start to price that outlook in ahead of its actual achievement. We continue to think that FDX is one of the best long opportunities in the sector and would use weakness in coming days to add positions at what we expect to be the Express margin inflection point.