Sentiment isn’t actually at the bottom of the sea but the Carnival brand image may be sinking.

Carnival has had a rough March so far, in share price and public sentiment. While sentiment has turned sour, it probably hasn’t bottomed. We think the deterioration of its brand could be the lasting issue. With the company still licking its wounds from the Costa Concordia tragedy, a compounding number of heavily publicized brand specific issues have further tarnished the brand. Until sentiment bottoms and/or visibility improves, we’re not sure investors should be buying the thesis that this is just a short-term blip.

Multiple ship mechanical issues and an unrelenting media attack stemming from each incident have surely damaged the Carnival brand and potentially the whole cruise industry. The timing of less publicized stories regarding a gastroenteritis outbreak at Grand Turk (Holland America Line, Princess Cruises, and Carnival Cruises) and a robbery that left two people dead (P&O Cruises) hasn’t helped. Other cruise liners also have incidents in 2013 (e.g. Norovirus on Royal Caribbean’s Vision of the Seas; minor fire on Norwegian’s Getaway new build) but they have remained relatively shielded from the media and public. In addition, there have been more cancellations. Carnival Triumph today canceled 10 more cruise itineraries, which means service will not resume until June 3. Carnival Sunshine canceled two European cruises to allow enough time to complete its dry dock and ensure its operations are fully improved. All is well though because travel agents and Carnival management are working nonstop to reassure its clients and interested parties that these are one-off incidents and that all ships are safe. Tired of those words?

Investors have punished the stock, which has fallen 12% since the Carnival Triumph fire (February 10). As we wrote in “CHART DU JOUR: CCL: IT COULD GET SMELLIER (2/14/13),” CCL could underperform the S&P 500 over the next month if we use the Carnival Splendor fire as a comp. Thus far, CCL has trailed the S&P by 15% since February 10.

But all is good because Carnival is low balling guidance again, right? Not so fast. We think whisper expectations are for a beat. Current 2013 Street EPS is at the high end of CCL’s guidance range of $1.80-$2.10 for fiscal year 2013. Moreover, sentiment metrics haven’t been overextended to the bearish side. The percent of buy/overweight analyst ratings have actually crept higher since December 2012. Meanwhile, short interest is climbing out of a recent bottom.

Before addressing the question of whether the brand is tarnished, some fundamental concerns were already emerging. Onboard and other yield growth, which mitigated some of the net yield decline in 2012, may be slowing. From a net yield perspective, this is troubling as CCL’s onboard and other yield as a % contribution to net yield recently grew to its highest level ever. This could be an indication that the resilient and robust onboard spending by North Americans may be losing its ability to offset the thrifty spending by Europeans. RCL’s onboard spending, on the other hand, while not immune, is less exposed to this.

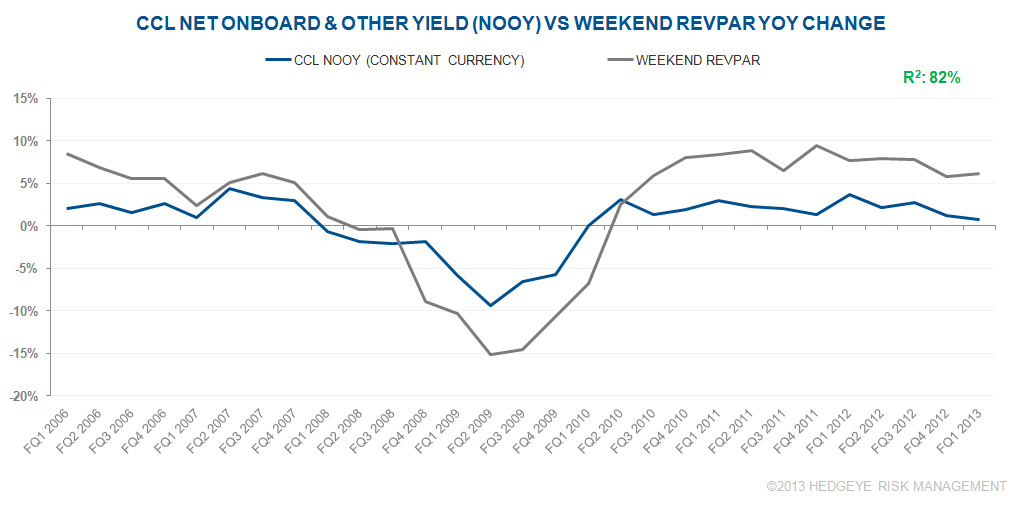

The macro still looks ok for the cruisers so we may be looking at just a CCL issue. US weekend (leisure) REVPAR is not suggesting a major pullback. We track weekend REVPAR on a weekly basis and its R2 to CCL’s onboard & other yield is 82%.

At 13x 2014 EPS, it is trading below its 5 year average valuation. However, if the brand is indeed tarnished, revenue and EPS estimates might be aggressive. Sentiment still has room to fall, in our opinion, and combined with a potentially less attractive fundamental backdrop suggests a much lower stock price.