This note was originally published at 8am on March 06, 2013 for Hedgeye subscribers.

“He gave the nation the idea of American progress.”

-John Meacham

That’s what John Meacham wrote about Thomas Jefferson in his prologue to the latest brick I tackled on a flight yesterday to San Francisco, California: Thomas Jefferson: The Art of Power.

“To his friends, who were numerous and devoted, Jefferson was among the greatest men who ever lived… to his foes, who were numerous and prolific, Jefferson was an atheist and a fanatic, a demagogue and a dreamer.” (Prologue xxiii)

Do you have a vision for your family and firm? Are you a dreamer? I am. And I’m damn proud of it too. Listening to politicians who don’t get liberty, free markets, and the purchasing power of success (#StrongDollar) has run its course. It’s a cycle. And so is American Progress.

Back to the Global Macro Grind…

At this point, the sequential progress in the US Economic data from December 2012 to March 2013 is glaringly obvious. When my signals tell me to, I have no problem fighting the Fed. But I don’t fight the data.

From US Housing to Employment (they progressed first), to more coincident economic indicators like yesterday’s ISM Services report (best since 2011), the risk management question now isn’t “where do I sell?” It’s “could growth stabilizing become #GrowthAccelerating?”

We analyze a lot of “stuff”, but some of the more forward looking “stuff” comes in the form of new order growth:

- ISM Manufacturing New Orders accelerated from 53.3 in JAN to 57.8 in FEB

- ISM Services New Orders accelerated from 54.4 in JAN to 58.2 in FEB

- PMI Manufacturing New Orders accelerated from 58.2 in JAN to 60.2 in FEB

So, if you use that “stuff” (otherwise known as economic data), you’d answer yes to the question of recent American Progress. But these are new orders, what about new consumption growth tailwinds that we didn’t have in JAN or FEB?

How about Oil prices coming down? Amidst all of the #PoliticalClass fear-mongering about the spending problem they created, could Sequestration = Strong Dollar = Down Oil = Stronger real (inflation adjusted) Consumption Growth?

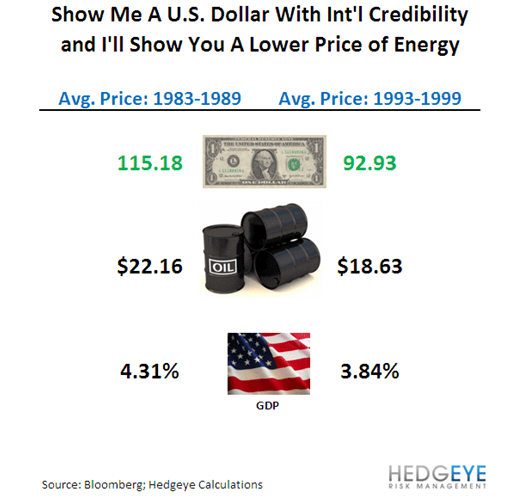

I’m no atheist, and my loathers can call me fanatic about this Strong Dollar Tax Cut idea all they want, but history sides with the Canadian on this front, bros. As you can see in today’s Chart of The Day, under both Reagan (1983-1989) and Clinton (1993-1999), American Progress was built on the back of a Strong Dollar, pro growth, recovery.

How does Mr Market score our theme of being long Consumption?

- US Healthcare Stocks (very much an American Consumption story) = +11.33% YTD (XLV)

- US Consumer Staples Stocks = +10.72% YTD (XLP)

- US Consumer Discretionary Stocks = +9.66% YTD (XLY)

Yes. All of those are beating what’s been a fantastic +7.9% YTD return for the SP500. And how does Mr Market score being short (or underweight) Commodity Inflation Expectations?

- US Basic Materials Stocks = +3.41% YTD (XLB is the worst performing Sector in the S&P Sector Model)

- CRB Index (19 commodities) = -1.35% YTD (awful relative to any major asset class)

- WTI Crude Oil = -1.4% YTD (having recently broke our $93.79/barrel TREND line of support)

OK. So being long Consumption growth and short Commodity exposures is still working. How is the end of the world trade going?

- Gold = down again this morning to $1574, = down -6.02% YTD

- US Treasuries = 10yr Yield up to 1.92% this morning = up +9.09% YTD

Again, if the world was going to end: A) all US economic data wouldn’t have gone from slowing to stabilizing to accelerating (look at the slope of the line) and B) Gold and Treasuries wouldn’t be losing you money in 2013 YTD.

I know, I know. People want to bring up what happened last year, and the year before that. I know, it’s like arguing with my college girlfriend. It was painful. But I got over it.

I don’t live a regressive life. I’m writing about American Progress because we have a tremendous opportunity here. What’s not only been happening for 3 months, but what could keep happening if the #StrongDollar setup remains excites me. It should excite you too.

Look at your screens. Markets are testing all-time highs. Be a leader. Be proud. Cut government spending. Get these people you already have on mute off TV. Let’s get back to what makes this country the most progressive that the world has ever seen. This is our chance.

Our immediate-term Risk Ranges for Gold, Oil (WTIC), US Dollar, USD/YEN, UST 10yr Yield, VIX, Russell2000 and the SP500 are now $1549-1584, $89.76-91.98, $81.76-82.38, 91.79-94.68, 12.21-14.63, 910-932, and 1519-1543, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer