This note was originally published March 19, 2013 at 20:56 in Retail

Here’s a review of who’s gaining share, who’s losing it, and who barely has their head above water. Hint: a) Nike, b) AdiBok, c) Unde rArmour

Here’s an overview of market share winners and losers, based on NPD’s monthly market share data:

a) Nike Brand market share is parabolic. Brand Jordan and Converse are both healthy, but stable.

b) AdiBok is a train wreck – both sides of the house. It’s a good thing that the brands have better allure outside the US.

c) UnderArmour is barely UnderWater. The general trajectory of its market share change is positive, but still unable to sustain share above 1% of the US market.

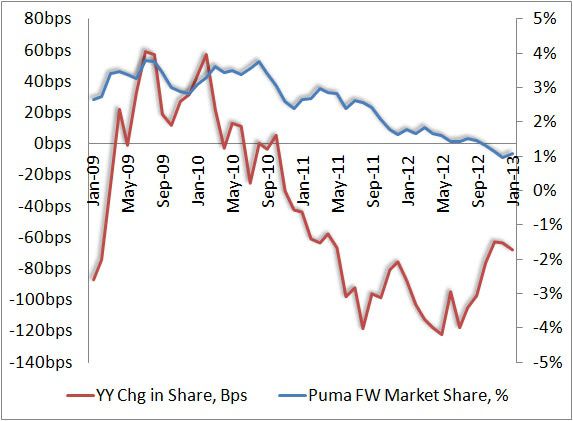

d) Puma is in a death spiral.

e) New Balance continues to grind higher in regaining its position as one of the top five brands. Its share now exceeds Reebok and equals Adidas.

Nike Brand Market Share

Source: NPD

Brand Jordan Market Share

Source: NPD

Converse Market Share

Source: NPD

Adidas Brand Market Share

Source: NPD

Reebok Market Share

Source: NPD

UnderArmour Market Share

Source: NPD

New Balance Market Share

Source: NPD

Puma Market Share

Source: NPD